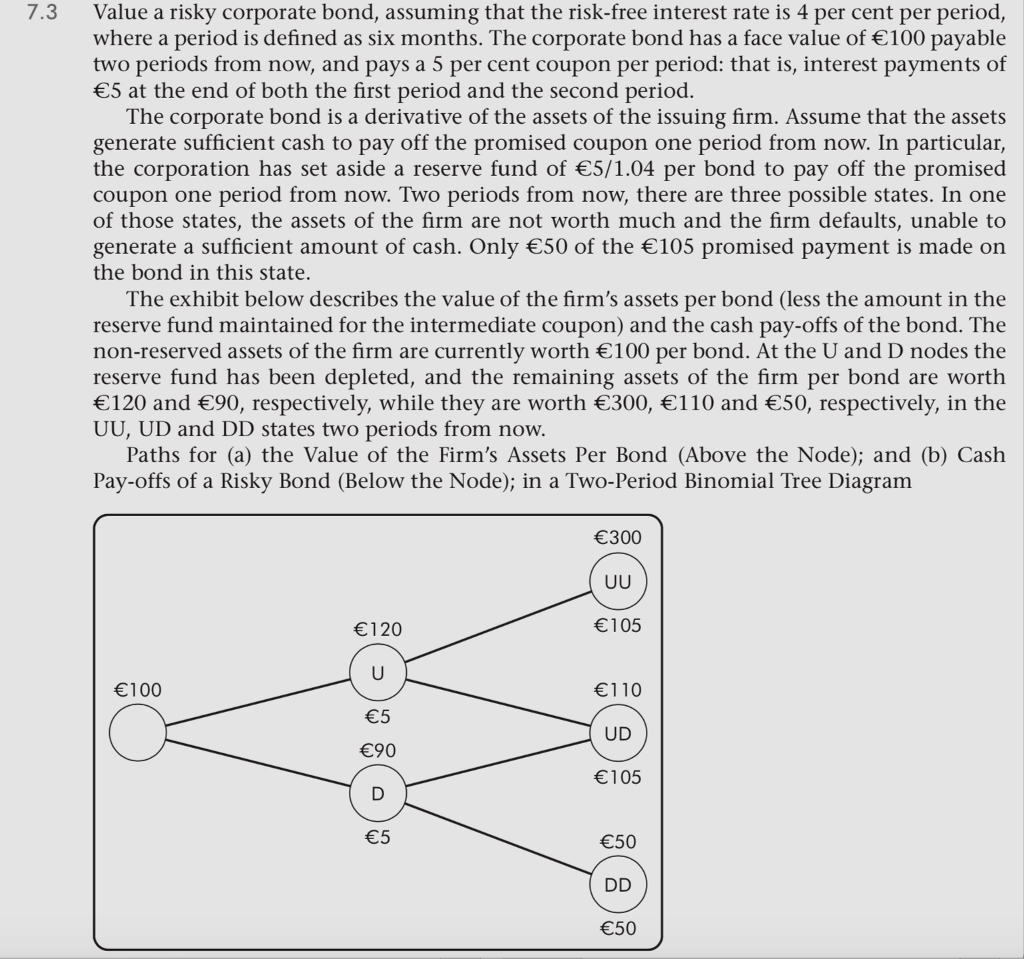

Value a risky corporate bond, assuming that the risk-free interest rate is 4 per cent per period, where a period is defined as six months. The corporate bond has a face value of €100 payable two periods from now, and pays a 5 per cent coupon per period: that is, interest payments of €5 at the end of both the first period and the second period. The corporate bond is a derivative of the assets of the issuing firm. Assume that the assets generate sufficient cash to pay off the promised coupon one period from now. In particular, the corporation has set aside a reserve fund of €5/1.04 per bond to pay off the promised coupon one period from now. Two periods from now, there are three possible states. In one of those states, the assets of the firm are not worth much and the firm defaults, unable to generate a sufficient amount of cash. Only €50 of the €105 promised payment is made on the bond in this state. The exhibit below describes the value of the firm's assets per bond (less the amount in the reserve fund maintained for the intermediate coupon) and the cash pay-offs of the bond. The non-reserved assets of the firm are currently worth €100 per bond. At the U and D nodes the reserve fund has been depleted, and the remaining assets of the firm per bond are worth €120 and €90, respectively, while they are worth €300, €110 and €50, respectively, in the UU, UD and DD states two periods from now. Paths for (a) the Value of the Firm's Assets Per Bond (Above the Node); and (b) Cash Pay-offs of a Risky Bond (Below the Node); in a Two-Period Binomial Tree Diagram €100 €120 U €5 €90 D €5 €300 UU €105 €110 UD €105 €50 DD €50

Value a risky corporate bond, assuming that the risk-free interest rate is 4 per cent per period, where a period is defined as six months. The corporate bond has a face value of €100 payable two periods from now, and pays a 5 per cent coupon per period: that is, interest payments of €5 at the end of both the first period and the second period. The corporate bond is a derivative of the assets of the issuing firm. Assume that the assets generate sufficient cash to pay off the promised coupon one period from now. In particular, the corporation has set aside a reserve fund of €5/1.04 per bond to pay off the promised coupon one period from now. Two periods from now, there are three possible states. In one of those states, the assets of the firm are not worth much and the firm defaults, unable to generate a sufficient amount of cash. Only €50 of the €105 promised payment is made on the bond in this state. The