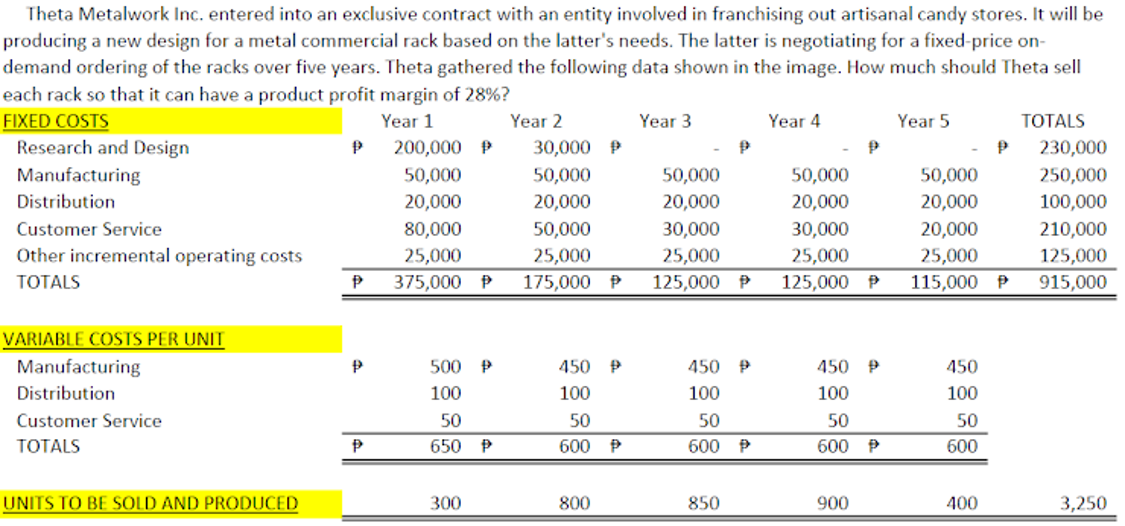

Theta Metalwork Inc. entered into an exclusive contract with an entity involved in franchising out artisanal candy stores. It will be producing a new design for a metal commercial rack based on the latter's needs. The latter is negotiating for a fixed-price on- demand ordering of the racks over five years. Theta gathered the following data shown in the image. How much should Theta sell each rack so that it can have a product profit margin of 28%? FIXED COSTS Research and Design Year 1 Year 2 Year 3 Year 4 Year 5 ТОTALS 200,000 P 30,000 P 230,000 Manufacturing 50,000 50,000 20,000 50,000 50,000 50,000 250,000 Distribution 20,000 20,000 20,000 20,000 100,000 Customer Service 80,000 50,000 30,000 30,000 20,000 210,000 Other incremental operating costs 25,000 25,000 115,000 P 25,000 25,000 25,000 125,000 TOTALS 375,000 P 175,000 P 125,000 P 125,000 915,000 VARIABLE COSTS PER UNIT Manufacturing 500 P 450 P 450 P 450 P 450 Distribution 100 100 100 100 100 Customer Service 50 50 50 50 50 ТОTALS 650 600 600 P 600 P 600 UNITS TO BE SOLD AND PRODUCED 300 800 850 900 400 3,250

Theta Metalwork Inc. entered into an exclusive contract with an entity involved in franchising out artisanal candy stores. It will be producing a new design for a metal commercial rack based on the latter's needs. The latter is negotiating for a fixed-price on- demand ordering of the racks over five years. Theta gathered the following data shown in the image. How much should Theta sell each rack so that it can have a product profit margin of 28%? FIXED COSTS Research and Design Year 1 Year 2 Year 3 Year 4 Year 5 ТОTALS 200,000 P 30,000 P 230,000 Manufacturing 50,000 50,000 20,000 50,000 50,000 50,000 250,000 Distribution 20,000 20,000 20,000 20,000 100,000 Customer Service 80,000 50,000 30,000 30,000 20,000 210,000 Other incremental operating costs 25,000 25,000 115,000 P 25,000 25,000 25,000 125,000 TOTALS 375,000 P 175,000 P 125,000 P 125,000 915,000 VARIABLE COSTS PER UNIT Manufacturing 500 P 450 P 450 P 450 P 450 Distribution 100 100 100 100 100 Customer Service 50 50 50 50 50 ТОTALS 650 600 600 P 600 P 600 UNITS TO BE SOLD AND PRODUCED 300 800 850 900 400 3,250

Principles of Cost Accounting

17th Edition

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Edward J. Vanderbeck, Maria R. Mitchell

Chapter10: Cost Analysis For Management Decision Making

Section: Chapter Questions

Problem 13P: Deuce Sporting Goods manufactures a high-end model tennis racket. The company’s forecasted income...

Related questions

Question

please help me answer the following in good accountng form

Transcribed Image Text:Theta Metalwork Inc. entered into an exclusive contract with an entity involved in franchising out artisanal candy stores. It will be

producing a new design for a metal commercial rack based on the latter's needs. The latter is negotiating for a fixed-price on-

demand ordering of the racks over five years. Theta gathered the following data shown in the image. How much should Theta sell

each rack so that it can have a product profit margin of 28%?

FIXED COSTS

Research and Design

Year 1

Year 2

Year 3

Year 4

Year 5

ТОTALS

200,000 P

30,000 P

230,000

Manufacturing

50,000

50,000

20,000

50,000

50,000

50,000

250,000

Distribution

20,000

20,000

20,000

20,000

100,000

Customer Service

80,000

50,000

30,000

30,000

20,000

210,000

Other incremental operating costs

25,000

25,000

115,000 P

25,000

25,000

25,000

125,000

TOTALS

375,000 P

175,000 P

125,000 P

125,000

915,000

VARIABLE COSTS PER UNIT

Manufacturing

500 P

450 P

450 P

450 P

450

Distribution

100

100

100

100

100

Customer Service

50

50

50

50

50

ТОTALS

650

600

600 P

600 P

600

UNITS TO BE SOLD AND PRODUCED

300

800

850

900

400

3,250

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning