1. Summarize total assembly department costs for April 2017, and assign them to units completed (and transferred out) and to units in ending work in process. 2. What issues should a manager focus on when reviewing the equivalent units calculation?

1. Summarize total assembly department costs for April 2017, and assign them to units completed (and transferred out) and to units in ending work in process. 2. What issues should a manager focus on when reviewing the equivalent units calculation?

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter5: Support Department And Joint Cost Allocation

Section: Chapter Questions

Problem 1BE: Charlies Wood Works produces wood products (e.g., cabinets, tables, picture frames, and so on)....

Related questions

Question

can you solve it

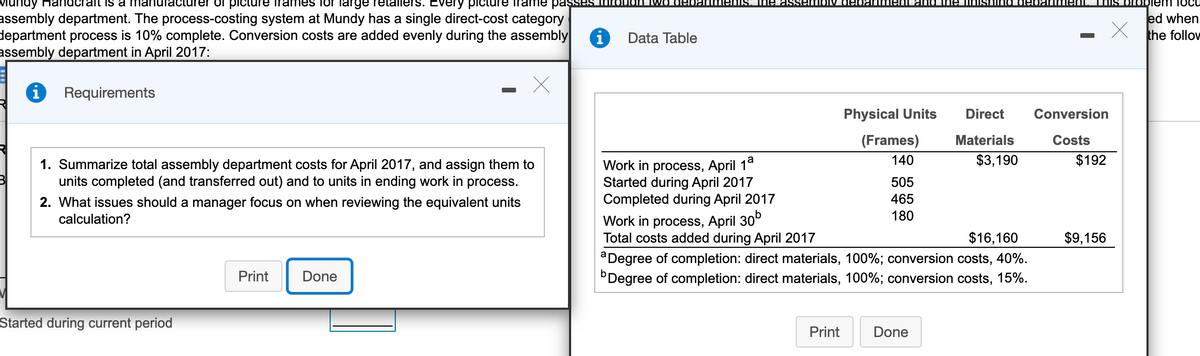

Transcribed Image Text:lundy Hanacraft is a nmanufacturer of picture frames for large retallers. Every picture frame pas

assembly department. The process-costing system at Mundy has a single direct-cost category

department process is 10% complete. Conversion costs are added evenly during the assembly

assembly department in April 2017:

GURE O ebart me

and tre

lem focu

ed when

the follov

i

Data Table

Requirements

Physical Units

Direct

Conversion

(Frames)

Materials

Costs

140

$3,190

$192

1. Summarize total assembly department costs for April 2017, and assign them to

units completed (and transferred out) and to units in ending work in process.

Work in process, April 1°

Started during April 2017

Completed during April 2017

505

2. What issues should a manager focus on when reviewing the equivalent units

465

calculation?

180

Work in process, April 30°

Total costs added during April 2017

$16,160

$9,156

aDegree of completion: direct materials, 100%; conversion costs, 40%.

'Degree of completion: direct materials, 100%; conversion costs, 15%.

Print

Done

Started during current period

Print

Done

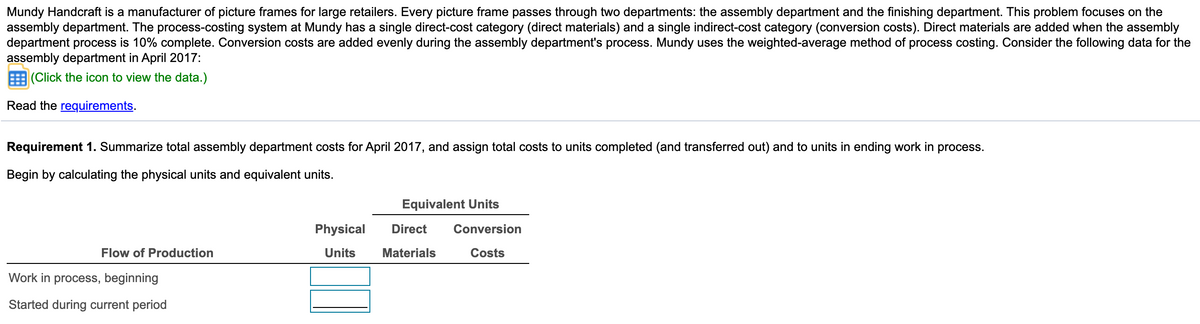

Transcribed Image Text:Mundy Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes through two departments: the assembly department and the finishing department. This problem focuses on the

assembly department. The process-costing system at Mundy has a single direct-cost category (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added when the assembly

department process is 10% complete. Conversion costs are added evenly during the assembly department's process. Mundy uses the weighted-average method of process costing. Consider the following data for the

assembly department in April 2017:

E (Click the icon to view the data.)

Read the requirements.

Requirement 1. Summarize total assembly department costs for April 2017, and assign total costs to units completed (and transferred out) and to units in ending work in process.

Begin by calculating the physical units and equivalent units.

Equivalent Units

Physical

Direct

Conversion

Flow of Production

Units

Materials

Costs

Work in process, beginning

Started during current period

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning