Chapter1: Making Economics Decisions

Section: Chapter Questions

Problem 1QTC

Related questions

Question

True or False: The shape of the total physical product curve reflects the law of increasing marginal returns.

A.) True

B.) False

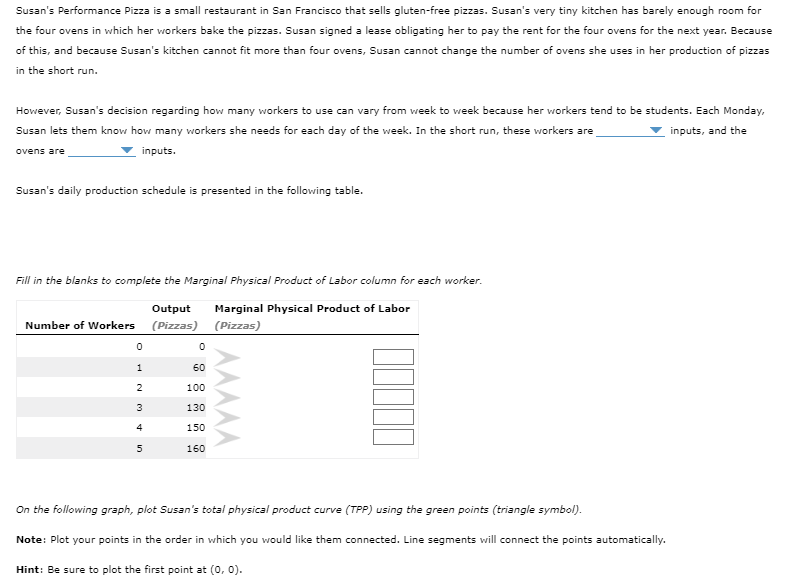

Transcribed Image Text:Susan's Performance Pizza is a small restaurant in San Francisco that sells gluten-free pizzas. Susan's very tiny kitchen has barely enough room for

the four ovens in which her workers bake the pizzas. Susan signed a lease obligating her to pay the rent for the four ovens for the next year. Because

of this, and because Susan's kitchen cannot fit more than four ovens, Susan cannot change the number of ovens she uses in her production of pizzas

in the short run.

However, Susan's decision regarding how many workers to use can vary from week to week because her workers tend to be students. Each Monday,

Susan lets them know how many workers she needs for each day of the week. In the short run, these workers are

inputs, and the

inputs.

ovens are

Susan's daily production schedule is presented in the following table.

Fill in the blanks to complete the Marginal Physical Product of Labor column for each worker.

Output

Marginal Physical Product of Labor

(Pizzas)

(Pizzas)

Number of Workers

0

1

2

3

4

5

0

60

100

130

150

160

On the following graph, plot Susan's total physical product curve (TPP) using the green points (triangle symbol).

Note: Plot your points in the order in which you would like them connected. Line segments will connect the points automatically.

Hint: Be sure to plot the first point at (0, 0).

Transcribed Image Text:QUANTITY OF OUTPUT (Pizzas)

200

180

TOTAL COST(Dollars)

160

140

120

100

80

60

40

20

0

200

180

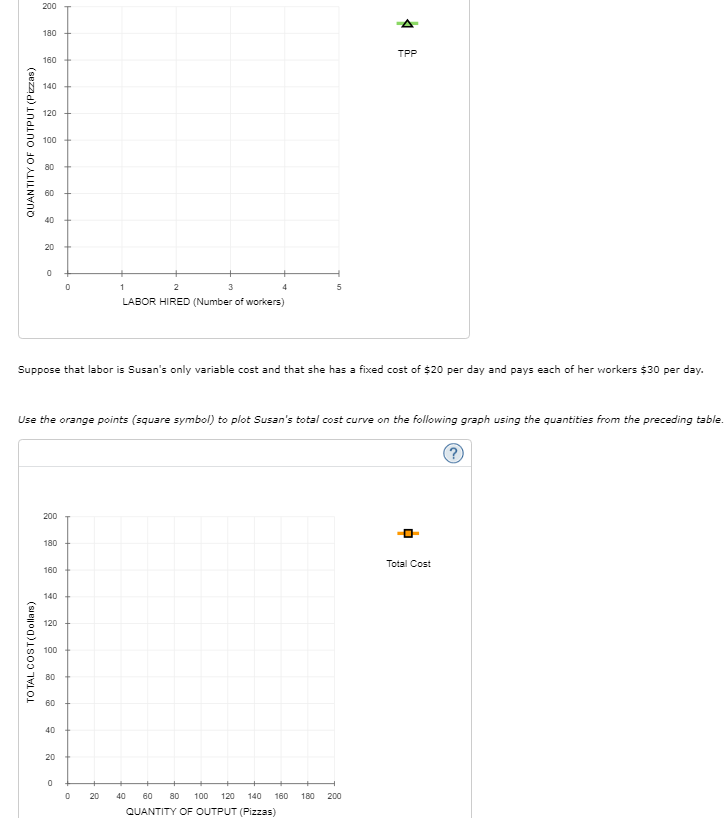

Suppose that labor is Susan's only variable cost and that she has a fixed cost of $20 per day and pays each of her workers $30 per day.

160

Use the orange points (square symbol) to plot Susan's total cost curve on the following graph using the quantities from the preceding table.

140

120

100

80

60

40

0

20

0

1

2

LABOR HIRED (Number of workers)

3

0

4

20

TPP

40 60 80 100 120 140 160 180 200

QUANTITY OF OUTPUT (Pizzas)

-O-

Total Cost

?

Expert Solution

Step 1

The law of increasing marginal returns also called the law of diminishing costs states that as far as all the variables are kept constant, there will be extra efficiency i.e. the extra output that can be manufactured by adding extra labor or any other input. There would also be reduced marginal cost i.e. the extra cost incurred in producing one extra unit. The law of increasing and diminishing marginal returns is used by companies to know the optimum choice that would increase their efficiency.

Thanks for the questions. As you have posted multiple questions, as per guidelines we will answer the first question for you. Please post the second question separately.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics (12th Edition)

Economics

ISBN:

9780134078779

Author:

Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:

PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:

9780134870069

Author:

William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:

PEARSON

Principles of Economics (12th Edition)

Economics

ISBN:

9780134078779

Author:

Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:

PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:

9780134870069

Author:

William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:

PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:

9781305585126

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-…

Economics

ISBN:

9781259290619

Author:

Michael Baye, Jeff Prince

Publisher:

McGraw-Hill Education