Why these preference shares is convertible into 100 L’Occitane ordinary share. The ordinary share capital (in the second image)aren't 3000000 and debit another subject (I don't know how to balance it).

Why these preference shares is convertible into 100 L’Occitane ordinary share. The ordinary share capital (in the second image)aren't 3000000 and debit another subject (I don't know how to balance it).

Financial Management: Theory & Practice

16th Edition

ISBN:9781337909730

Author:Brigham

Publisher:Brigham

Chapter21: Dynamic Capital Structures And Corporate Valuation

Section: Chapter Questions

Problem 3MC: David Lyons, CEO of Lyons Solar Technologies, is concerned about his firms level of debt financing....

Related questions

Question

Why these preference shares is convertible into 100 L’Occitane ordinary share. The ordinary share capital (in the second image)aren't 3000000 and debit another subject (I don't know how to balance it).

Transcribed Image Text:Share s ut

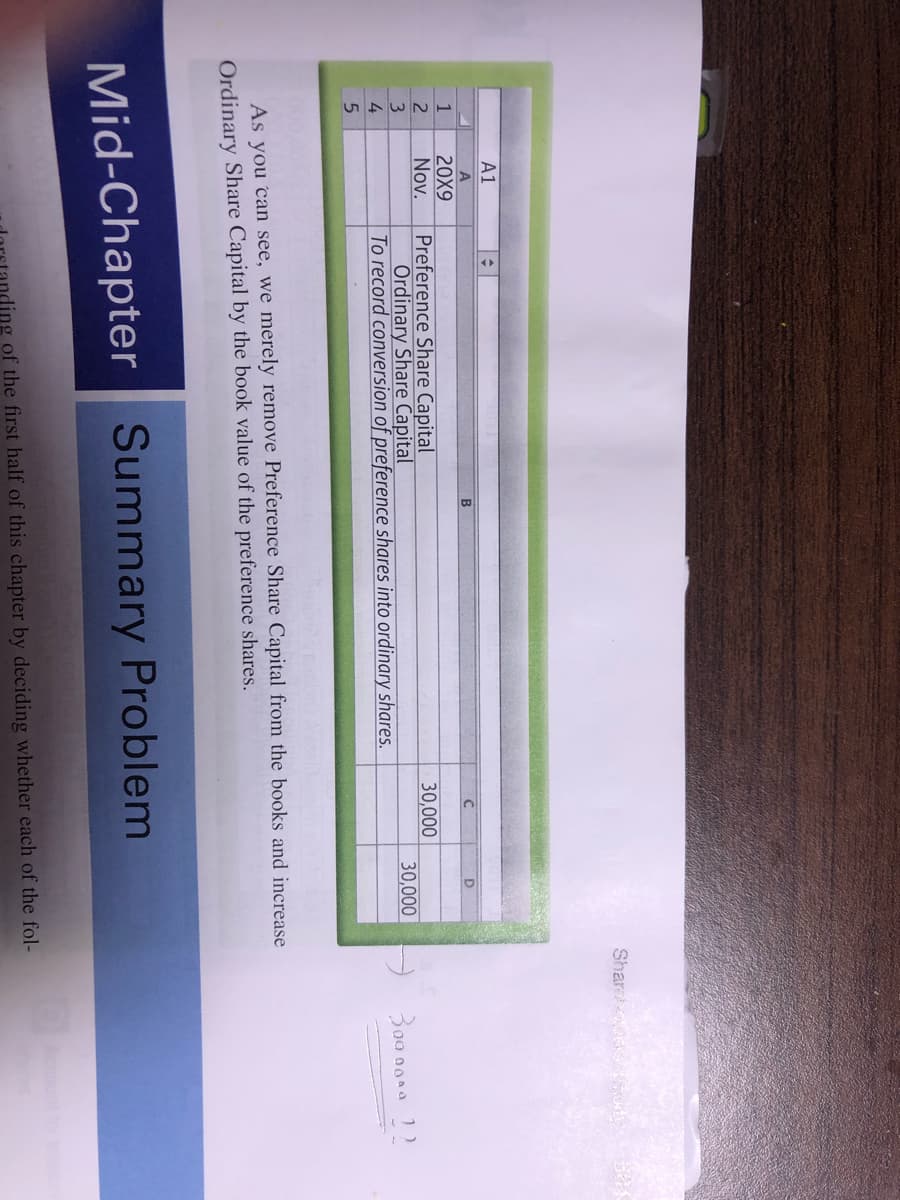

A1

20X9

Nov.

1

Preference Share Capital

Ordinary Share Capital

To record conversion of preference shares into ordinary shares.

30,000

3.

4

30,000

As you can see, we merely remove Preference Share Capital from the books and increase

Ordinary Share Capital by the book value of the preference shares.

Mid-Chapter Summary Problem

ling of the first half of this chapter by deciding whether each of the fol-

Transcribed Image Text:256655

Kes

uleni 10UR Prosperous and creditworthy. Gee-WhizZ looks debt-ree and appears to hay es

asset. Will you invest in this new business? Here are two takeaway lessons:

1. Some accounting values better represent the underlying economic phenomenon

2. Not all financial statements mean exactly what they say-compliance wit

standards and an audit by an independent CPA lend more credibility to the

porting process.

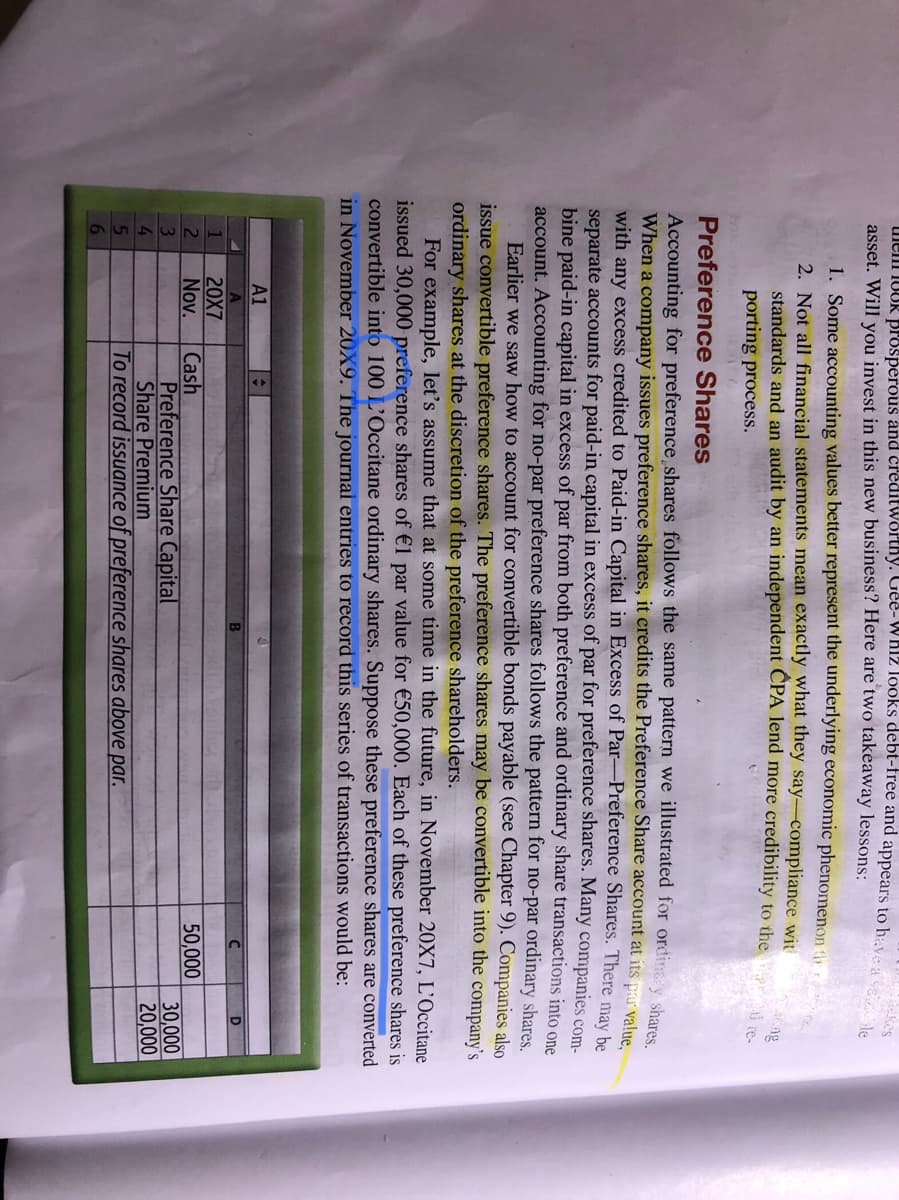

Preference Shares

Accounting for preference shares follows the same pattern we illustrated for ordina y shares

When a company issues preference shares, it credits the Preference Share account at its par valu

with any excess credited to Paid-in Capital in Excess of Par-Preference Shares. There may be

separate accounts for paid-in capital in excess of par for preference shares. Many companies com-

bine paid-in capital in excess of par from both preference and ordinary share transactions into one

account. Accounting for no-par preference shares follows the pattern for no-par ordinary shares.

Earlier we saw how to account for convertible bonds payable (see Chapter 9). Companies also

issue convertible preference shares. The preference shares may be convertible into the company's

ordinary shares at the discretion of the preference shareholders.

For example, let's assume that at some time in the future, in November 20X7, L'Occitane

issued 30,000 preference shares of €1 par value for €50,000. Each of these preference shares is

convertible into 100 L'Occitane ordinary shares. Suppose these preference shares are converted

in November 20X9. The journal entries to record this series of transactions would be:

A1

20X7

Nov.

50,000

Cash

Preference Share Capital

Share Premium

To record issuance of preference shares above par.

3

4.

30,000

20,000

6

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Business/Professional Ethics Directors/Executives…

Accounting

ISBN:

9781337485913

Author:

BROOKS

Publisher:

Cengage

Business/Professional Ethics Directors/Executives…

Accounting

ISBN:

9781337485913

Author:

BROOKS

Publisher:

Cengage