g and noncontrolling interests was $500,000 over the book value of the subsidiary’s Stockholders’ Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) [A] Asset Initial Fair Value Useful Life (years) Property, plant and equipment (PPE), net $100,000 10 Customer list 150,000 10 Goodwill 250,000 Indefinite $5

Please see below

Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary’s

[A] Asset Initial Fair Value Useful Life (years)

[A] Asset |

Initial Fair Value |

Useful Life (years) |

|---|---|---|

| Property, plant and equipment (PPE), net | $100,000 | 10 |

| Customer list | 150,000 | 10 |

| 250,000 | Indefinite | |

| $500,000 |

80% of the Goodwill is allocated to the parent. The parent and the subsidiary report the following financial statements at December 31, 2013:

| Parent | Subsidiary | Parent | Subsidiary | |||

|---|---|---|---|---|---|---|

| Income statement: | Balance sheet: | |||||

| Sales | $7,330,000 | $1,870,500 | Assets | |||

| Cost of goods sold | (5,131,000) | (1,122,300) | Cash | $411,313 | $131,511 | |

| Gross profit | 2,199,000 | 748,200 | 938,240 | 433,956 | ||

| Income (loss) from subsidiary | 189,496 | Inventory | 1,422,020 | 557,409 | ||

| Operating expenses | (1,392,700) | (486,330) | Equity investment | 1,475,671 | ||

| Net income | $995,796 | 261,870 | Property, plant and equipment (PPE), net | 5,374,356 | 1,280,669 | |

| $9,621,600 | $2,403,545 | |||||

| Statement of |

||||||

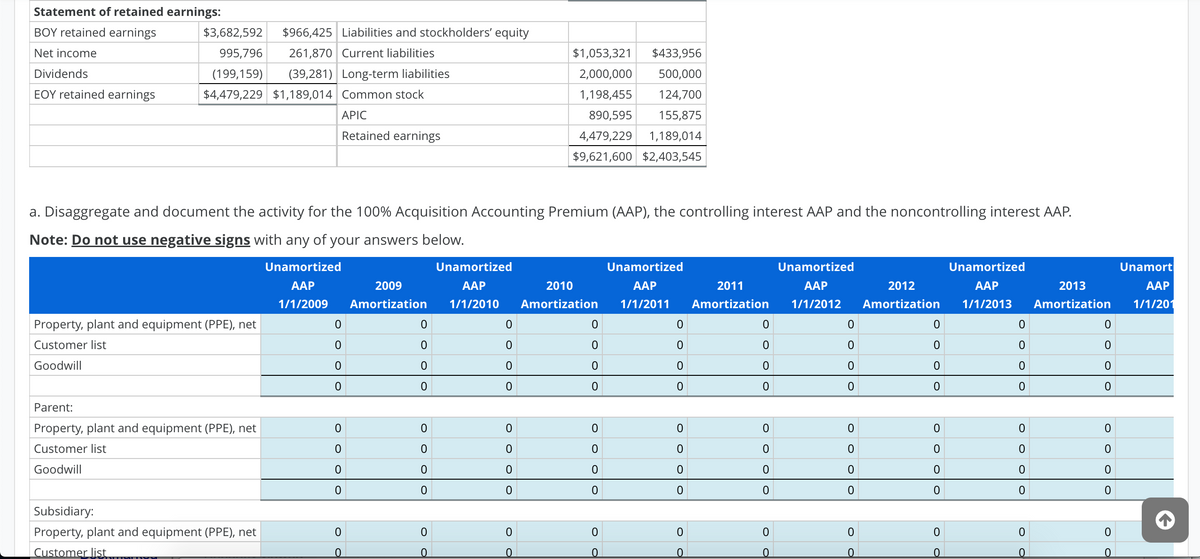

| BOY retained earnings | $3,682,592 | $966,425 | Liabilities and stockholders’ equity | |||

| Net income | 995,796 | 261,870 | Current liabilities | $1,053,321 | $433,956 | |

| Dividends | (199,159) | (39,281) | Long-term liabilities | 2,000,000 | 500,000 | |

| EOY retained earnings | $4,479,229 | $1,189,014 | Common stock | 1,198,455 | 124,700 | |

| APIC | 890,595 | 155,875 | ||||

| Retained earnings | 4,479,229 | 1,189,014 | ||||

| $9,621,600 | $2,403,545 |

a. Disaggregate and document the activity for the 100% Acquisition Accounting Premium (AAP), the controlling interest AAP and the noncontrolling interest AAP.

Note: Do not use negative signs with any of your answers below.

| Unamortized | Unamortized | Unamortized | Unamortized | Unamortized | Unamortized | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| AAP | 2009 | AAP | 2010 | AAP | 2011 | AAP | 2012 | AAP | 2013 | AAP | |

| 1/1/2009 | Amortization | 1/1/2010 | Amortization | 1/1/2011 | Amortization | 1/1/2012 | Amortization | 1/1/2013 | Amortization | 1/1/2014 | |

| Property, plant and equipment (PPE), net | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Customer list | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Goodwill | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

|

| Parent: | |||||||||||

| Property, plant and equipment (PPE), net | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Customer list | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Goodwill | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

|

| Subsidiary: | |||||||||||

| Property, plant and equipment (PPE), net | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Customer list | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Goodwill | Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

| Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

Answer

|

b. Calculate and organize the

| Downstream | Upstream | ||

|---|---|---|---|

| Jan. 1, 2013 | Answer | Answer

|

Answer

|

| Dec. 31, 2013 | Answer | Answer

|

Answer

|

c. Compute the pre-consolidation Equity Investment account beginning and ending balances starting with the stockholders’ equity of the subsidiary.

| Equity investment at 1/1/13: | |

| Common stock | Answer

|

| APIC | Answer

|

| Retained earnings | Answer

|

| Answer | Answer

|

| Answer

|

|

| Equity investment at 12/31/13: | |

| Common stock | Answer

|

| APIC | Answer

|

| Retained earnings | Answer

|

| Answer | Answer

|

| Answer

|

![Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP

Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000

over the book value of the subsidiary's Stockholders' Equity on the acquisition date. The parent assigned the excess to the following [A] assets:

[A] Asset Initial Fair Value Useful Life (years)

[A] Asset

Property, plant and equipment (PPE), net

Customer list

Goodwill

Income statement:

Sales

Cost of goods sold

Gross profit

Income (loss) from subsidiary

Operating expenses

Net income

Initial Useful

Fair Value Life (years)

$100,000

150,000

250,000

$500,000

80% of the Goodwill is allocated to the parent. The parent and the subsidiary report the following financial statements at December 31, 2013:

Parent Subsidiary

10

10

(1,392,700)

$995,796

Indefinite

Balance sheet:

$7,330,000 $1,870,500 Assets

(5,131,000) (1,122,300) Cash

2,199,000

189,496

748,200 Accounts receivable

Inventory

(486,330) Equity investment

261,870 Property, plant and equipment (PPE), net

Parent

Subsidiary

$411,313 $131,511

938,240 433,956

1,422,020

557,409

1,475,671

5,374,356 1,280,669

$9,621,600 $2,403,545](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F0d9d312f-4636-4de3-b73d-69def91fce63%2F24689928-d787-4fb3-9222-fc27c47b64de%2Foo6j90n_processed.png&w=3840&q=75)

Step by step

Solved in 4 steps