D) Assume that the firm's minimum average variable cost is £6.5. Should the firm continue operating in the market in the short run? In the long run? Explain. E) If the firm is typical of other firms in the market, what price will it charge in the long run? Explain.

D) Assume that the firm's minimum average variable cost is £6.5. Should the firm continue operating in the market in the short run? In the long run? Explain. E) If the firm is typical of other firms in the market, what price will it charge in the long run? Explain.

Microeconomics A Contemporary Intro

10th Edition

ISBN:9781285635101

Author:MCEACHERN

Publisher:MCEACHERN

Chapter8: An Introduction To Perfect Competition

Section: Chapter Questions

Problem 16PAE

Related questions

Question

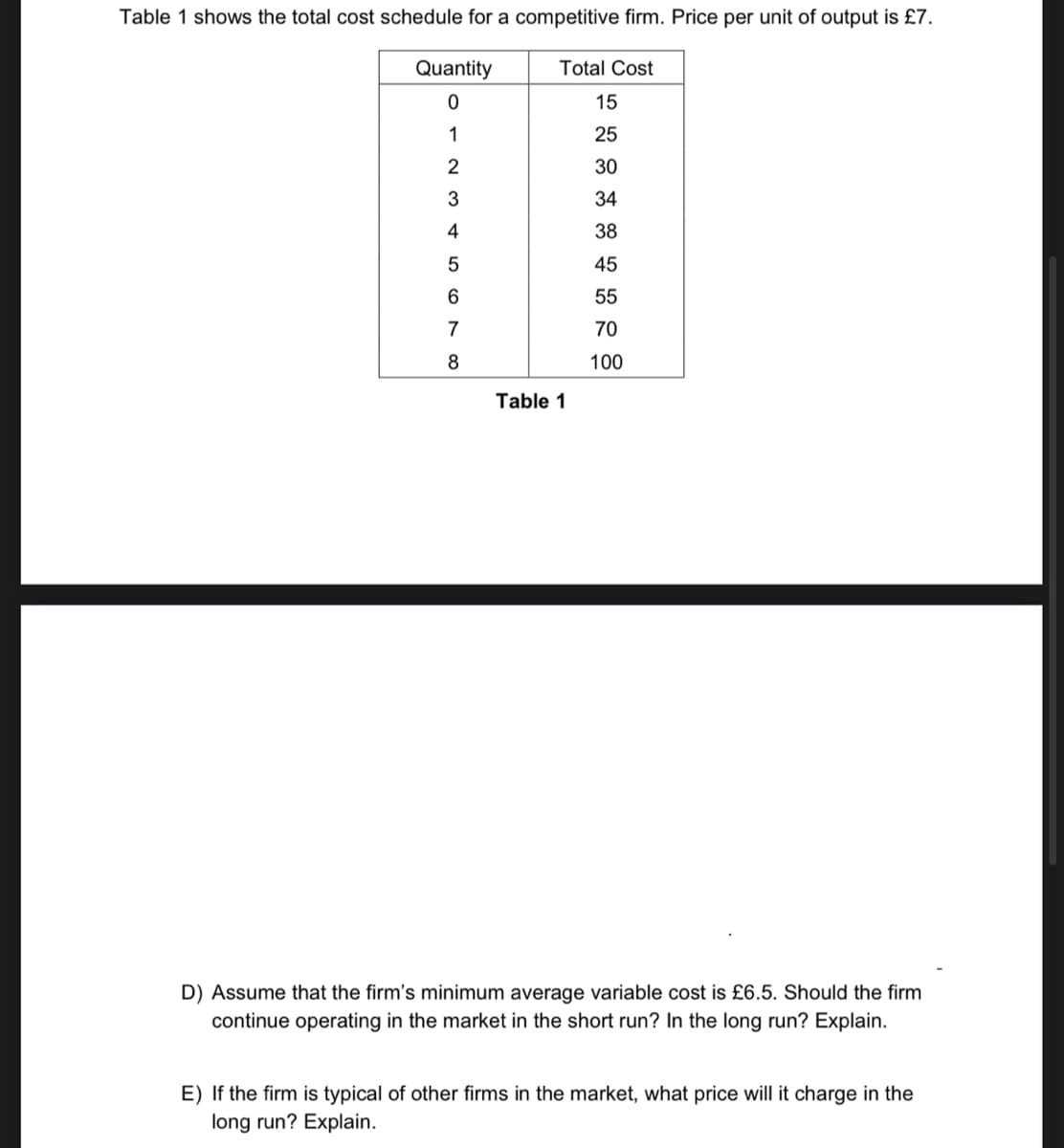

Transcribed Image Text:Table 1 shows the total cost schedule for a competitive firm. Price per unit of output is £7.

Quantity

0

1

2

3

4

5

6

7

8

Total Cost

15

25

30

34

38

45

55

70

100

Table 1

D) Assume that the firm's minimum average variable cost is £6.5. Should the firm

continue operating in the market in the short run? In the long run? Explain.

E) If the firm is typical of other firms in the market, what price will it charge in the

long run? Explain.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Microeconomics

Economics

ISBN:

9781305156050

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics (MindTap Course List)

Economics

ISBN:

9781305585126

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning