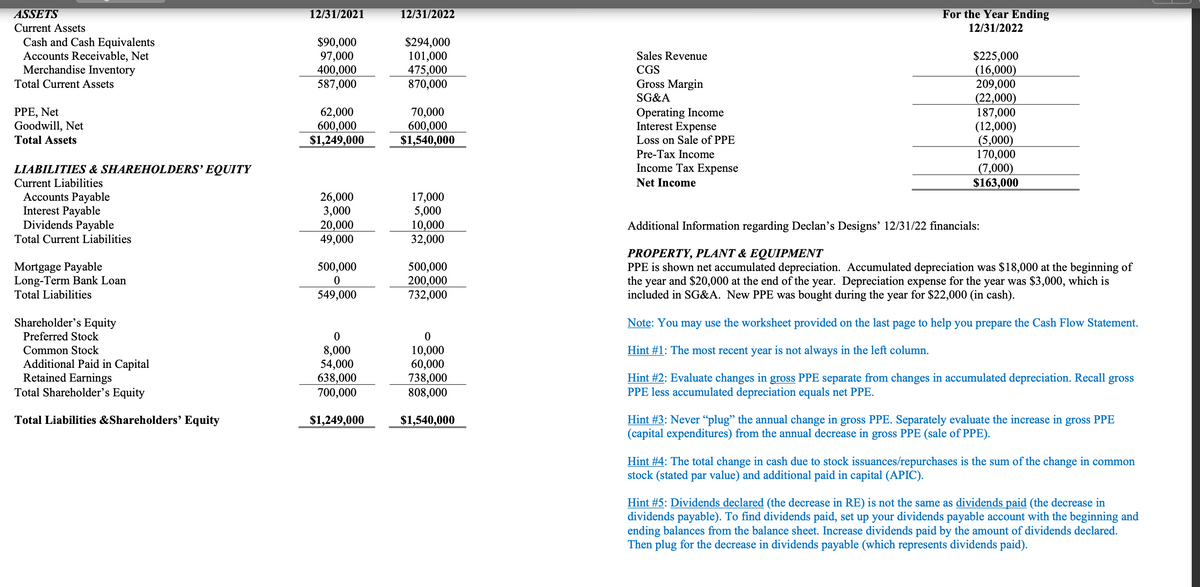

How does Accounts Receivable impact Declan's Designs 2022 Statement of Cash Flows? Question 19 options: The periodic change in Accounts Receivable is not included on the Statement of Cash Flows The periodic change in Accounts Receivable is subtracted in Cash Flows from Operations The periodic change in Accounts Receivable is is added in Cash Flows from Investing The periodic change in Accounts Receivable is subtracted in Cash Flows from Investing The periodic change in Accounts Receivable is added in Cash Flows from Operations The periodic change in Accounts Receivable is added in Cash Flows from Financing The periodic change in Accounts Receivable is subtracted in Cash Flows from Financing

How does

Question 19 options:

|

|

The periodic change in Accounts Receivable is not included on the Statement of Cash Flows |

|

|

The periodic change in Accounts Receivable is subtracted in Cash Flows from Operations |

|

|

The periodic change in Accounts Receivable is is added in Cash Flows from Investing |

|

|

The periodic change in Accounts Receivable is subtracted in Cash Flows from Investing |

|

|

The periodic change in Accounts Receivable is added in Cash Flows from Operations |

|

|

The periodic change in Accounts Receivable is added in Cash Flows from Financing |

|

|

The periodic change in Accounts Receivable is subtracted in Cash Flows from Financing |

Trending now

This is a popular solution!

Step by step

Solved in 3 steps