Question 1 Consider two identical firms (firm 1 and firm 2) that face a linear market demand curve. Each firm has a marginal cost of zero and the two firms together face demand: P = 150 - 0.25Q, where Q = Q₁ + Q2. Find the Cournot equilibrium quantity and market price for each firm.

Question 1 Consider two identical firms (firm 1 and firm 2) that face a linear market demand curve. Each firm has a marginal cost of zero and the two firms together face demand: P = 150 - 0.25Q, where Q = Q₁ + Q2. Find the Cournot equilibrium quantity and market price for each firm.

Chapter15: Imperfect Competition

Section: Chapter Questions

Problem 15.3P

Related questions

Question

100%

Textbook Exercises ... please help

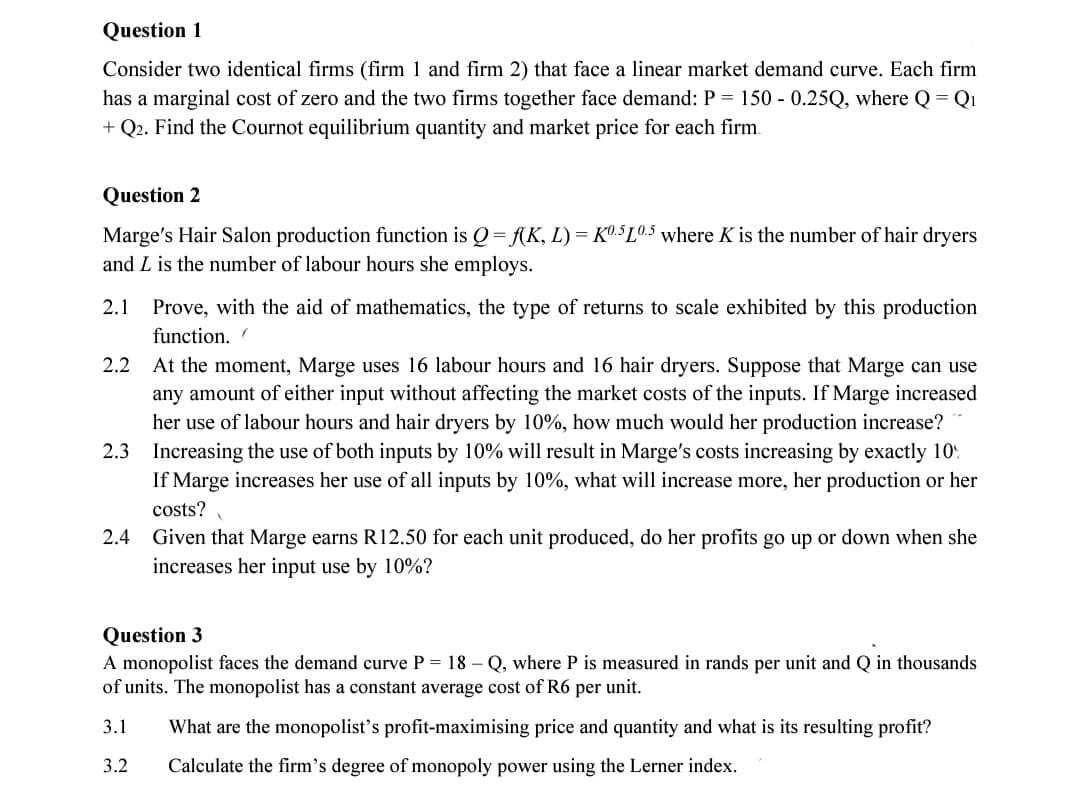

Transcribed Image Text:Question 1

Consider two identical firms (firm 1 and firm 2) that face a linear market demand curve. Each firm

has a marginal cost of zero and the two firms together face demand: P = 150 - 0.25Q, where Q = Q₁

+ Q2. Find the Cournot equilibrium quantity and market price for each firm.

Question 2

Marge's Hair Salon production function is Q = f(K, L) = K0.5 10.5 where K is the number of hair dryers

and L is the number of labour hours she employs.

2.1 Prove, with the aid of mathematics, the type of returns to scale exhibited by this production

function. (

2.2 At the moment, Marge uses 16 labour hours and 16 hair dryers. Suppose that Marge can use

any amount of either input without affecting the market costs of the inputs. If Marge increased

her use of labour hours and hair dryers by 10%, how much would her production increase?

2.3 Increasing the use of both inputs by 10% will result in Marge's costs increasing by exactly 10%

If Marge increases her use of all inputs by 10%, what will increase more, her production or her

costs?

2.4

Given that Marge earns R12.50 for each unit produced, do her profits go up or down when she

increases her input use by 10%?

Question 3

A monopolist faces the demand curve P = 18-Q, where P is measured in rands per unit and Q in thousands

of units. The monopolist has a constant average cost of R6 per unit.

3.1

What are the monopolist's profit-maximising price and quantity and what is its resulting profit?

3.2 Calculate the firm's degree of monopoly power using the Lerner index.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Survey of Economics (MindTap Course List)

Economics

ISBN:

9781305260948

Author:

Irvin B. Tucker

Publisher:

Cengage Learning

Survey of Economics (MindTap Course List)

Economics

ISBN:

9781305260948

Author:

Irvin B. Tucker

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning