In a perfectly competitive market, the firms are observed to make positive economic profits in the short run. Due to the positive profits, new firms enter the market. Hence supply _(39), causing the equilibrium price level to _(40). This will corresponds to the minimum of the |(41) profits. The process will continue until the market equilibrium price _(42) function. 39. a) increases b) decreases 40. a) increase b) decrease 41. a) drive up b) drive down 42. a) long run average cost b) long run marginal cost

In a perfectly competitive market, the firms are observed to make positive economic profits in the short run. Due to the positive profits, new firms enter the market. Hence supply _(39), causing the equilibrium price level to _(40). This will corresponds to the minimum of the |(41) profits. The process will continue until the market equilibrium price _(42) function. 39. a) increases b) decreases 40. a) increase b) decrease 41. a) drive up b) drive down 42. a) long run average cost b) long run marginal cost

Microeconomics: Private and Public Choice (MindTap Course List)

16th Edition

ISBN:9781305506893

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Chapter9: Price Takers And The Competitive Process

Section: Chapter Questions

Problem 5CQ

Related questions

Question

For Questions 39 to 42, consider the following paragraph on long run dynamics of a

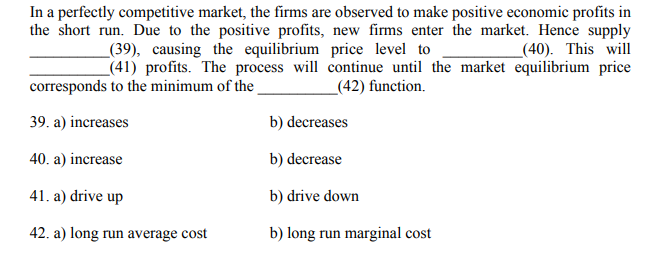

Transcribed Image Text:In a perfectly competitive market, the firms are observed to make positive economic profits in

the short run. Due to the positive profits, new firms enter the market. Hence supply

_(39), causing the equilibrium price level to

(40). This will

(41) profits. The process will continue until the market equilibrium price

_(42) function.

corresponds to the minimum of the

39. a) increases

b) decreases

40. a) increase

b) decrease

41. a) drive up

b) drive down

42. a) long run average cost

b) long run marginal cost

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning