12. Casillas, Inc. is a calendar-year corporation. Its financial statements for the years 2011 and 2010 contained errors as follows: 2010 Ending Inventory$3,000 overstated$8,000 overstated $2,000 understated$6,000 overstated 2011 Depreciation Expense Assume that no correcting entries were made at December 31, 2010, or December 31, 2011 and that no additional errors occurred in 2012. Ignoring income taxes, by how much will working capital at December 31, 2012 be overstated or understated? a. $0 b. $2,000 overstated c. $2,000 understated d. $5,000 understated

12. Casillas, Inc. is a calendar-year corporation. Its financial statements for the years 2011 and 2010 contained errors as follows: 2010 Ending Inventory$3,000 overstated$8,000 overstated $2,000 understated$6,000 overstated 2011 Depreciation Expense Assume that no correcting entries were made at December 31, 2010, or December 31, 2011 and that no additional errors occurred in 2012. Ignoring income taxes, by how much will working capital at December 31, 2012 be overstated or understated? a. $0 b. $2,000 overstated c. $2,000 understated d. $5,000 understated

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter22: Accounting For Changes And Errors.

Section: Chapter Questions

Problem 10MC: Shannon Corporation began operations on January 1, 2019. Financial statements for the years ended...

Related questions

Question

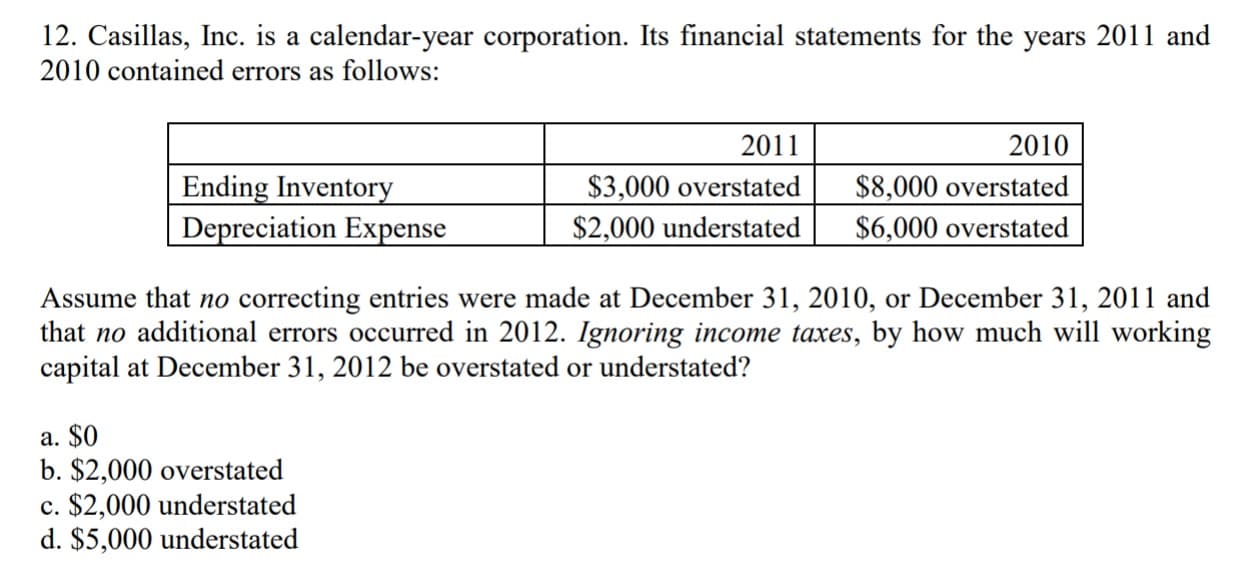

Transcribed Image Text:12. Casillas, Inc. is a calendar-year corporation. Its financial statements for the years 2011 and

2010 contained errors as follows:

2010

Ending Inventory$3,000 overstated$8,000 overstated

$2,000 understated$6,000 overstated

2011

Depreciation Expense

Assume that no correcting entries were made at December 31, 2010, or December 31, 2011 and

that no additional errors occurred in 2012. Ignoring income taxes, by how much will working

capital at December 31, 2012 be overstated or understated?

a. $0

b. $2,000 overstated

c. $2,000 understated

d. $5,000 understated

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College