1. Material Variance 2. Direct Labor Costs Variances (Direct 3. Factory Overhead Variance

1. Material Variance 2. Direct Labor Costs Variances (Direct 3. Factory Overhead Variance

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter9: Evaluating Variances From Standard Costs

Section: Chapter Questions

Problem 3PA: Direct materials, direct labor, and factory overhead cost variance analysis Mackinaw Inc. processes...

Related questions

Question

Please answer the required question

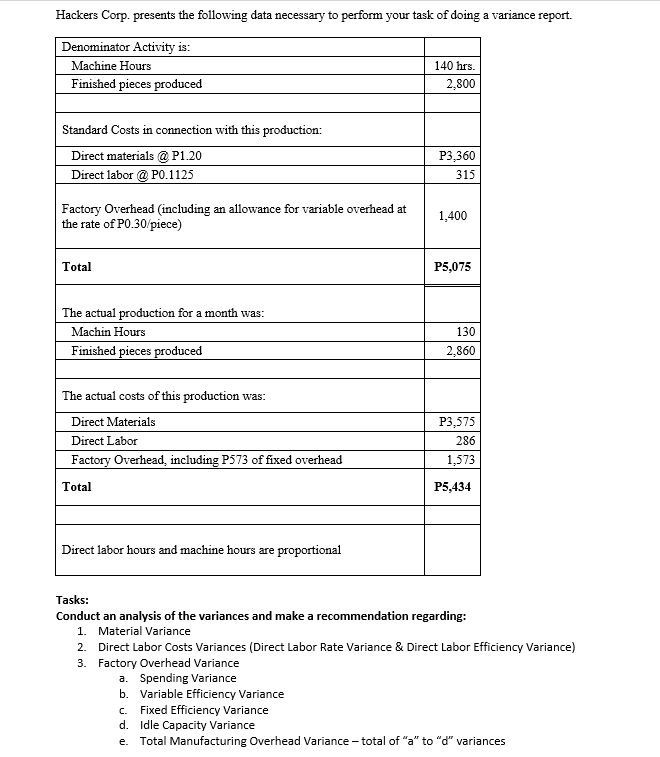

Transcribed Image Text:Hackers Corp. presents the following data necessary to perform your task of doing a variance report.

Denominator Activity is:

Machine Hours

140 hrs.

Finished pieces produced

2,800

Standard Costs in connection with this production:

Direct materials @ P1.20

P3,360

Direct labor @ PO.1125

315

Factory Overhead (including an allowance for variable overhead at

1,400

the rate of PO.30/piece)

Total

P5,075

The actual production for a month was:

Machin Hours

130

Finished pieces produced

2,860

The actual costs of this production was:

Direct Materials

P3,575

Direct Labor

286

Factory Overhead, including P573 of fixed overhead

1,573

Total

P5,434

Direct labor hours and machine hours are proportional

Tasks:

Conduct an analysis of the variances and make a recommendation regarding:

1. Material Variance

2. Direct Labor Costs Variances (Direct Labor Rate Variance & Direct Labor Efficiency Variance)

3. Factory Overhead Variance

a. Spending Variance

b. Variable Efficiency Variance

c. Fixed Efficiency Variance

d. Idle Capacity Variance

Total Manufacturing Overhead Variance - total of "a" to "d" variances

e.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning