10. Fixed Proportions Production vigg - The long run supply curve of a perfectly competitive industry (LS) shows the minimum average cost for each level of industry output. Industry Q is the sum of the quantities (q) of the firms. Along LS, there is no incentive for entry or exit, as profits are zero. No firm has an incentive to alter its output, because each produces the q that minimizes its LRAC. > The LS for a constant cost industry is perfectly elastic (horizontal). The LS for an increasing cost industry is upward sloping, because as the industry grows, rising demand for inputs shifts up each firm's marginal and average cost curves. Note: The slope of LS for an industry is has nothing to do with economies of scale for firms in that industry. The whatnot industry employs three inputs: labor (L), capital (K), and land (G). The production function is fixed proportions: Q = min{10L, 10K, 10G} %3D Combining one unit each of L, K, and G produces Q = 10 whatnots. %3D Both L and K are perfectly elastically supplied. Input prices are: PL = $2 PK = $3 Growth in the output of the whatnot industry puts upward pressure on the price of land. The supply of the land input to industry X is: PG = .01Q %3D → Derive the long run industry supply schedule (LS). K G PG PGG PLL PkK TC MC LS 100 10 10 10 1 10 30 60 .60 > .80 200 20 20 20 40 300 400 500 20

10. Fixed Proportions Production vigg - The long run supply curve of a perfectly competitive industry (LS) shows the minimum average cost for each level of industry output. Industry Q is the sum of the quantities (q) of the firms. Along LS, there is no incentive for entry or exit, as profits are zero. No firm has an incentive to alter its output, because each produces the q that minimizes its LRAC. > The LS for a constant cost industry is perfectly elastic (horizontal). The LS for an increasing cost industry is upward sloping, because as the industry grows, rising demand for inputs shifts up each firm's marginal and average cost curves. Note: The slope of LS for an industry is has nothing to do with economies of scale for firms in that industry. The whatnot industry employs three inputs: labor (L), capital (K), and land (G). The production function is fixed proportions: Q = min{10L, 10K, 10G} %3D Combining one unit each of L, K, and G produces Q = 10 whatnots. %3D Both L and K are perfectly elastically supplied. Input prices are: PL = $2 PK = $3 Growth in the output of the whatnot industry puts upward pressure on the price of land. The supply of the land input to industry X is: PG = .01Q %3D → Derive the long run industry supply schedule (LS). K G PG PGG PLL PkK TC MC LS 100 10 10 10 1 10 30 60 .60 > .80 200 20 20 20 40 300 400 500 20

Chapter8: Perfect Competition

Section: Chapter Questions

Problem 2.4P

Related questions

Question

Given this practice question could I get help understanding how to fill out the table?

Transcribed Image Text:10.

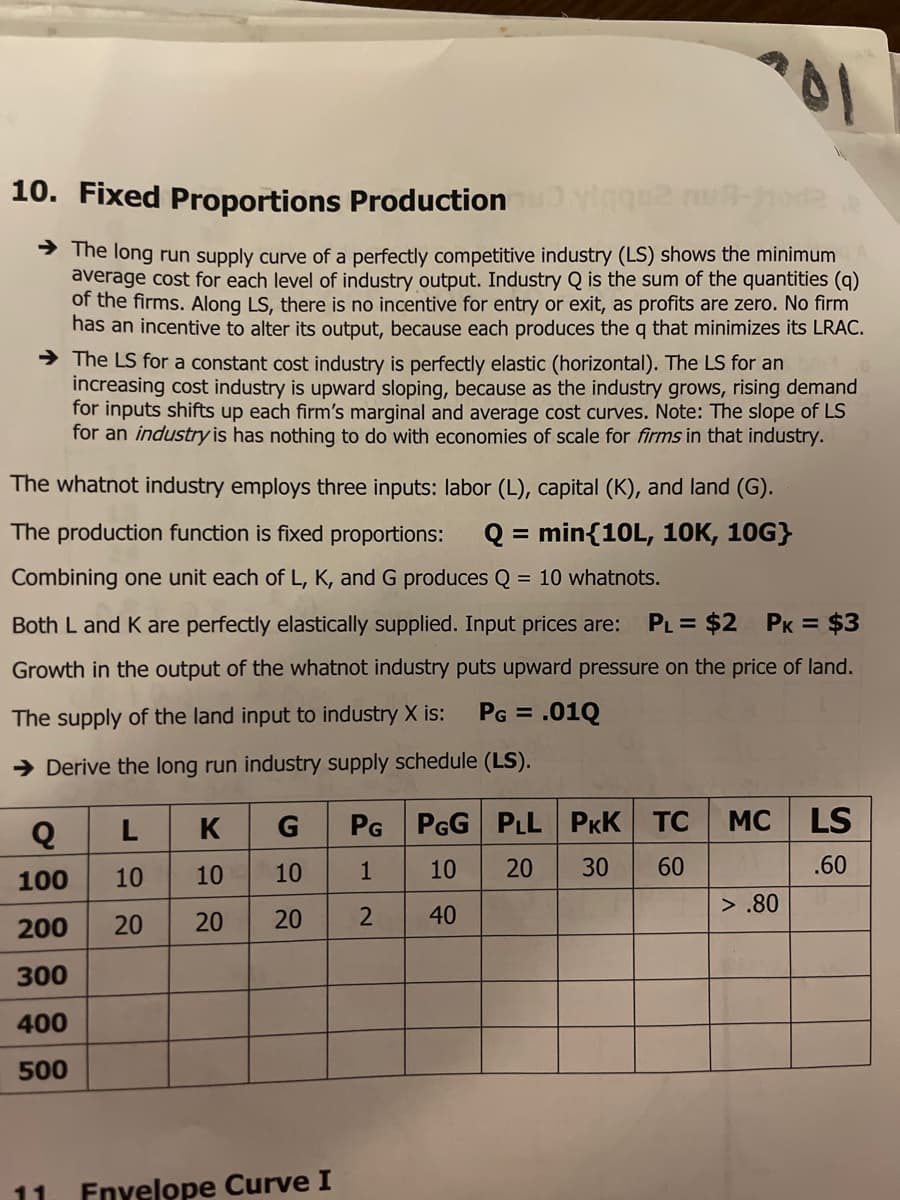

Fixed Proportions Production

> The long run supply curve of a perfectly competitive industry (LS) shows the minimum

average cost for each level of industry output. Industry Q is the sum of the quantities (q)

of the firms. Along LS, there is no incentive for entry or exit, as profits are zero. No firm

has an incentive to alter its output, because each produces the q that minimizes its LRAC.

> The LS for a constant cost industry is perfectly elastic (horizontal). The LS for an

increasing cost industry is upward sloping, because as the industry grows, rising demand

for inputs shifts up each firm's marginal and average cost curves. Note: The slope of LS

for an industry is has nothing to do with economies of scale for firms in that industry.

The whatnot industry employs three inputs: labor (L), capital (K), and land (G).

The production function is fixed proportions:

Q = min{10L, 10K, 10G}

Combining one unit each of L, K, and G produces Q = 10 whatnots.

Both L and K are perfectly elastically supplied. Input prices are:

PL = $2 PK = $3

Growth in the output of the whatnot industry puts upward pressure on the price of land.

The supply of the land input to industry X is:

PG = .01Q

→ Derive the long run industry supply schedule (LS).

L

K

G

PG

PGG

PLL PKK

TC

MC

LS

100

10

10

10

1

10

30

60

.60

> .80

200

20

20

20

2

40

300

400

500

11

Fnyelope Curve I

20

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Principles of Microeconomics

Economics

ISBN:

9781305156050

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning