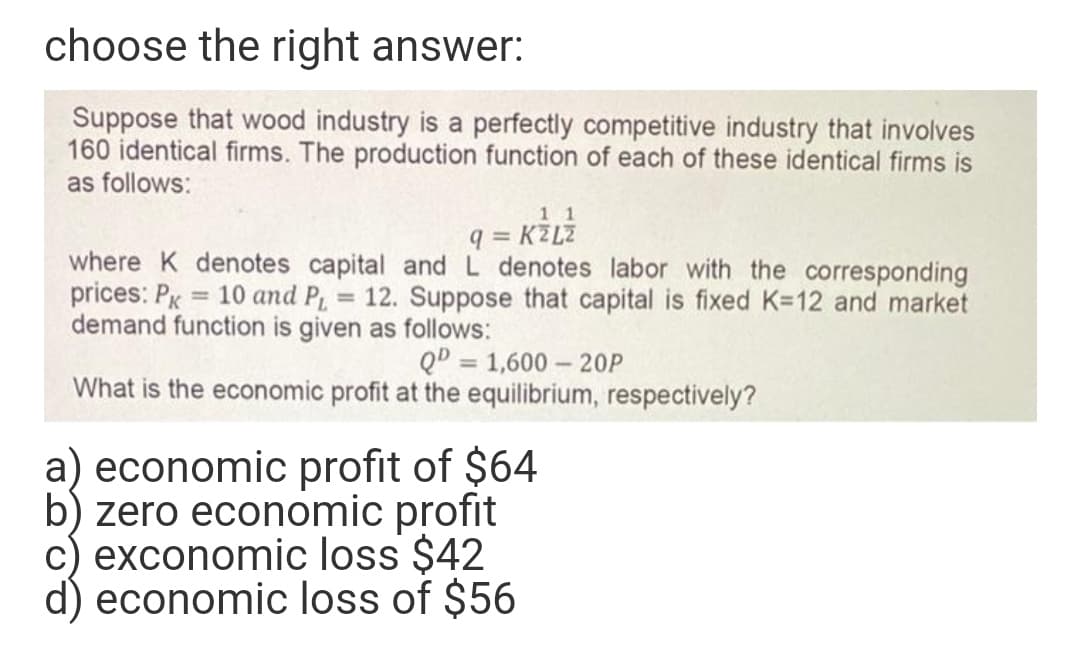

Suppose that wood industry is a perfectly competitive industry that involves 160 identical firms. The production function of each of these identical firms is as follows: 1 1 q = KZLZ where K denotes capital and L denotes labor with the corresponding prices: PK = 10 and P, 12. Suppose that capital is fixed K=12 and market %3D %3D demand function is given as follows: QD = 1,600 - 20P %3D What is the economic profit at the equilibrium, respectively?

Q: A firm in a perfectly competitive market has a short-run total cost function equal to SRTC=4+20q,…

A: In perfect competition there are large number of firms selling identical goods.

Q: Assume that the above cost data is for a perfectly competitive firm. Using this data answer the…

A: Answer to the question is as follows :

Q: There are 300 identical firms in a perfectly competitive market, the price of the output is p, the…

A: Given: C = q3 - 2q2 + 2q + 10 Number of firms = 300

Q: In a perfectly competitive industry, each firm has the following long run (total) cost function: C =…

A: Output is the amount, either utilized or employed for more manufacturing, of products or services…

Q: The competitive fringe supply function (total): QF=2P-12 The dominant firms marginal cost function:…

A: (Q) A market consists of a dominant firm and a number of fringe firms. The followings are the…

Q: Suppose that wood industry is a perfectly competitive industry that involves 160 identical firms.…

A: Correct Answer: Option (a) P = 16, q = 8

Q: C = 250,000 + 40Q + 0.01Q2, and market demand function: P = 940 – 0.02Q (a) Determine…

A: Total cost function represents the total cost as the sum of the fixed costs and the variable costs…

Q: Assume the demand function for a product is given by QD = 20,000 – 10P + 0.4I, where P = price of…

A: Given: QD = 20,000 – 10P + 0.4I QS = 30P I= $10,000 Therefore, QD=20,000–10P+0.4IAs…

Q: Now lets discuss the short run on the same market. Assume there are 30 identical firms in a…

A: At equilibrium ; MR = MC

Q: Per-unit cost (P) P = 12 10 8 80 90 100 Marginal Cost long run, Average Cost Average Variable Cost…

A: Here the supply curve is the curve depicting how much production of manufacturing goods is being…

Q: Suppose you are hired as an economic consultant for Promax Consulting Company. Your job is to…

A: The perfectly competitive firm, maximize its benefit when its minimal expense is equivalent to the…

Q: If the demand function faced by a firm is: Q = 90 – 2P TC = 2 + 57Q – 8Q2 + Q3 Determine the best…

A: Dear student, There are multiple questions asked in a single post. I am answer question 1. You can…

Q: FInd the profit maximizing levels of K and L as functions of r,w, and p. b) Suppose that r = w= $1…

A: Profit maximization is the process that helps to regulate the prices, input, and output level of the…

Q: Find an individual firm’s supply curve. How many firms are there currently in the market?

A:

Q: Suppose that the firm operates in a perfectly competitive market. The market price of his product is…

A: The perfectly competitive market is a market type which is characterized by a large number of buyers…

Q: Consider a competitive firm with a short-run cost function C(q) = 100q−q2 + 1/5q3 +450. (a)…

A: Answer to the three sub parts are as follows :

Q: The wood-pallet market contains many identical firms, each with the short-run total cost function…

A: The perfectly competitive market structure is characterized by the large number of firms and buyers.…

Q: A market consists of a dominant firm and a number of fringe firms. The followings are the…

A: Since you have posted a question with multiple sub-parts, we will solve the first three subparts for…

Q: Suppose Firm X is a dominant firm in a market where the market demand is Q = 1200 -2p. Once Firm X…

A: A residual demand function means the demand faced by an individual firm (Firm X in given case) that…

Q: A competitive firm’s production function is given by y= f(x1,x2)= 4x11/2 + 10x21/2 a) The price of…

A: Answer: Given, Production function: y=fx1,x2=4x112+10x212 Price of factor 1(w1)= 1 Price of factor 2…

Q: 29. Consider a perfectly competitive industry in which each firm has the total cost function tc = q…

A: In a perfectly competitive market there are large number of firms producing identical products thus…

Q: firm’s production function is Q = 10 + 30L - .5L2+ 30K – K2, and its competitive demand function is…

A: Answer A firm’s production function is Q = 10 + 30L - 0.5L2 + 30K – K2 MPL = = 40 - L At…

Q: Solve the attachment.

A: Hessian matrix is a square matrix of partial second derivatives of the cost function with respect to…

Q: Consider a competitive firm with a short-run cost function C(q)=100q-q^2+(1/5)q^3+450 (a) Suppose…

A: We will use short run profit maximisation condition for perfectly competitive market to solve this…

Q: A firm is a perfectly competitive producer and sells two goods G1 and G2 at $1600 and $1200,…

A: Given, P1 = $1600 P2 = $1200 MC1 = 2Q1 + Q2 MC2 = 4Q2 + Q1

Q: uppose that each firm in a competitive industry has the following identical costs: Total cost: TC =…

A: 1) Let's start by calculating the fixed, variable and marginal costs. The total cost function of…

Q: Suppose the market for cat food is perfectly competitive, with each firm having the total cost…

A: At the point when market price = MC, a profit-maximizing fully competitive company produces. In…

Q: Suppose you are given the following information about a particular industry: Market…

A: Given information-

Q: A perfectly competitive industry has a large number of potential entrants. Each firm has an…

A: The short run supply function for each firm is p= MC = q -10 => q = p+10

Q: The market for good X consists of 1,000 identical firms, each with the total and marginal cost…

A: In short run, Price = MC. Firm's supply function is its MC function. In long run, new firms enter…

Q: Each firm in a competitive market has a cost function of: C = 49 + g?. so its marginal cost function…

A: Answers In the long run AC = MC = P. Hence we have P = 49/q + q = 2q which gives q = 7 units and…

Q: The demand for bicycles is given by the equation: Q = 1000 – 5P There are currently 100 identical…

A: Given information Market Demand function Q=1000-5P Firms Cost function C=25/2*q2+20q+50 There are…

Q: Consider an individual firm operating in a perfectly competitive market. Suppose there is an…

A: A perfectly competitive firm is characterized by three factors: infinite number of buyers and…

Q: Determining Rent in a Market with Low-Cost and High-Cost Firms Suppose firms in a competitive market…

A: The competitive market is the one where there are infinite buyers and sellers who produces…

Q: PakMonoG’s inverse demand function is P = 100 – 2Q and cost function is TC = 10 + 2Q, where Q is…

A: Given; Demand function; P=100-2Q Cost function; TC=10+2Q where; Q= quantity in units P= price in PKR

Q: Suppose the doll company American Girl has an inverse demand curve of P = 150 – 0.25Q, where Q…

A: Total cost (TC): - it is the sum of fixed and variable costs incurred in the production process.…

Q: The following relations describe monthly demand and supply for a wheat Qp = 32 - 4 Qs = ÷P- 16 where…

A: (a) A perfectly competitive market produces at the intersection point of market demand and market…

Q: Given the cost function underlying the figure, would two firms producing output Q (>0) always incur…

A: The total cost incurred by a firm operating in a market can be fixed cost or variable cost. Fixed…

Q: There are 300 identical firms in a perfectly competitive market, the price of the output is p, the…

A: C = q3 - 2q2 + 2q + 10 Number of firms = 300

Q: Suppose that the total market demand for crude oil is given by 70, 000 – 2,000P - where Q, is the…

A: Given; Demand for crude oil; QD=70000-2000P Number of identical small producers= 1000 Marginal Cost;…

Q: Each firm in a perfectly competitive industry has the following production function: q = K1/4L1/4…

A: To calculate the total number of firms in the industry, first we must be aware of the fact that in…

Q: Suppose that wood industry is a perfectly competitive industry that involves 160 identical firms.…

A: Correct option : b) P= 16, q= 8 In perfect competition, short run firm's supply is given by marginal…

Q: The market for drones is perfectly competitive. Assume for simplicity that fractions of everything,…

A: In perfect competition, when the price increases then the firm is willing to produce more. This…

Q: Assume that the market determined price is $10 in a perfectly competitive industry. A firm is…

A: Profit maximization refers to a process that firms go through to guarantee that they have the…

Q: Suppose that many small firms operating in the perfectly competitive market set-up. All firms are…

A: c (q)= 40+8q+(q^2/10) P= A - (Q/50) 78 firms in the market, firm’s maximum profit is $22.5

Q: Under what condition will a competitive firm necessarily shut down its operations? What does this…

A: According to the law of supply the higher is price higher is the quantity supplied and lower the…

Q: 1. There are 300 identical firms in a perfectly competitive market, the price of the output is the…

A: The producer is in surplus when he gets abnormal profit, that is MR>MC. The benefit the producer…

Q: The demand for bicycles is given by the equation: Q = 1000 – 5P - There are currently 100 identical…

A: Given information Market Demand function Q=1000-5P Firms Cost functionC=252q2+20q+50 There are 100…

Q: Consider a competitive market in which the market demand for the product is expressed as P = 75 ‑…

A: Perfect competition is one of the types of market structure where there are many sellers and many…

Q: There are 300 identical firms in a perfectly competitive market, the price of the output iS p, the…

A: Given Total cost function in short run: C(q)=q3-2q2+2q+10 .........(1)

Step by step

Solved in 2 steps

- Suppose a firm’s total cost is C = rK + (q 2 /2K), where K = the firm’s capital (plant size), q is output and r is the price of a unit of capital. 1. What is short-run average total cost (C/q) and what is marginal cost dC/dq, assuming K is fixed at K0 (2 points) 2. Suppose K is not fixed, but output is fixed at q0. Given this exogenous output and exogenous price of capital r0, what level of capital (K*) is most efficient – that is, minimizes total cost C? Do not forget to check the second order condition (4 points) 3. Find and interpret ∂K*/∂r.A purely competitive firm has a single variable input L (labor), with the wage rate W0 per period. Its fixed inputs cost the firm a total of F dollars per period. The price of the product is P0. (a) write the production function, revenue function, cost function, and profit function of the firm. (b) What is the first-order condition for profit maximization? Give this condition an economic interpretation. (c) What economic circumstances would ensure that profit is maximized rather thatn minimized?Modified True or False: State whether each statement is true or false. If the statement is false, briefly explain why it is so, and then restate it to make it true. The shapes of long-run cost curves follow directly from the assumption of a fixed factor of production, which implies diminishing returns. The optimal scale of plant is the scale of plant that maximizes average cost. In the long-run competitive equilibrium, each individual firm chooses a scale of operations that minimizes its long-run average cost. Answer correctly and explain within 30mins will give you positive feedback.

