Jade Bhd. has a policy of writing off development expenditure to profit or loss as it was incurred. In preparing its financial statements for the year ended 30 September 2020 it has become aware that, under IFRS rules, qualifying development expenditure should be treated as an intangible asset. Below is the qualifying development expenditure for Jade: RM’ 000 Year ended 30 September 2017 300

Jade Bhd. has a policy of writing off development expenditure to profit or loss as it was incurred. In preparing its financial statements for the year ended 30 September 2020 it has become aware that, under IFRS rules, qualifying development expenditure should be treated as an intangible asset. Below is the qualifying development expenditure for Jade: RM’ 000 Year ended 30 September 2017 300

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter12: Intangibles

Section: Chapter Questions

Problem 4C

Related questions

Question

Please answer competely

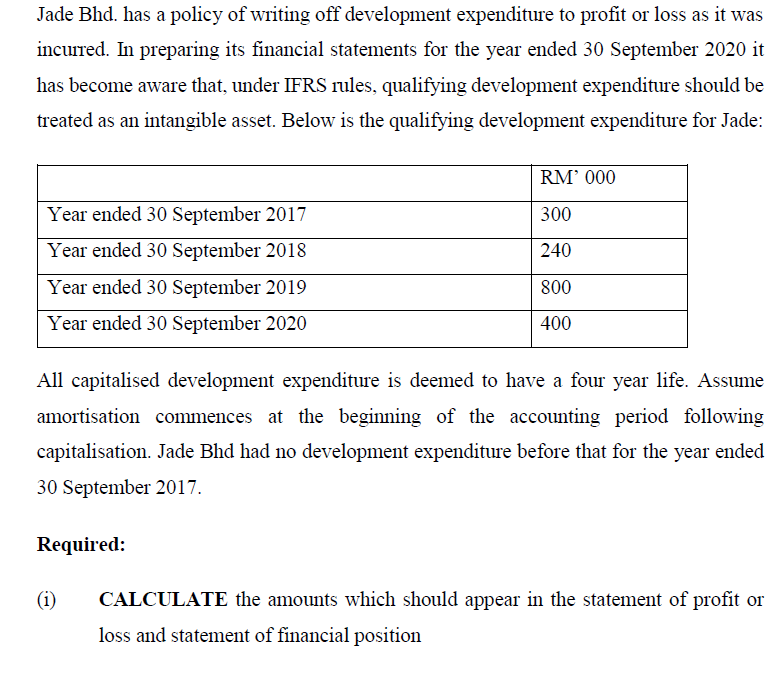

Transcribed Image Text:Jade Bhd. has a policy of writing off development expenditure to profit or loss as it was

incurred. In preparing its financial statements for the year ended 30 September 2020 it

has become aware that, under IFRS rules, qualifying development expenditure should be

treated as an intangible asset. Below is the qualifying development expenditure for Jade:

RM' 000

Year ended 30 September 2017

300

Year ended 30 September 2018

240

Year ended 30 September 2019

800

Year ended 30 September 2020

400

All capitalised development expenditure is deemed to have a four year life. Assume

amortisation commences at the beginning of the accounting period following

capitalisation. Jade Bhd had no development expenditure before that for the year ended

30 September 2017.

Required:

(i)

CALCULATE the amounts which should appear in the statement of profit or

loss and statement of financial position

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning