Tanufacturing is a cost center and the two sales departments are profit centers. full cost of each roll of carpeting produced (including fully absorbed overhead) is transferred to the sales department ordering the carpet. The evaluation of the sales departments includes the fully absorbed cost of each roll as the transfer price. The current manufacturing plant is operating at capacity. A new plant is being built that will more than double capacity. Within two years, management believes that its businesses will grow such that most of the excess capacity will be eliminated. When the new plant comes online, the plan is for one plant to produce exclusively commercial carpeting and the other to produce exclusively residential carpeting. This change will simplify scheduling, ordering, and inventory control in each plant. It will also create some economies of scale by producing longer mill runs. Nevertheless, it will take a couple of years before these economies of scale can be realized. Each mill produces carpeting in four-meter-wide rolls of up to 100 meters in length. The output of each mill is measured in terms of meters of four-meter rolls produced. Overhead is assigned to carpet rolls using carpet meters produced in the mill. The cost structure of each plant is as follows: Old Plant New Plant Normal machine hours per year 6,000 5,000 Normal carpet meters per hour 1,000 1,400 Normal capacity 6,000,000 meters 7,000,000 meters Annual manufacturing overhead costs excluding accounting depreciation €15,000,000 €21,000,000 Accounting depreciation per year € 6,000,000 €21,000,000 Karsten's new mill will run at higher speed and therefore produce more meters of carpet per hour. Moreover, the new mill will use 15 percent less direct materials and direct labor because the new machines, being more automated, produce less scrap and 497

Tanufacturing is a cost center and the two sales departments are profit centers. full cost of each roll of carpeting produced (including fully absorbed overhead) is transferred to the sales department ordering the carpet. The evaluation of the sales departments includes the fully absorbed cost of each roll as the transfer price. The current manufacturing plant is operating at capacity. A new plant is being built that will more than double capacity. Within two years, management believes that its businesses will grow such that most of the excess capacity will be eliminated. When the new plant comes online, the plan is for one plant to produce exclusively commercial carpeting and the other to produce exclusively residential carpeting. This change will simplify scheduling, ordering, and inventory control in each plant. It will also create some economies of scale by producing longer mill runs. Nevertheless, it will take a couple of years before these economies of scale can be realized. Each mill produces carpeting in four-meter-wide rolls of up to 100 meters in length. The output of each mill is measured in terms of meters of four-meter rolls produced. Overhead is assigned to carpet rolls using carpet meters produced in the mill. The cost structure of each plant is as follows: Old Plant New Plant Normal machine hours per year 6,000 5,000 Normal carpet meters per hour 1,000 1,400 Normal capacity 6,000,000 meters 7,000,000 meters Annual manufacturing overhead costs excluding accounting depreciation €15,000,000 €21,000,000 Accounting depreciation per year € 6,000,000 €21,000,000 Karsten's new mill will run at higher speed and therefore produce more meters of carpet per hour. Moreover, the new mill will use 15 percent less direct materials and direct labor because the new machines, being more automated, produce less scrap and 497

Accounting (Text Only)

26th Edition

ISBN:9781285743615

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Carl Warren, James M. Reeve, Jonathan Duchac

Chapter21: Cost Behavior And Cost-volume-profit Analysis

Section: Chapter Questions

Problem 21.4CP: Variable costs and activity bases in decision making The owner of Warwick Printing, a printing...

Related questions

Question

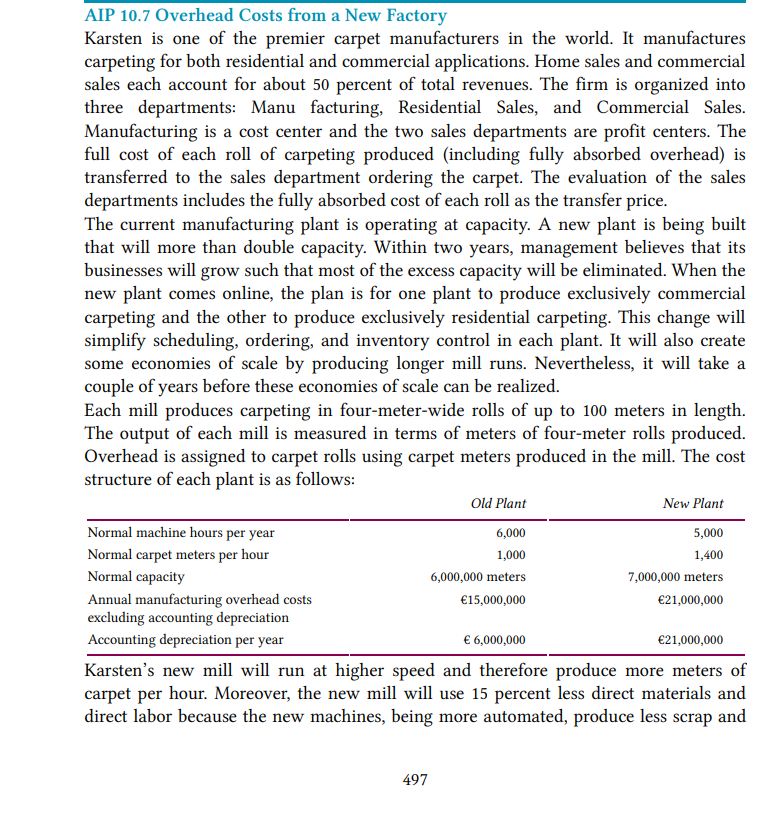

Transcribed Image Text:AIP 10.7 Overhead Costs from a New Factory

Karsten is one of the premier carpet manufacturers in the world. It manufactures

carpeting for both residential and commercial applications. Home sales and commercial

sales each account for about 50 percent of total revenues. The firm is organized into

three departments: Manu facturing, Residential Sales, and Commercial Sales.

Manufacturing is a cost center and the two sales departments are profit centers. The

full cost of each roll of carpeting produced (including fully absorbed overhead) is

transferred to the sales department ordering the carpet. The evaluation of the sales

departments includes the fully absorbed cost of each roll as the transfer price.

The current manufacturing plant is operating at capacity. A new plant is being built

that will more than double capacity. Within two years, management believes that its

businesses will grow such that most of the excess capacity will be eliminated. When the

new plant comes online, the plan is for one plant to produce exclusively commercial

carpeting and the other to produce exclusively residential carpeting. This change will

simplify scheduling, ordering, and inventory control in each plant. It will also create

some economies of scale by producing longer mill runs. Nevertheless, it will take a

couple of years before these economies of scale can be realized.

Each mill produces carpeting in four-meter-wide rolls of up to 100 meters in length.

The output of each mill is measured in terms of meters of four-meter rolls produced.

Overhead is assigned to carpet rolls using carpet meters produced in the mill. The cost

structure of each plant is as follows:

Old Plant

New Plant

Normal machine hours per year

6,000

5,000

Normal carpet meters per hour

Normal capacity

1,000

1,400

6,000,000 meters

7,000,000 meters

Annual manufacturing overhead costs

excluding accounting depreciation

€15,000,000

€21,000,000

Accounting depreciation per year

€ 6,000,000

€21,000,000

Karsten's new mill will run at higher speed and therefore produce more meters of

carpet per hour. Moreover, the new mill will use 15 percent less direct materials and

direct labor because the new machines, being more automated, produce less scrap and

497

Transcribed Image Text:require less direct labor per meter. A job sheet run at the old mill is as follows:

Carpet A6106: (100-meter roll)

Direct materials

€ 800

Direct labor

600

Direct costs

€1,400

Although the new mill has lower direct costs of carpet production than the old mill

does, the new facility's higher overhead costs per meter have the sales department

managers worried. They already are lobbying senior management to have the old mill

assigned to produce their products. The Commercial Sales department manager argues,

“More of my customers are located closer to the old plant than are the Residential Sales

department's customers. Therefore, to economize on transportation costs, my products

should be produced in the old plant." The Residential Sales department manager

counters with the argument, "Transportation costs are less than 1 percent of total

revenues. The new plant should produce commercial products because we expect new

commercial products to use more synthetic materials and the latest technology at the

new mill is better able to adapt to the new synthetics." Senior management is worried

about how to deal with the two sales department managers' reluctance to have their

products produced at the new plant. One suggestion put forth is for each plant to

produce about half of Commercial Sales products and about half of Residential Sales

products. However, this proposal would eliminate most of the economies of scale that

would result from specializing production in each plant to one market segment.

a. Calculate the overhead rates for the new plant and the old plant, where overhead

is assigned to carpet based on normal meters per year.

b. Calculate the expected total cost of carpet A6106, if run at the old mill and if run

at the new mill.

c. Put forth two new potential solutions that overcome the desire of the Residential

and Commercial Sales department managers to have their products produced in

the old plant. Discuss the pros and cons of your two solutions.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Accounting (Text Only)

Accounting

ISBN:

9781285743615

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781285866307

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Accounting (Text Only)

Accounting

ISBN:

9781285743615

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781285866307

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781337119207

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning