Vhat are the NE quantities, price, and profits if there is no government intervention. o block entry, the incumbent appeals to the government to require that the entrant xtra costs. What happens to the equilibrium if the legal requirement causes the al cost of the second firm to rise to that of the first firm, $20? Jow suppose that the barrier leaves the marginal cost unchanged, but imposes a st. The incumbent keeps its strategy from a). What is the minimal fixed cost that 1

Vhat are the NE quantities, price, and profits if there is no government intervention. o block entry, the incumbent appeals to the government to require that the entrant xtra costs. What happens to the equilibrium if the legal requirement causes the al cost of the second firm to rise to that of the first firm, $20? Jow suppose that the barrier leaves the marginal cost unchanged, but imposes a st. The incumbent keeps its strategy from a). What is the minimal fixed cost that 1

Managerial Economics: A Problem Solving Approach

5th Edition

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Chapter17: Making Decisions With Uncertainty

Section: Chapter Questions

Problem 10MC: You are considering entry into a market in which there is currently only one producer (incumbent)....

Related questions

Question

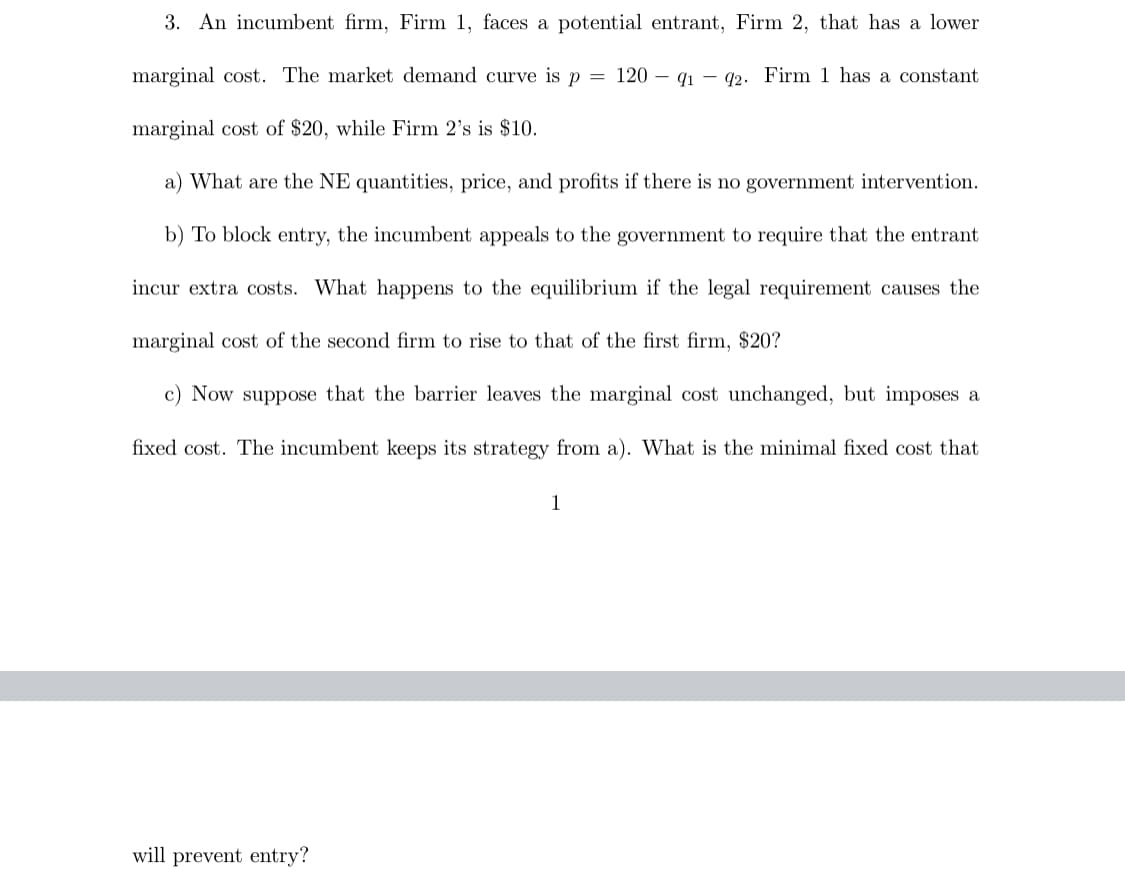

Transcribed Image Text:3. An incumbent firm, Firm 1, faces a potential entrant, Firm 2, that has a lower

marginal cost. The market demand curve is p =

120 – 91 - 92. Firm 1 has a constant

marginal cost of $20, while Firm 2's is $10.

a) What are the NE quantities, price, and profits if there is no government intervention.

b) To block entry, the incumbent appeals to the government to require that the entrant

incur extra costs. What happens to the equilibrium if the legal requirement causes the

marginal cost of the second firm to rise to that of the first firm, $20?

c) Now suppose that the barrier leaves the marginal cost unchanged, but imposes a

fixed cost. The incumbent keeps its strategy from a). What is the minimal fixed cost that

1

will prevent entry?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning