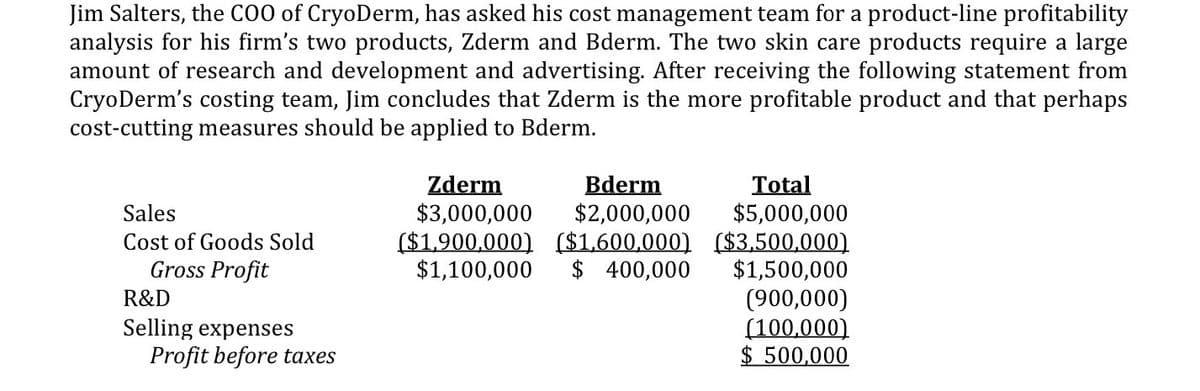

Briefly explain why Jim may be wrong in his assessment of the relative performance of the two products

Q: The cost of quality are costs incurred to prevent, or costs arising as a result of, the production…

A: The cost of quality are costs incurred to prevent, or costs arising as a result of, the production…

Q: Which of the following is not a qualitative decision that should be considered in an outsourcing…

A: Outsourcing refers to receiving of services from another company in order to fulfill out company…

Q: What does the following sentence mean? "It is critical to define your product while considering the…

A: "It is critical to define your items before taking into consideration the responses of rivals."When…

Q: The cost of lost future sales after a customer finds a defect in a product is which type of quality…

A: a) Prevention costs: Prevention costs are incurred to avoid quality problems and are incurred to…

Q: hese issues associated with using accounting measures as performance measures through use of…

A: The answer has been mentioned below.

Q: Which of the following statements is true regarding CVP analysis? Select one: A. CVP is only useful…

A: Fixed Cost: The fixed cost is a a type of cost that remains constant whether the activity level of…

Q: a difference in cost-plus pricing and target costing is that target costing starts with the price…

A: Target costing says that first target selling price is calculated, then markup is deducted from…

Q: limitations to employing the PE Ratio for company to company comparisons. Describe several of the…

A: The Price Earnings Ratio which is commonly referred as P/E ratio or PER. It is the ratio which is…

Q: The cost of lost future sales after a customer finds a defect in a product is which type of quality…

A:

Q: Does having a positive Contribution Margin always indicate that it is better to continue operations…

A: Contribution Margin is calculated by deduction variable costs from the sales revenue.

Q: Assume that ABC Company planned to conduct the market survey to know the opinions of the customers…

A: There are different types of costing method which are available to determine the required profit of…

Q: Consultant Frank Alvarez recently commented that the mostcommon error made by his clients is…

A: Given case is: Consultant Frank Alvarez recently commented that the mostcommon error made by his…

Q: A decision about one product is said to have ________ effects when a change in the sales of one…

A: A decision about one product is said to have ________ effects when a change in the sales of one…

Q: Prime indicators of problems with a conventional costing system include company profits being eroded…

A: Product cost refers to the cost or expense which is incurred for creating the product and this cost…

Q: When standard costs are used in applying the cost-plus approach to product pricing, the standards…

A: False No, the standards should not be based upon normal levels of performance.

Q: Which of the following decreases the non-value added time of producing a product and in turn…

A: Subassemblies service:It is a service offered by the manufacturer who do not have adequate time and…

Q: As a result of cost distortion, some products will be overcosted while other products will be…

A: Solution: Cost distortions occurs when the overhead costs are not properly allocated, when the…

Q: What is customer value? Choose the correct. A. Ratio between the customer's perceived benefits…

A: A customer is an entity that buys goods or services from third parties. Accumulating a profitable…

Q: Distinguish how SFS could use Target Costing and Kaizen Costing to improve its future performance.…

A: Target Costing and Kaizen Costing to improve its future performance by the following manner –…

Q: The main categories of income statement for a manufacturer includes the following, except a. Direct…

A: We’ll answer the first question since the exact one wasn’t specified. Please submit a new question…

Q: To determine if a performance obligation exists, A. none of the alternatives are correct. B.…

A: Introduction: Performance obligation: Rendering service or delivering the goods are pending , its a…

Q: QUESTION 1 Match the type of company and its most likely pricing approach given the company sells…

A: Cost-Plus Pricing Strategy: Retailers frequently use this pricing approach to set prices. Cost-plus…

Q: Wrong allocation of common costs lead to A. Inaccurate estimation of cost of products or…

A: Common costs are those costs that are incurred for two or more products simultaneously. Common costs…

Q: Which of the following is not true regarding continuous improvement?A. It applies to both service…

A: Continuous Improvement means business or process should be improving on regular or continuous basis.…

Q: Which of the following is a false statement about scrap and by-products? Select one: a. Both scrap…

A: Scrap is the incidental residue from material used in production activities that can be recovered…

Q: Give two examples of nonnancial measures of customer satisfaction relating to quality.

A:

Q: Which statement is FALSE about product-market fit?

A: Product market fit is a strategy to find which product caters to the demand of the market. It is…

Q: Which of the following statements is true with respect to the performance metrics useful for…

A: In production process, the ratio of direct labor should be more than the indirect labor. An ideal…

Q: Which of the following statements is not true regarding the use of variable and absorption costing…

A: Answer: Option d.

Q: Please explain the statement below thourougly with an example to illustrate the answer.

A: The statement "A product with a high gross profit could be an unprofitable product" is false as a…

Q: If the company is successful in achieving challenging targets for the performance measures of…

A: On-time delivery – 3 types of performance measures would be Percentage of orders that were…

Q: Which of the following is not a qualitative decision that should be considered in an outsourcing…

A: Qualitative decisions are more subjective since they are based on elements other than numerical…

Q: Explain why a new product costing system may be needed when line managers suggest that an apparently…

A: Product Costing System:-It is a framework that is used to determine the cost of the product for…

Q: Which of the following statements regarding activity-based costing (ABC) is false? A. ABC is…

A: Overheads are the indirect cost involved in the production process of the company. It is charged to…

Q: Which of the following statements is TRUE? Joint product allocation results in more accurate…

A: Joint products are multiple products which are produced within a single process that means they…

Q: Which of the following is not a qualitative factor that Atlas Manufacturing should consider when…

A: A make-or-buy decision is a strategic choice made by the management between producing an item…

Q: What kinds of challenges occurs in the Cost Control and Cost Reduction in the Manufacturing conce

A: Cost Control is different from cost reduction Cost Control focuses/emphasizes on decreasing the…

Q: Describe an adverse selection problem a company is facing. What is the source of the asymmetric…

A: When one party in a transaction has more or better information than another. Generally, this type of…

Q: 1. What is the financial advantage (disadvantage) of further processing each of the three products…

A: The question is related Process Costing. Joint cost is that cost which is incurred in making of…

(i) Briefly explain why Jim may be wrong in his assessment of the relative performance of the two products

Step by step

Solved in 2 steps

- Salem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs. In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.) All depreciation. The following activity data were also gathered: Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on). Engineering also provided the following additional estimates for the proposed product line: Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of 26 and just 18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line. Required: 1. Reproduce Bettys break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold? 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units. 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?Kagle design engineers are in the process of developing a new green product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed 550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit-and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system: Variable conversion activity rate: 100 per direct labor hour Material usage rate: 20 per part ABC system: Labor usage: 15 per direct labor hour Material usage (direct materials): 20 per part Machining: 75 per machine hour Purchasing activity: 150 per purchase order Setup activity: 3,000 per setup hour Warranty activity: 500 per returned unit (usually requires extensive rework) Customer repair cost: 25 per repair hour (average) Required: 1. Select the lower-cost design using unit-based costing. Are logistical and post-purchase activities considered in this analysis? 2. Select the lower-cost design using ABC analysis. Explain why the analysis differs from the unit-based analysis. 3. What if the post-purchase cost was an environmental contaminant and amounted to 10 per unit for Design A and 40 per unit for Design B? Assume that the environmental cost is borne by society. Now which is the better design?Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?

- Moisha is developing material standards for her company. The operations manager wants grade A widgets because they are the easiest to work with and are the quality the customers want. Grade B will not work because customers do not want the lower grade, and it takes more time to assemble the product than with grade A materials. Moisha calls several suppliers to get prices for the widget. All are within $0.05 of each other. Since they will use millions of widgets, she decides that the $0.05 difference is important. The supplier who has the lowest price is known for delivering late and low-quality materials. Moisha decides to use the supplier who is $0.02 more but delivers on time and at the right quality. This supplier charges $0.48 per widget. Each unit of product requires four widgets. What is the standard cost per unit for widgets?Abernathy, Inc., produces two different generators and is concerned about their quality. The company has identified the following quality activities and costs associated with the two products: Required: 1. Calculate the quality cost per unit for each product, and break this unit cost into quality cost categories. Which of the two seems to have the lowest quality? 2. How might a manager use the unit quality cost information?The Chocolate Baker specializes in chocolate baked goods. The firm has long assessed the profitability of a product line by comparing revenues to the cost of goods sold. However, Barry White, the firms new accountant, wants to use an activity-based costing system that takes into consideration the cost of the delivery person. Following are activity and cost information relating to two of Chocolate Bakers major products: Using activity-based costing, which of the following statements is correct? a. The muffins are 2,000 more profitable. b. The cheesecakes are 75 more profitable. c. The muffins are 1,925 more profitable. d. The muffins have a higher profitability as a percentage of sales and, therefore, are more advantageous.

- Jim Salters, the COO of CryoDerm, has asked his cost management team for a product-line profitability analysis for his firm’s two products, Zderm and Bderm. The two skincare products require a large amount of research and development and advertising. After receiving the following statement fromCryoDerm’s costing team, Jim concludes that Zderm is the more profitable product and that perhaps cost-cutting measures should be applied to Bderm. Zderm Bderm Total Sales $3,000,000 $2,000,000 $5,000,000 Cost of Goods Sold ($1,900,000) ($1,600,000) ($3,500,000) Gross Profit $1,100,000 $ 400,000 $1,500,000 R&D (900,000) Selling expenses (100,000) Profit before taxes $ 500,000 Required:(i) Briefly explain why Jim may be wrong in his assessment of the relative performance of the twoproducts. (ii) Suppose that 80% of the R&D and selling expenses are traceable to Zderm. Prepare life-cycle income statements for each product. What does this indicate…Ken Yalters, the COO of FreshSkin, asked his cost management team for a product line profitability analysis for his firm's two products - Askin and Bskin. The two products are skin care products that require a large amount of research and development and advertising. He received the report below. Ken concluded that Askin was the more profitable product, and that perhaps cost-cutting measures should be applied to the Bskin product. Askin Bskin Total Sales $ 4,011,000 $ 2,605,500 $ 6,616,500 Cost of goods sold (2,605,500 ) (2,111,000 ) (4,716,500 ) Gross profit $ 1,405,500 $ 494,500 $ 1,900,000 Research and development (1,181,000 ) Selling expenses (135,500 ) Profit before taxes $ 583,500 Seventy-five percent of the research and development and selling expenses were traceable to Askin.Profit before taxes for the Bskin product, per life-cycle income statements, is:Danna Lumus, the marketing manager for a division that produces a variety of paper products, is considering the divisional manager’s request for a sales forecast for a new line of paper napkins. The divisional manager has been gathering data so that he can choose between two different production processes. The first process would have a variable cost of $10 per case produced and total fixed cost of $100,000. The second process would have a variable cost of $6 per case and total fixed cost of $200,000. The selling price would be $30 per case. Danna had just completed a marketing analysis that projects annual sales of 30,000 cases. Danna is reluctant to report the 30,000 forecast to the divisional manager. She knows that the first process would be labor intensive, whereas the second would be largely automated with little labor and no requirement for an additional production supervisor. If the first process is chosen, Jerry Johnson, a good friend, will be appointed as the line supervisor.…

- Brasher Company is transitioning to a lean manufacturing system and has just finalized two order fulfillment value streams. One of the value streams has two products, and the other has four products. The two-product value stream produces precision machine parts and the four-product value stream produces machine tools. Before moving to the value-stream structure, Brasher had a well-developed ABC system ( one that used all duration drivers) and had experienced good success with the more accurate product costs. Management wanted to be sure that the average costing approach of value-stream costing did not produce distorted product costs. Accordingly, expected weekly activity data were provided for the two-product value-streams to see how well average costing worked; however, management did not want to continue using ABC because if its intense data demands and the cost of updating as changes unfolded due to lean practices. In the table below, the driver for each activity is a…The Monroe Forging Company sells a corrugated steel product to the Standard Manufacturing Company and is in competition on such sales with other suppliers of the Standard Manufacturing Co. The vice president of sales of Monroe Forging Co. believes that by reducing the price of the product, a 40% increase in the volume of units sold to the Standard Manufacturing Co. could be secured. As the manager of the cost and analysis department, you have been asked to analyze the proposal of the vice president and submit your recommendations as to whether it is financially beneficial to the Monroe Forging Co. You are specifically requested to determine the following: (a) Net profit or loss based on the pricing proposal. (b) Unit sales volume under the proposed price that is required to make the same $40,000 profit that is now earned at the current price and unit sales volume. Use the following data in your analysis:Harris Systems has decided to adopt ABC. To remain competitive, Harris Systems’s management believes the company must produce the type of servers produced in Job B (from Decision Case 19-1) at a target cost of $5,400. Harris Systems has just joined a B2B e-market site that management believes will enable the firm to cut direct materials costs by 10%. Harris’s management also believes that a value engineering team can reduce assembly time. Compute the assembling cost savings required per Job B-type server to meet the $5,400 target cost. (Hint: Begin by calculating the direct materials, direct labor, and allocated overhead costs per server.)