Which describes the firms supply curve for the short run with perfect competition? O The section of MC that is above AVC O The section of MC that is above ATC O There is no supply curve since it depends on the slope of demand O The section of ATC to the right of its intersection with MC

Which describes the firms supply curve for the short run with perfect competition? O The section of MC that is above AVC O The section of MC that is above ATC O There is no supply curve since it depends on the slope of demand O The section of ATC to the right of its intersection with MC

Principles of Economics 2e

2nd Edition

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:Steven A. Greenlaw; David Shapiro

Chapter8: Perfect Competition

Section: Chapter Questions

Problem 1SCQ: Firms ill a perfectly competitive market are said to be price takers that is, once the market...

Related questions

Question

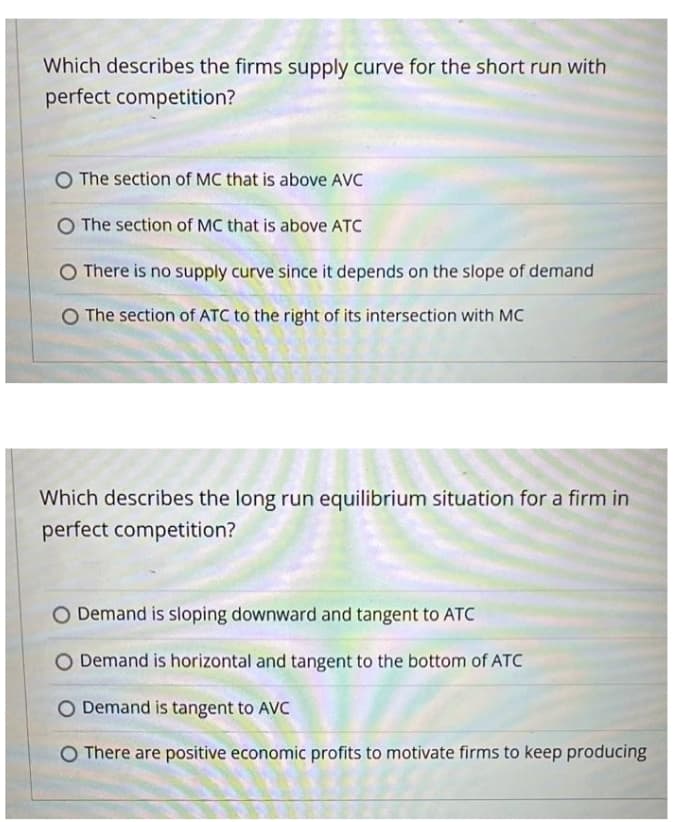

Transcribed Image Text:Which describes the firms supply curve for the short run with

perfect competition?

O The section of MC that is above AVC

O The section of MC that is above ATC

There is no supply curve since it depends on the slope of demand

O The section of ATC to the right of its intersection with MC

Which describes the long run equilibrium situation for a firm in

perfect competition?

O Demand is sloping downward and tangent to ATC

Demand is horizontal and tangent to the bottom of ATC

O Demand is tangent to AVC

O There are positive economic profits to motivate firms to keep producing

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Economics (MindTap Course List)

Economics

ISBN:

9781337617383

Author:

Roger A. Arnold

Publisher:

Cengage Learning