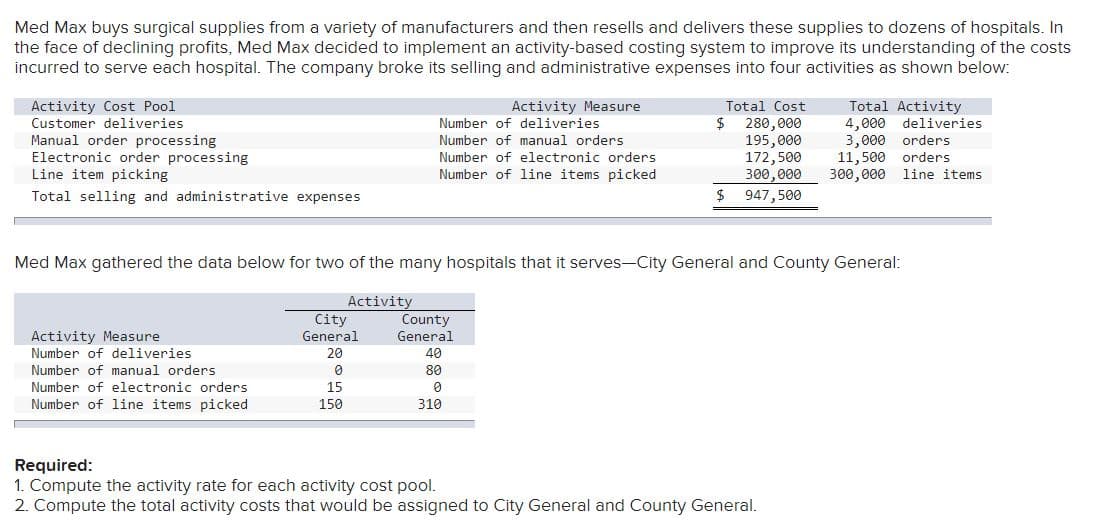

Med Max buys surgical supplies from a variety of manufacturers and then resells and delivers these supplies to dozens of hospitals. In the face of declining profits, Med Max decided to implement an activity-based costing system to improve its understanding of the costs incurred to serve each hospital. The company broke its selling and administrative expenses into four activities as shown below: Activity Cost Pool Customer deliveries Activity Measure Total Cost Total Activity 4,000 deliveries 3,000 orders 11,500 orders 300,000 line items Number of deliveries 2$ Manual order processing Electronic order processing Line item picking 280,000 195,000 172,500 300,000 $ 947,500 Number of manual orders Number of electronic orders Number of line items picked Total selling and administrative expenses Med Max gathered the data below for two of the many hospitals that it serves-City General and County General: Activity City County Activity Measure Number of deliveries Number of manual orders General General 20 40 80 Number of electronic orders 15 Number of line items picked 150 310 Required: 1. Compute the activity rate for each activity cost pool. 2. Compute the total activity costs that would be assigned to City General and County General.

Med Max buys surgical supplies from a variety of manufacturers and then resells and delivers these supplies to dozens of hospitals. In the face of declining profits, Med Max decided to implement an activity-based costing system to improve its understanding of the costs incurred to serve each hospital. The company broke its selling and administrative expenses into four activities as shown below: Activity Cost Pool Customer deliveries Activity Measure Total Cost Total Activity 4,000 deliveries 3,000 orders 11,500 orders 300,000 line items Number of deliveries 2$ Manual order processing Electronic order processing Line item picking 280,000 195,000 172,500 300,000 $ 947,500 Number of manual orders Number of electronic orders Number of line items picked Total selling and administrative expenses Med Max gathered the data below for two of the many hospitals that it serves-City General and County General: Activity City County Activity Measure Number of deliveries Number of manual orders General General 20 40 80 Number of electronic orders 15 Number of line items picked 150 310 Required: 1. Compute the activity rate for each activity cost pool. 2. Compute the total activity costs that would be assigned to City General and County General.

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter4: Activity-based Costing

Section: Chapter Questions

Problem 4BE: Activity-based costing: selling and administrative expenses Jungle Junior Company manufactures and...

Related questions

Question

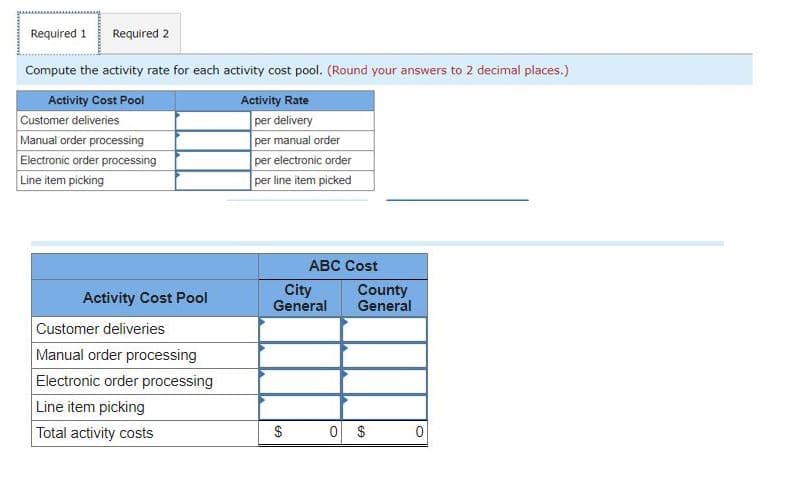

Transcribed Image Text:Required 1

Required 2

Compute the activity rate for each activity cost pool. (Round your answers to 2 decimal places.)

Activity Cost Pool

Activity Rate

Customer delivenies

Manual order processing

Electronic order processing

Line item picking

per delivery

per manual order

per electronic order

per line item picked

ABC Cost

Activity Cost Pool

City

General

County

General

Customer deliveries

Manual order processing

Electronic order processing

Line item picking

Total activity costs

$

0 $

%24

Transcribed Image Text:Med Max buys surgical supplies from a variety of manufacturers and then resells and delivers these supplies to dozens of hospitals. In

the face of declining profits, Med Max decided to implement an activity-based costing system to improve its understanding of the costs

incurred to serve each hospital. The company broke its selling and administrative expenses into four activities as shown below:

Activity Measure

Total Cost

Activity Cost Pool

Customer deliveries

Manual order processing

Electronic order processing

Line item picking

Total Activity

4,000

3,000 orders

11,500 orders

300,000 line items

Number of deliveries

280,000

195,000

172, 500

300,000

deliveries

Number of manual orders

Number of electronic orders

Number of line items picked

Total selling and administrative expenses

$

947,500

Med Max gathered the data below for two of the many hospitals that it serves-City General and County General:

Activity

City

County

Activity Measure

General

General

Number of deliveries

20

40

Number of manual orders

80

Number of electronic orders

15

Number of line items picked

150

310

Required:

1. Compute the activity rate for each activity cost pool.

2. Compute the total activity costs that would be assigned to City General and County General.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning