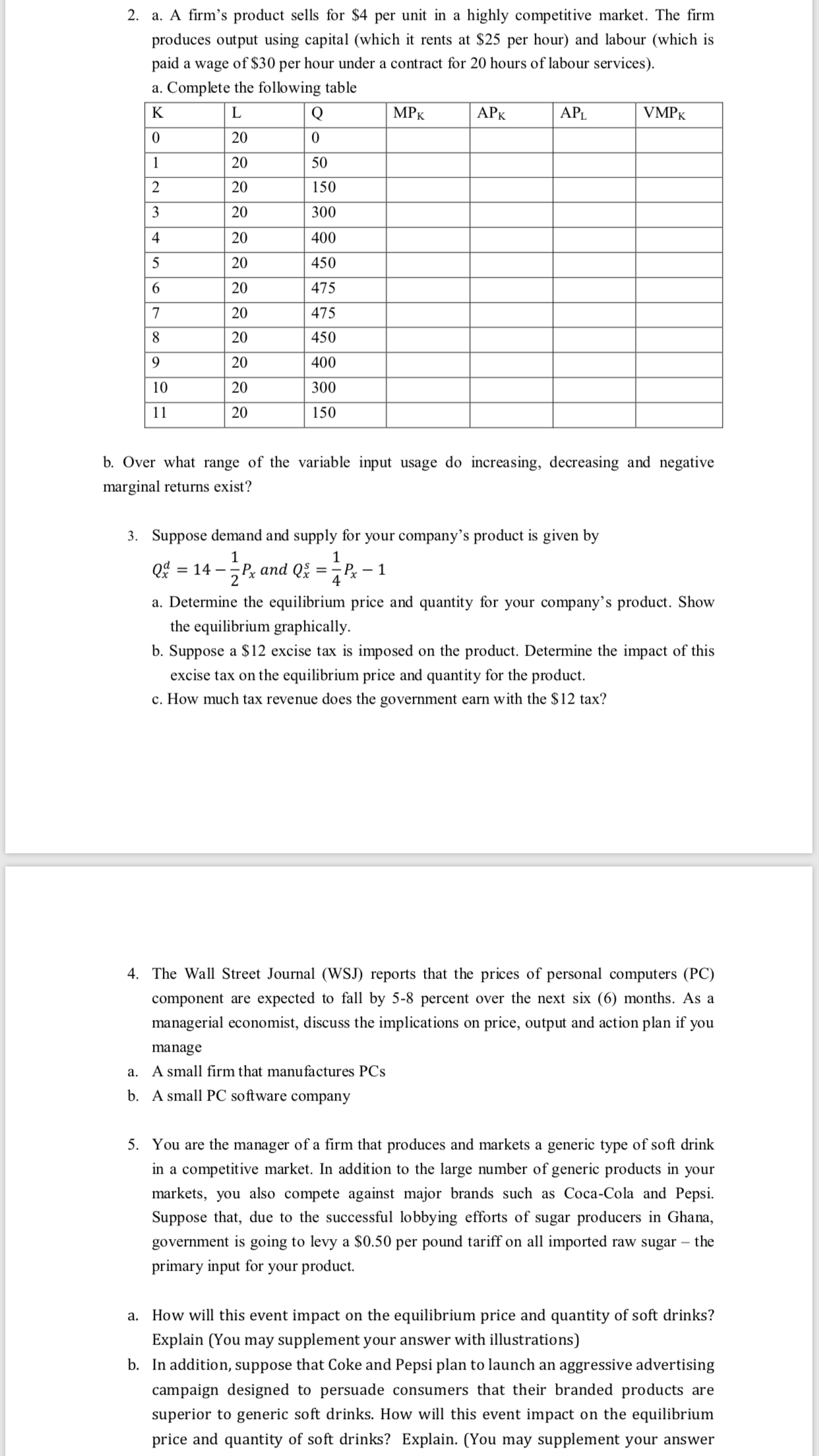

2. a. A firm's product sells for $4 per unit in a highly competitive market. The firm produces output using capital (which it rents at $25 per hour) and labour (which is paid a wage of $30 per hour under a contract for 20 hours of labour services). a. Complete the following table

Q: How does the impact of fixed costs change production decisions in the short run and in the long run?

A: A fixed cost(FC) is an expense that doesn't change with an expansion or reduction in the measure of…

Q: 2.6 Isabel runs her family's small pineapple processing plant, which takes fresh pineapples and cuts…

A: Cost of processing per pineapple Cost of processing total pineapple Machine maintenance per day…

Q: 5) Arswer the following questions based on the graph below: a)From point A to B and from B to C, is…

A: [a]From point A to B and from B to C, overall production is risingL rose from 80 to 140 to 280…

Q: Com 120.000 80.000 40.000 C A Robots 5.000 10.000 15.000 In the graph above, the resources in this…

A: The production possibility frontier of an economy shows the maximum amount of two goods that an…

Q: Question 3: Assume that there are two inputs that a car producer uses: 1 engine and 4 tires. 1 car…

A: Given , There are two inputs that a car producer uses : 1 engine and 4 tires 1 car is produced…

Q: A factory supervisor faces the following table: Quantity of laptops Labour cost ($) Rental of…

A: The term "average cost" refers to the production cost per unit, which is determined by dividing the…

Q: In the United States, where Internet services are cheap, the ratio of capital to labor used is…

A: Money is important in day to day life. Money has been developed since the ages and currently it is…

Q: 3. Explain why speed is important in the production process of the fashion industry, but why…

A: Fast fashion is a boon for retailers due to the constant introduction of new products encouraging…

Q: 6. Consider in this question that the market for truffles operates in a free market economy. The…

A: Q VC FC TC 0 21,000 10 80,000 20 2,10,000 30 3,10,000

Q: The table below presents the production quantity, total revenue, and total cost of a company in its…

A: A firm produces to maximizes profit and profit is the difference between the total revenue and total…

Q: How are the resource and product markets connected? A change in the product market affects the…

A: Resource market is where businesses purchase their resources in order to produce goods and services.…

Q: Suppose that firms in the zipper industry have the production technology: F(K,L)=4K^(3/4) * L^(1/4)…

A: Answer: Given: Production function: FK,L=4K34×L14 Cost/price of labor = 27 Cost/price of capital =??…

Q: 1) The joint cost (in thousands of euros) for two products X and Y can be given by the following…

A: We will use incremental cost concepts to answer this question

Q: Consider the following production chain for bread. Assume that a Farmer grows wheat, and sells this…

A: Value added is the difference in cost of a good or service when it moves from one stage to other.

Q: 2. An infinite number of sellers exist in this type of market. 3. It is a past expenditure that…

A: Factors of production are the inputs used in the process of production, these can be labor(L),…

Q: Explain the counter-intuitive proof of diminishing marginal productivity: if the law of diminishing…

A: Total product refers to the output amount that can be produced by a given amount of variable factor,…

Q: The oversupply of bananas in Mexico, which is recorded in the months of September and October,…

A: The increase in income that occurs from the sale of one more unit of production is known as marginal…

Q: Wheat 300 200 100 100 200 300 400 Soybeans Refer to Figure 2-7. In order to move from Point C to…

A: Opportunity cost refers to the additional cost or foregone income of an individual or firm when…

Q: Suppose that you operate a business that produces widgets. What's a widget? A widget is a…

A: The total cost is the sum of fixed cost and variable cost. The fixed cost (FC) is the cost of fixed…

Q: 1. (Production) Jasmine has just inherited a restaurant. In the short run, she has to stick with the…

A: The short-run is a notion that states that at least one input is fixed while the others are variable…

Q: A firm's product sells for $4 per unit in a highly competitive market. The firm produces output…

A: Competitive market: It refers to the market under which there are many firms that are available and…

Q: Use the following information to answer the questions below Computers: Soybeans: Total revenue =…

A: The rental rate of capital refers to the price one needs to pay in order to obtain capital from the…

Q: What level of output does a firm produce?

A: The quantity of products and services produced in a particular time period is referred to as output…

Q: Short Answer 12) Using the following table, which of the production choices (a, b, c, d, e) are…

A: Note: The last row values were not clearly visible. Production technique o/p capital labour A…

Q: Show why the cycle of productive capital P… M’- D’-M… P expresses the formula for the simple…

A: Productive capital is the physical capital that includes both the advanced and consumed labor power,…

Q: 5. Given the following, complete the box and show calculations. Also draw the following graphs based…

A: Marginal Physical Product(MPP)=Change in Output(TP)/Change in Variable Input Average Fixed…

Q: What are the short-run and long-run costs of the production of Walmar

A: There are various costs incurred by a firm during its production process and even in the pre and…

Q: An economy can produce leather using labor and capital and wheat using labor and land. The total…

A: In the business examination, the production possibility frontier (PPF) is a bend showing the…

Q: 2. A firm is using 7 units of labor and 100 units of capital to produce 1000 units of goods. At…

A: Cost of labour is $15 per unit but quantity is less Cost of capital is $2 but quantity is more

Q: 2.In order to maximize profits, a firm will produce output where (check all that apply) a. total…

A: A firm produces output(Y) till the profit(π) is maximum. The profit(π) is the difference between…

Q: Explain the absence of economic profit in a purely competitive, static economy. Realizing that the…

A: In a purely competitive economy, there are large number of buyers and sellers and each firm sells…

Q: QUESTION 15 A perfectly competitive firm produces digital devices using capital and labour. The wage…

A: Marginal cost refers to the cost of generating or consuming an additional unit of output by the…

Q: Which stage of short run production is efficient? Why?

A: In microeconomics, we have two time periods namely short run and long run. Short run is the time…

Q: 5. Your aunt is thinking about opening a hardware store. She estimates that it would cost $500 000…

A: a.Opportunity cost is the value of the next best alternative that we foregone while making a…

Q: What is under allocation of resources?

A: Since you have asked multiple questions, we will solve the first question for you. If you want any…

Q: 5) Why is a firm willing to produce at a loss in the short run if the loss is no greater than the…

A: Costs refers to the amount of money involved in the production process to produce the goods and…

Q: 1. Figure 1 shows the production function of a firm. Y Y2 Y1 X1 X2 a) What are the variables along…

A: Note: Since we only answer up to 3 sub-parts, we’ll answer the first 3. Please resubmit the question…

Q: Profit maximization may not be the goal of a business firm. What other goals might a business…

A: Profit maximization is one of the goal of business.

Q: What are the items that make opportunity cost differ from the accountant's measure of cost? A firm's…

A: A firm's opportunity cost is the cost foregone in terms of the next best alternative to pursue the…

Q: 7. For the following industries, state whether the long-run average cost curve has an extended range…

A: Handcrafting work are critical as far as monetary turn of events. They provide plenty of job…

Q: In a perfectly competitive market, a firm’s production in the market described as Q = f(X) = 5X0.5 ,…

A:

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 1 images

- If two painters can paint 200 square feet of wall in an hour, and three painters can paint 275 square feet, what is the marginal product of the third painter?4) A firm faces a production function of twittle-twaps: Q(K,Lp,Ln) = 5*K(2/5)*LP(1/3)*LN(1/5) per hour, where capital (K), production labor (LP), and non-production labor (LN) are input factors used in production. The firm operates in a competitive market, where they are a price taker within the capital & labor markets and its own price (r = 40, wP = 25, wN = 50, P = 20). Answer the following.a. If capital and non-production labor are fixed at K = 32 and LN = 243, what is the general form MPLP and graph Q wrt to LP changing [you do not need to solve for LP yet].b. Is this production function decreasing, constant, or increasing returns to scale and why.c. Given the wage of production workers and the price of twittle-twaps, what is the optimal number of LP to employ to maximize profits and the quantity produced (VMPLP = wP).d. If the firm can control both K and LP, what does the Isoquant curve look like and its slope in relative terms if LN is fixed at 243 units [IQ slope =…4) A firm faces a production function of twittle-twaps: Q(K,Lp,Ln) = 5*K(2/5)*LP(1/3)*LN(1/5) per hour, where capital (K), production labor (LP), and non-production labor (LN) are input factors used in production. The firm operates in a competitive market, where they are a price taker within the capital & labor markets and its own price (r = 40, wP = 25, wN = 50, P = 20). Answer the following.a. If capital and non-production labor are fixed at K = 32 and LN = 243, what is the general form MPLP and graph Q wrt to LP changing [you do not need to solve for LP yet].b. Is this production function decreasing, constant, or increasing returns to scale and why.c. Given the wage of production workers and the price of twittle-twaps, what is the optimal number of LP to employ to maximize profits and the quantity produced (VMPLP = wP).d. If the firm can control both K and LP, what does the Isoquant curve look like and its slope in relative terms if LN is fixed at 243 units [IQ slope =…

- 4. For each of the following production functions, write the equation and graph the supply curve of the firm if w=20 and r=50 When the price of output is $20, how much will the firm offer to the market and what are the profits of the firm? a. Q = 10 K^.2L^.5B^.1 in the long-run with capital flexible. B is the amount of Building Space employed, which is held fixed at 1 unit in both the long-run and the short-run and has a price of $100 per unit. b. Q= (4K^.6 + 8L^.6)^ 1.256 workers and 4 machines are required to produce 2 computers. 2 workers and 2 machines are required to produce 2 units of tomato. A. Find the labor and capital requirement per one computer and 1 unit of tomato? B. Which industry is a labor intensive? Capital intensive?2. Thor runs a business called Heavy Hammers, which produces some of the heaviest hammers you’ve ever seen! He uses two inputs in the production of hammers: labour, denoted by L, and capital, denoted by K. Heavy Hammers produces hammers, denoted by H, according to the following production technology: H = f(L,K) = L12 K14 . Thor must pay each unit of labour a wage rate w and is able lease his capital equipment at r dollars per unit. The market price of hammers is $4. (a) Write down Thor’s profit maximization problem. (b) Write down and equation that sets the marginal product of labour equal to the wage rate of labour, w. Then write down and equation that sets the marginal product of capital equal to the lease rate, r. 2 (c) Solve the two equations from part (b) for the two unknown inputs L and K. Your solutions give the profit-maximizing choices of labour and capital as functions of the wage and lease rates, w and r. (d) If the wage is 2, and the lease rate is 1, how…

- Only typed answer and please don't use chatgpt How does the market for inputs like labor differ from the market for goods and services? (Check all that apply.) Part 2 A. Firms are sellers in the market for goods and services, while individuals are sellers in the market for inputs. B. The demand for inputs is derived from the demand for final goods and services. C. Firms are buyers in the market for inputs, while individuals are buyers in the market for goods and services. D. The market for inputs resolves shortages and surpluses through government-supervised negotiations.Q5. A bicycle manufacturer in China currently employs 40 production workers and five supervisors and produces . The marginal product of the last production worker employed is 60 units of output per hour, and production workers are paid 50 CNY per hour. The marginal product of the last supervisor employed is 120 units of output per hour, and supervisors are paid 80 CNY per hour. i. If the firm produced 2,100 bicycles per month before the last production worker was hired, how many bicycles does it produce now? ii. Assume that the firm's isoquants are smooth curves and that labor hours can be varied continuously. Is the firm producing the maximum level of bicycles given its current level of cost? Explain why or why not. If it isn't, explain what it should do to increase output.5:23 The amount that a firm pays for all of the inputs that go into producing goods and services is the: O average cost. O total revenue. O total price. O total cost.

- H6. Your mother owns and runs an arts and craft store, and the business is doing well. She would have otherwise been employed as a high school geography teacher making $80,000 a year or as an interior decorator making $68,000 a year. She owns the building in which her shop is located, which she could have rented out for $24,000 a year. Her annual revenue from the shop is $430,000 and she employs four workers, each of whom earns $30,000 a year. On average, she spends $206,000 per year traveling, purchasing, and shipping unique merchandise for resale at her store. Based on this information, do you think you should encourage her to return to teaching? Explain your advice with the help of calculations on her opportunity costs, accounting profit, and economic profit.Explain with the help of Graphs of Total Product (TP) and Marginal product (MP) the three laws of variable proportions and their significance in Industry and agriculture. Give the relationship between TP and MP at different stages of variable proportions. What is the relationship between Average Product curve (AP) and marginal product curve (MP) and explain at what point a progressive firm should change its labor or capital inputs with more skilled labor or with new technological machine in order to remain comparative in the market. What would happen to its product in the market if it does not change its machines or if it changes all its machines at the same timeI plan to reopen a business consists of five kiosks for serving the customers who come to service their Phones. In this case, I must hir five Professional workers.So here, we can regard the kiosk and workers as the input and the serviceable phones as output. IN five kiosks = I can serve a total of 100 customers every week. But the expectons we will facing 150 customers daily for servicing their Phones.So, to serve all the customers, if I -rent five more kiosks to do the needful and also , hir additional five Professional workers. 1- How to exhibit increasing returns To Scale?2- How to exhibit decreasing Returns To Scale3- How to exhibit Constant returns to scale? Please make sure to include an adequate explanation as to why this is true.