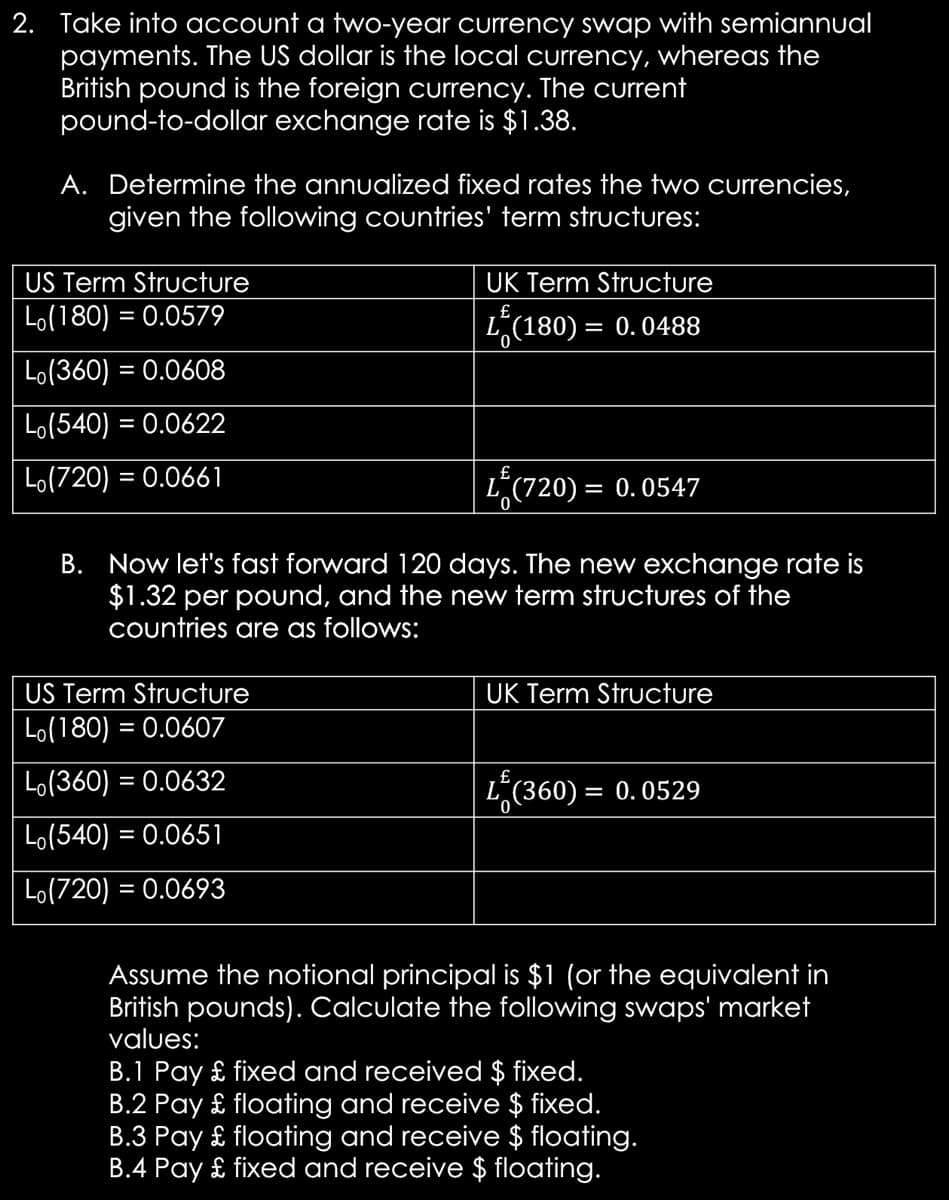

2. Take into account a two-year currency swap with semiannual payments. The US dollar is the local currency, whereas the British pound is the foreign currency. The current pound-to-dollar exchange rate is $1.38. A. Determine the annualized fixed rates the two currencies, given the following countries' term structures: US Term Structure Lo(180) = 0.0579 Lo(360) = 0.0608 Lo(540) = 0.0622 Lo(720) = 0.0661 UK Term Structure L (180) = 0.0488 L(720) = 0.0547 B. Now let's fast forward 120 days. The new exchange rate is $1.32 per pound, and the new term structures of the countries are as follows: US Term Structure Lo(180) = 0.0607 Lo(360) = 0.0632 Lo(540) = 0.0651 Lo(720) = 0.0693 UK Term Structure L(360) = 0.0529 Assume the notional principal is $1 (or the equivalent in British pounds). Calculate the following swaps' market values: B.1 Pay £ fixed and received $ fixed. B.2 Pay £ floating and receive $ fixed. B.3 Pay £ floating and receive $ floating. B.4 Pay £ fixed and receive $ floating.

2. Take into account a two-year currency swap with semiannual payments. The US dollar is the local currency, whereas the British pound is the foreign currency. The current pound-to-dollar exchange rate is $1.38. A. Determine the annualized fixed rates the two currencies, given the following countries' term structures: US Term Structure Lo(180) = 0.0579 Lo(360) = 0.0608 Lo(540) = 0.0622 Lo(720) = 0.0661 UK Term Structure L (180) = 0.0488 L(720) = 0.0547 B. Now let's fast forward 120 days. The new exchange rate is $1.32 per pound, and the new term structures of the countries are as follows: US Term Structure Lo(180) = 0.0607 Lo(360) = 0.0632 Lo(540) = 0.0651 Lo(720) = 0.0693 UK Term Structure L(360) = 0.0529 Assume the notional principal is $1 (or the equivalent in British pounds). Calculate the following swaps' market values: B.1 Pay £ fixed and received $ fixed. B.2 Pay £ floating and receive $ fixed. B.3 Pay £ floating and receive $ floating. B.4 Pay £ fixed and receive $ floating.

Managerial Accounting: The Cornerstone of Business Decision-Making

7th Edition

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Chapter13: Emerging Topics In Managerial Accounting

Section: Chapter Questions

Problem 47E: Match each term in Column A with its related definition in Column B. Column A 1. ____________ Spot...

Related questions

Question

Transcribed Image Text:2. Take into account a two-year currency swap with semiannual

payments. The US dollar is the local currency, whereas the

British pound is the foreign currency. The current

pound-to-dollar exchange rate is $1.38.

A. Determine the annualized fixed rates the two currencies,

given the following countries' term structures:

US Term Structure

UK Term Structure

Lo(180) = 0.0579

L(180) = 0.0488

%3D

Lo(360) = 0.0608

Lo(540) = 0.0622

Lo(720) = 0.0661

L(720):

= 0. 0547

B. Now let's fast forward 120 days. The new exchange rate is

$1.32 per pound, and the new term structures of the

Countries are as follows:

US Term Structure

UK Term Structure

Lo(180) = 0.0607

%3D

Lo(360) = 0.0632

L*(360) = 0.0529

Lo(540)

= 0.0651

Lo(720) = 0.0693

Assume the notional principal is $1 (or the equivalent in

British pounds). Calculate the following swaps' market

values:

B.1 Pay £ fixed and received $ fixed.

B.2 Pay £ floating and receive $ fixed.

B.3 Pay £ floating and receive $ floating.

B.4 Pay £ fixed and receive $ floating.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 6 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning