Financial Accounting

14th Edition

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Carl Warren, Jim Reeve, Jonathan Duchac

Chapter8: Sarbanes-oxley, Internal Control, And Cash

Section: Chapter Questions

Problem 18E

Related questions

Question

These are the answers to the solution manual:

24.P430,000

25.P350,000

26.P11,350

27.P836,350

28. P836,350

Are these really the correct answers? Please show the computation from 24-28 please, thank you!

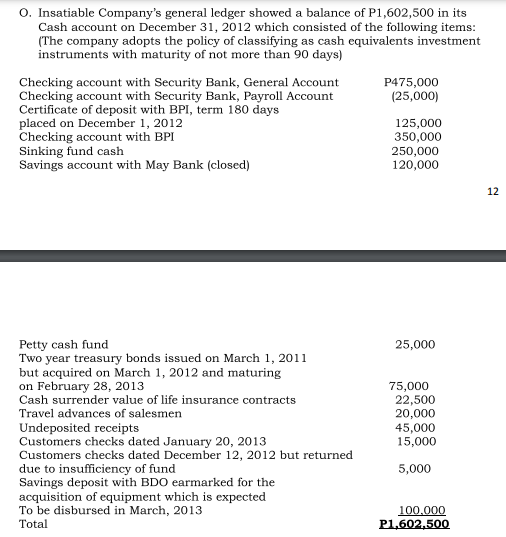

Transcribed Image Text:O. Insatiable Company's general ledger showed a balance of P1,602,500 in its

Cash account on December 31, 2012 which consisted of the following items:

(The company adopts the policy of classifying as cash equivalents investment

instruments with maturity of not more than 90 days)

Checking account with Security Bank, General Account

Checking account with Security Bank, Payroll Account

Certificate of deposit with BPI, term 180 days

placed on December 1, 2012

Checking account with BPI

Sinking fund cash

Savings account with May Bank (closed)

P475,000

(25,000)

125,000

350,000

250,000

120,000

12

Petty cash fund

Two year treasury bonds issued on March 1, 2011

but acquired on March 1, 2012 and maturing

on February 28, 2013

Cash surrender value of life insurance contracts

25,000

75,000

22,500

20,000

45,000

15,000

Travel advances of salesmen

Undeposited receipts

Customers checks dated January 20, 2013

Customers checks dated December 12, 2012 but returned

due to insufficiency of fund

Savings deposit with BDO earmarked for the

acquisition of equipment which is expected

5,000

To be disbursed in March, 2013

Total

100.000

P1,602,500

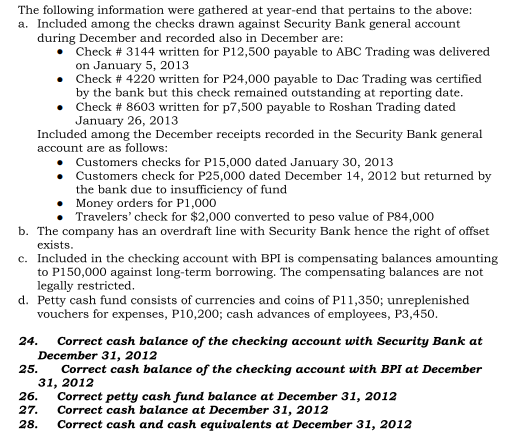

Transcribed Image Text:The following information were gathered at year-end that pertains to the above:

a. Included among the checks drawn against Security Bank general account

during December and recorded also in December are:

Check # 3144 written for P12,500 payable to ABC Trading was delivered

on January 5, 2013

• Check # 4220 written for P24,000 payable to Dac Trading was certified

by the bank but this check remained outstanding at reporting date.

Check # 8603 written for p7,500 payable to Roshan Trading dated

January 26, 2013

Included among the December receipts recorded in the Security Bank general

account are as follows:

Customers checks for P15,000 dated January 30, 2013

Customers check for P25,000 dated December 14, 2012 but returned by

the bank due to insufficiency of fund

Money orders for P1,000

Travelers' check for $2,000 converted to peso value of P84,000

b. The company has an overdraft line with Security Bank hence the right of offset

exists.

c. Included in the checking account with BPI is compensating balances amounting

to P150,000 against long-term borrowing. The compensating balances are not

legally restricted.

d. Petty cash fund consists of currencies and coins of P11,350; unreplenished

vouchers for expenses, P10,200; cash advances of employees, P3,450.

Correct cash balance of the checking account with Security Bank at

December 31, 2012

Correct cash balance of the checking account with BPI at December

31, 2012

Correct petty cash fund balance at December 31, 2012

Correct cash balance at December 31, 2012

Correct cash and cash equivalents at December 31, 2012

24.

25.

26.

27.

28.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,