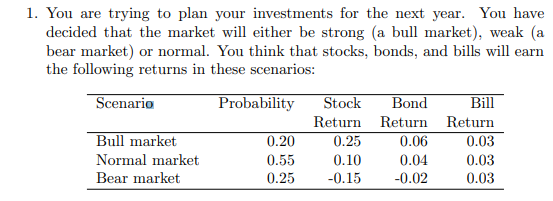

You have also decided that you have a risk-aversion (A) of 4. (a) What is the expected return for each of the securities? (b) What is the volatility of each security return? (c) What is the covariance between stock and bond returns?

You have also decided that you have a risk-aversion (A) of 4.

(a) What is the expected return for each of the securities?

(b) What is the volatility of each security return?

(c) What is the covariance between stock and bond returns?

(d) If you combine stocks and bills as an investment, what is your optimal combination? What is your expected return? What is your

portfolio’s volatility?

(e) If you combine bonds and bills, what is your optimal combination?

What is your expected return? What is your portfolio’s volatility?

(f) If you combine stocks and bonds, what is your optimal combination?

What is your expected return? What is your portfolio’s volatility?

(g) If you combine all three assets in your portfolio, what is your optimal combination? What is your expected return? What is your

portfolio’s volatility?

Step by step

Solved in 4 steps with 12 images

Is the equation for volatility not Σ P ( x - x̄ )^2 ?

And I am finding online that covariance is cov(x,y) = ∑(xi - x̄)(yi - ȳ) / N - 1 , I see the equation you have given does not divide by the samples, why is this?

For part B, is it meant to be the expected return on the stock in all market conditions or should I be using the expected return depending on the market?

e.g. instead of using 0.07 for each of the stocks, using 0.05, 0.06 and (0.04)