- The graph below shows a particular firms marginal revenue (mr) marginal cost (mc) and average total cost (atc) curves, where the market is competitive. Suppose that a new management team is brought in and that this team is initially less concerned about maximizing profits than it is simply about making a profit. What range of production quantities will allow the firm to operate while earning a profit? Give you're answer by dragging the qmin to Qmax lines into their correct positions. The output will need to lie somewhere between those limits.In the graph below, you can see the iso-cost curve and the iso-quant curve for the firm to produce q = 1000 units of output. Note that the vertical axis shows the quantity of capital while the horizontal axis shows the quantity of labor. Suppose that the firm is producing 1000 units of output at point A, using 200 units of capital and 100 units of labor. (i) As an outside consultant, what actions would you suggest to management to improve profits? (ii) What would you recommend if the firm were operating at point B, using 100 units of capital and 200 units of labor? Explain your answer.A purely competitive firm has a single variable input < (labor), with the wage rate. W0 per period. Its fixed inputs cost the firm a total of F dollars per period. The price of the product is P0. (a) write the production function, revenue function, cost function, and profit function of the firm. (b) what is the first-order condition for profit maximization ? Give this condition an economic interpretation. (c) What economic circumstances would ensure taht profit is maximized rather tahtn minimized?

- Answer the given question with a proper explanation and step-by-step solution. Ned’s Tuna has the following production function: q = K3/4L1/4, Where q is the number of tunas per hour, L is the number of workers and K is the number of boats. Suppose that w = $20/hour (PL) and r = $30/hour (PK). a. Find Ned’s marginal product of labor (MPL). Does it exhibit diminishing marginal returns? b. Find Ned’s marginal product of capital (MPK). Does it exhibit diminishing marginal returns? c. Find and draw an isocost function for CSuppose the production function is given by Q=K1/2L1/2, and that Q=30 and K = 36. How much labor isemployed by the firm?A. 49 B.6 C.36 D.25Use second image for reference, for part b here is referene; The maximum profit is found at the tangency between the production function and the isoprofit line. In other words, the slope of the production function and the slope of the isoprofit line must be the same. This is written as MPL = w where w is the slope of the isoprofit line. Then we get sqrt1 / 2L = w => 1/2w = sqrtL => L*D = 1/4w^2

- QUESTION 1a. Is it possible to have diminishing returns to a single factor of production and constant returnsto scale at the same time? Discuss.b. Isoquants can be convex, linear, or L-shaped. What does each of these shapes tell you aboutthe nature of the production function? What does each of these shapes tell you about theMRTS?QUESTION 2a. A firm faces the following average revenue (demand) curve:P = 120 − 0.02Qwhere Q is weekly production and P is price, measured in cents per unit. The firm’s costfunction is given by C = 60Q + 25,000. Assume that the firm maximizes profits.i. What is the level of production, price, and total profit per week?ii. If the government decides to levy a tax of 14 cents per unit on this product, what will be thenew level of production, price, and profit?b. The United States currently imports all of its coffee. The annual demand for coffee by U.S.consumers is given by the demand curve Q = 250 – 10P, where Q is quantity (in millions ofpounds) and P is the…(a) Show that the production function Q = (Kα + Lα)β, where Q is output, K is capital input, L islabour input and α > 0 and β > 0 exhibits diminishing returns when α < 1 and increasing returns to scale when αβ > 1.(b) Specify a translog cost function for two inputs and show that the input shares depend on inputprices.2.1 Consider N firms each with the constant-returns-to-scale production function Y = F (K, AL), or (using the intensive form) Y = ALf (k). Assume f'(•) > 0, f"(•) < 0. Assume that all firms can hire labor at wage wA and rent capital at cost r, and that all firms have the same value of A.(a) Consider the problem of a firm trying to produce Y units of output at minimum cost. Show that the cost-minimizing level of k is uniquely defined and is independent of Y, and that all firms therefore choose the same value of k.(b) Show that the total output of the N cost-minimizing firms equals the output that a single firm with the same production function has if it uses all the labor and capital used by the N firms. 2.2 The elasticity of substitution with constant-relative-risk-aversion utility. Consider an individual who lives for two periods and whose utility is given by equation (2.43). Let P1 and P2 denote the prices of consumption in the two periods, and let W denote the value of the…