exhibit below describes the value of the firm's assets per bond (less the amount in the reserve fund maintained for the intermediate coupon) and the cash pay-offs of the bond. The non-reserved assets of the firm are currently worth €100 per bond. At the U and D nodes the reserve fund has been depleted, and the remaining assets of the firm per bond are worth €120 and €90, respectively, while they are worth €300, €110 and €50, respectively, in the UU, UD and DD states two periods from now. Paths for (a) the Value of the Firm's Assets Per Bond (Above the Node); and (b) Cash Pay-offs of a Risky Bond (Below the Node); in a Two-Period Binomial Tree Diagram €100 €120 U €5 €90 D €5 €300 UU €105 €110 UD €105 €50 DD €50

Chapter5: The Cost Of Money (interest Rates)

Section: Chapter Questions

Problem 19PROB

Related questions

Question

Transcribed Image Text:Value a risky corporate bond, assuming that the risk-free interest rate is 4 per cent per period,

where a period is defined as six months. The corporate bond has a face value of €100 payable

two periods from now, and pays a 5 per cent coupon per period: that is, interest payments of

€5 at the end of both the first period and the second period.

The corporate bond is a derivative of the assets of the issuing firm. Assume that the assets

generate sufficient cash to pay off the promised coupon one period from now. In particular,

the corporation has set aside a reserve fund of €5/1.04 per bond to pay off the promised

coupon one period from now. Two periods from now, there are three possible states. In one

of those states, the assets of the firm are not worth much and the firm defaults, unable to

generate a sufficient amount of cash. Only €50 of the €105 promised payment is made on

the bond in this state.

7.3

The exhibit below describes the value of the firm's assets per bond (less the amount in the

reserve fund maintained for the intermediate coupon) and the cash pay-offs of the bond. The

non-reserved assets of the firm are currently worth €100 per bond. At the U and D nodes the

reserve fund has been depleted, and the remaining assets of the firm per bond are worth

€120 and €90, respectively, while they are worth €300, €110 and €50, respectively, in the

UU, UD and DD states two periods from now.

Paths for (a) the Value of the Firm's Assets Per Bond (Above the Node); and (b) Cash

Pay-offs of a Risky Bond (Below the Node); in a Two-Period Binomial Tree Diagram

€300

UU

€120

€105

€100

€110

€5

UD

€90

€105

€5

€50

DD

€50

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning