1. A basis for the systematic study of economics exists because A Resources are scarce in relation to material wants. B Governments interfere because there is always an efficient allocation of scarce resources. C ndividual economic actors never make rational economic decisions. D Resources are plentiful relative to wants, therefore an allocation problem arises. E The market consistently fails to allocate resources efficiently, thereby establishing the need to study economics. 2. The law of increasing opportunity cost is reflected in the shape of the A Production possibilities curve concave to the origin. B Production possibilities curve convex to the origin. C Horizontal production possibilities curve. D Straight- line production possibilities curve. E Upward-sloping production possibilities curve. 3. A production possibility frontier shows A The maximum combination of inputs that can be used to produce output in a typical economy. B The maximum revenue that can be generated from the sale of output produced by limited resources in an economy. C The minimum quantities of commodities that can be produced from limited but fully-employed resources in an economy. D The maximum quantities of commodities that can be produced from limited but fully-employed resources in an economy. E The quantities of factors of production available to produce goods and services in an economy.

1. A basis for the systematic study of economics exists because A Resources are scarce in relation to material wants. B Governments interfere because there is always an efficient allocation of scarce resources. C ndividual economic actors never make rational economic decisions. D Resources are plentiful relative to wants, therefore an allocation problem arises. E The market consistently fails to allocate resources efficiently, thereby establishing the need to study economics. 2. The law of increasing opportunity cost is reflected in the shape of the A Production possibilities curve concave to the origin. B Production possibilities curve convex to the origin. C Horizontal production possibilities curve. D Straight- line production possibilities curve. E Upward-sloping production possibilities curve. 3. A production possibility frontier shows A The maximum combination of inputs that can be used to produce output in a typical economy. B The maximum revenue that can be generated from the sale of output produced by limited resources in an economy. C The minimum quantities of commodities that can be produced from limited but fully-employed resources in an economy. D The maximum quantities of commodities that can be produced from limited but fully-employed resources in an economy. E The quantities of factors of production available to produce goods and services in an economy.

Principles of Economics 2e

2nd Edition

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:Steven A. Greenlaw; David Shapiro

Chapter2: Choice In A World Of Scarcity

Section: Chapter Questions

Problem 21CTQ: It is clear that productive inefficiency is a waste since resources are used in a way that produces...

Related questions

Question

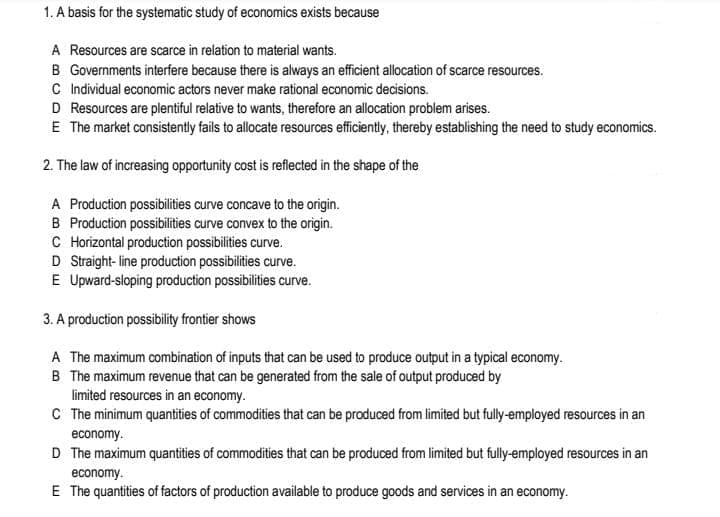

Transcribed Image Text:1. A basis for the systematic study of economics exists because

A Resources are scarce in relation to material wants.

B Governments interfere because there is always an efficient allocation of scarce resources.

C Individual economic actors never make rational economic decisions.

D Resources are plentiful relative to wants, therefore an allocation problem arises.

E The market consistently fails to allocate resources efficiently, thereby establishing the need to study economics.

2. The law of increasing opportunity cost is reflected in the shape of the

A Production possibilities curve concave to the origin.

B Production possibilities curve convex to the origin.

C Horizontal production possibilities curve.

D Straight-line production possibilities curve.

E Upward-sloping production possibilities curve.

3. A production possibility frontier shows

A The maximum combination of inputs that can be used to produce output in a typical economy.

B The maximum revenue that can be generated from the sale of output produced by

limited resources in an economy.

C The minimum quantities of commodities that can be produced from limited but fully-employed resources in an

economy.

D The maximum quantities of commodities that can be produced from limited but fully-employed resources in an

economy.

E The quantities of factors of production available to produce goods and services in an economy.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax