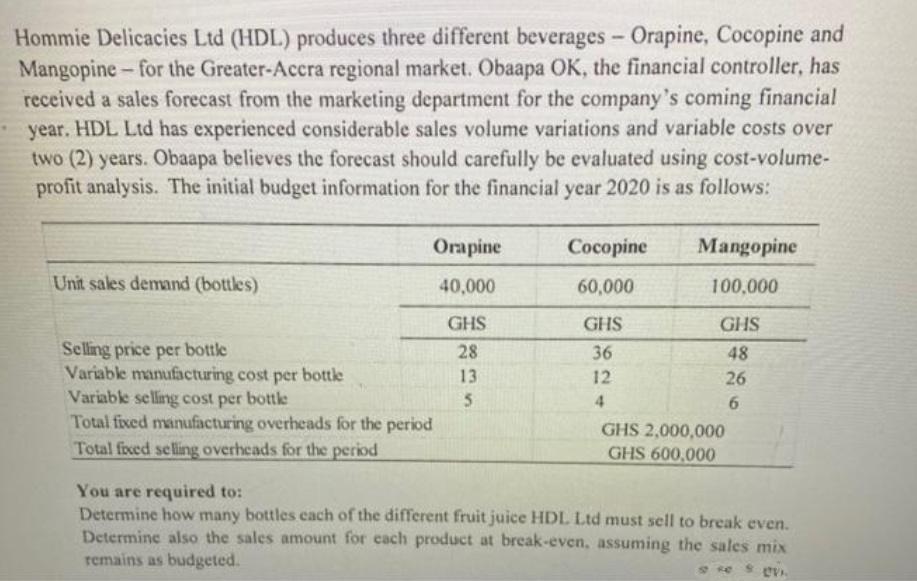

Hommie Delicacies Ltd (HDL) produces three different beverages - Orapine, Cocopine and Mangopine-for the Greater-Accra regional market. Obaapa OK, the financial controller, has received a sales forecast from the marketing department for the company's coming financial year. HDL Ltd has experienced considerable sales volume variations and variable costs over two (2) years. Obaapa believes the forecast should carefully be evaluated using cost-volume- profit analysis. The initial budget information for the financial year 2020 is as follows: Orapine Cocopine Mangopine Unit sales demand (bottles) 40,000 60,000 100,000 GHS GHS GHS Selling price per bottle 28 36 48 Variable manufacturing cost per bottle 13 12 26 Variable selling cost per bottle 5 4 6 Total fixed manufacturing overheads for the period GHS 2,000,000 GHS 600,000 Total fixed selling overheads for the period You are required to: Determine how many bottles each of the different fruit juice HDL Ltd must sell to break even. Determine also the sales amount for each product at break-even, assuming the sales mix remains as budgeted.

Hommie Delicacies Ltd (HDL) produces three different beverages - Orapine, Cocopine and Mangopine-for the Greater-Accra regional market. Obaapa OK, the financial controller, has received a sales forecast from the marketing department for the company's coming financial year. HDL Ltd has experienced considerable sales volume variations and variable costs over two (2) years. Obaapa believes the forecast should carefully be evaluated using cost-volume- profit analysis. The initial budget information for the financial year 2020 is as follows: Orapine Cocopine Mangopine Unit sales demand (bottles) 40,000 60,000 100,000 GHS GHS GHS Selling price per bottle 28 36 48 Variable manufacturing cost per bottle 13 12 26 Variable selling cost per bottle 5 4 6 Total fixed manufacturing overheads for the period GHS 2,000,000 GHS 600,000 Total fixed selling overheads for the period You are required to: Determine how many bottles each of the different fruit juice HDL Ltd must sell to break even. Determine also the sales amount for each product at break-even, assuming the sales mix remains as budgeted.

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter3: Cost Behavior

Section: Chapter Questions

Problem 34P: Kimball Company has developed the following cost formulas:...

Related questions

Question

V5

Transcribed Image Text:Hommie Delicacies Ltd (HDL) produces three different beverages - Orapine, Cocopine and

Mangopine-for the Greater-Accra regional market. Obaapa OK, the financial controller, has

received a sales forecast from the marketing department for the company's coming financial

year. HDL Ltd has experienced considerable sales volume variations and variable costs over

two (2) years. Obaapa believes the forecast should carefully be evaluated using cost-volume-

profit analysis. The initial budget information for the financial year 2020 is as follows:

Orapine

Cocopine

Mangopine

Unit sales demand (bottles)

40,000

60,000

100,000

GHS

GHS

GHS

Selling price per bottle

28

36

48

Variable manufacturing cost per bottle

13

12

26

Variable selling cost per bottle

5

4

6

Total fixed manufacturing overheads for the period

GHS 2,000,000

GHS 600,000

Total fixed selling overheads for the period

You are required to:

Determine how many bottles each of the different fruit juice HDL Ltd must sell to break even.

Determine also the sales amount for each product at break-even, assuming the sales mix

remains as budgeted.

se sv

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning