Wildhorse Industries works hard to keep pace with demand for its modern chandelier. To get it out the door, Wildhorse first machines raw materials into key component parts. Next, the component parts are assembled. These two processing departments work together, coordinating the output from the machining process into the assembly process. All DM resources are added at the beginning of the machining process, while conversion costs are added evenly throughout the process. For May, the following information was available for the machining process. Units DM Conversion Costs Units in beginning WIP Inventory 700 Beginning WIP Inventory degree of completion 2 70% Costs in beginning WIP Inventory $36,500 $19,650 New units started 9,200 Costs added to WIP Inventory this period $349.600 $186,270 Units completed 9,000 Units in ending WIP Inventory 900 Ending WIP Inventory degree of completion ? 40% (b) Determine the total cost of units completed and the cost of units in ending WIP Inventory-Machining in May by completing Steps 1-5 of the template, assuming Wildhorse Industries uses the weighted-average method of process costing. Total cost of units completed $ Cost of units in ending WIP Inventory $ 品(Ctrl)、

Wildhorse Industries works hard to keep pace with demand for its modern chandelier. To get it out the door, Wildhorse first machines raw materials into key component parts. Next, the component parts are assembled. These two processing departments work together, coordinating the output from the machining process into the assembly process. All DM resources are added at the beginning of the machining process, while conversion costs are added evenly throughout the process. For May, the following information was available for the machining process. Units DM Conversion Costs Units in beginning WIP Inventory 700 Beginning WIP Inventory degree of completion 2 70% Costs in beginning WIP Inventory $36,500 $19,650 New units started 9,200 Costs added to WIP Inventory this period $349.600 $186,270 Units completed 9,000 Units in ending WIP Inventory 900 Ending WIP Inventory degree of completion ? 40% (b) Determine the total cost of units completed and the cost of units in ending WIP Inventory-Machining in May by completing Steps 1-5 of the template, assuming Wildhorse Industries uses the weighted-average method of process costing. Total cost of units completed $ Cost of units in ending WIP Inventory $ 品(Ctrl)、

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter3: Cost Behavior

Section: Chapter Questions

Problem 14E: Vargas, Inc., produces industrial machinery. Vargas has a machining department and a group of direct...

Related questions

Question

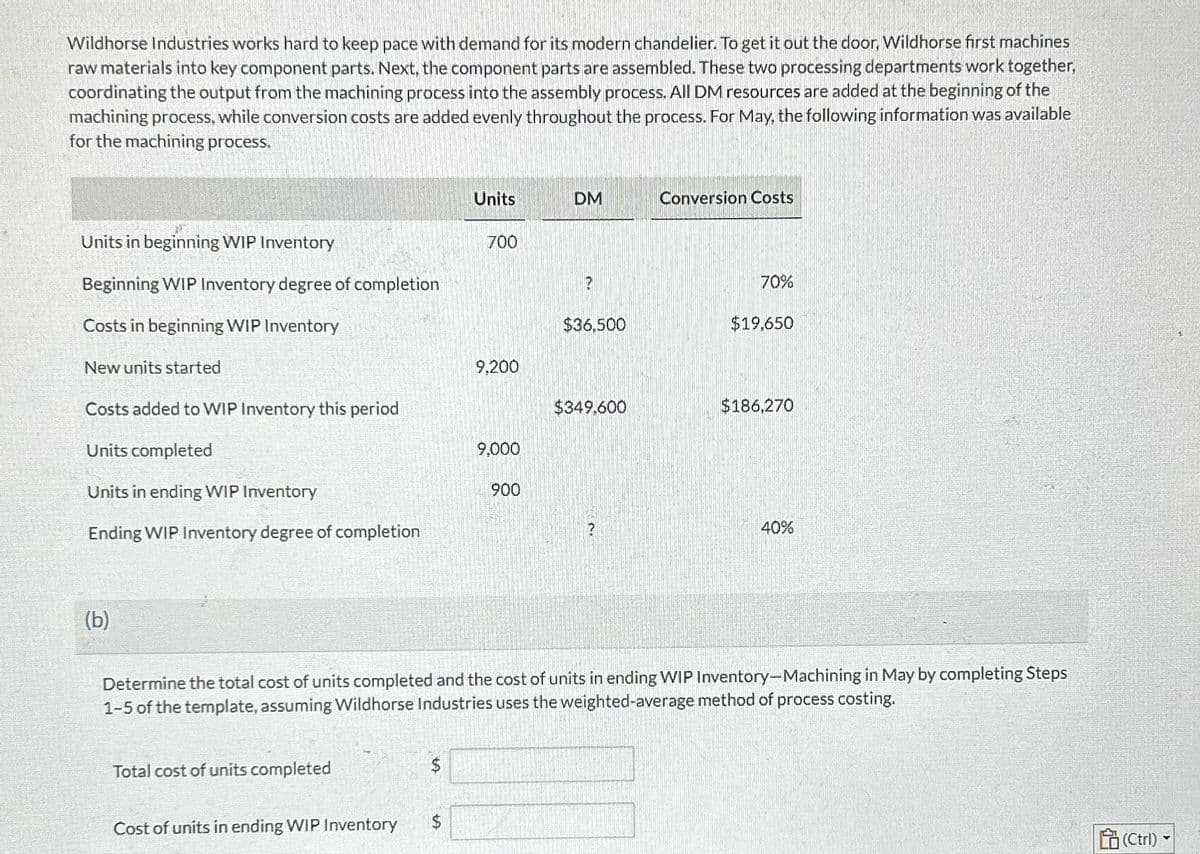

Transcribed Image Text:Wildhorse Industries works hard to keep pace with demand for its modern chandelier. To get it out the door, Wildhorse first machines

raw materials into key component parts. Next, the component parts are assembled. These two processing departments work together,

coordinating the output from the machining process into the assembly process. All DM resources are added at the beginning of the

machining process, while conversion costs are added evenly throughout the process. For May, the following information was available

for the machining process.

Units

DM

Conversion Costs

Units in beginning WIP Inventory

700

Beginning WIP Inventory degree of completion

2

70%

Costs in beginning WIP Inventory

$36,500

$19,650

New units started

9,200

Costs added to WIP Inventory this period

$349.600

$186,270

Units completed

9,000

Units in ending WIP Inventory

900

Ending WIP Inventory degree of completion

?

40%

(b)

Determine the total cost of units completed and the cost of units in ending WIP Inventory-Machining in May by completing Steps

1-5 of the template, assuming Wildhorse Industries uses the weighted-average method of process costing.

Total cost of units completed

$

Cost of units in ending WIP Inventory

$

品(Ctrl)、

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning