Concept explainers

Videos

Direct materials and direct labor variance analysis

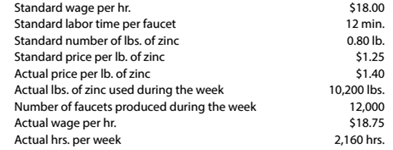

Faucet Industries Inc. manufactures faucets in a small manufacturing facility. The faucets are made from zinc. Faucet Industries has 60 employees. Each employee presently provides 36 hours of labor per week. Information about a production week is as follows:

Instructions

Determine (a) the

(a)

Concept Introduction:

Standard cost is an accounting system which is used by manufacturers to know the difference between actual cost and standard cost of product.

To Compute:

The standard cost per unit for direct material and direct labor.

Answer to Problem 13.4P

The standard cost per unit for direct material is

Explanation of Solution

Details of material and labour are given in following table:

| Materials and Labours | ||||||

| Particulars | Standard Quantity | Standard Price(per unit) | Standard Cost | Actual Quantity | Actual Price(Per unit) | Actual cost |

| Material (lbs) | | | | | | |

| Labour (hrs) | | | | | | |

Now, the calculation of standard cost per unit of direct material and direct labour:

| Particulars | Amount ($)( | Amount per Faucet |

| Material | | |

| Labour | | |

| | |

(b)

Concept Introduction:

Standard cost is an accounting system which is used by manufacturers to know the difference between actual cost and standard cost of product.

To Compute:

The price variance, quantity variance and cost variance direct material.

Answer to Problem 13.4P

The direct material price variance is

The direct material quantity variance is

The direct material cost variance is

Explanation of Solution

Computation of direct material price variance is as follows:

Direct material price variance is adverse as the actual price is more than standard price.

Computation of Direct material quantity variance is as follows:

Direct material quantity variance is adverse as the actual quantity is more than standard quantity.

Computation of Direct material cost variance is as follows:

The direct material cost variance is also adverse.

(c)

Concept Introduction:

Standard cost is an accounting system which is used by manufacturers to know the difference between actual cost and standard cost of product.

To Compute:

The rate variance, time variance and cost variance of direct labour.

Answer to Problem 13.4P

The direct labourrate variance is

The direct labour time variance is

The direct labour cost variance is

Explanation of Solution

Computation of direct labour rate variance is as follows:

Direct labour rate variance is adverse as the actual rate per hour is more than standard rate per hour.

Computation of Direct labor time variance is as follows:

Direct labour time variance is Favorable as the actual direct labour hours is less than standard direct labour hours.

Computation of Direct labour cost variance is as follows:

The direct labour cost variance is also Favorable.

Want to see more full solutions like this?

Chapter 13 Solutions

Survey of Accounting (Accounting I)

- Direct materials, direct labor, and factory overhead cost variance analysis Mackinaw Inc. processes a base chemical into plastic. Standard costs and actual costs for direct materials, direct labor, and factory overhead incurred for the manufacture of 40,000 units of product were as follows: Each unit requires 0.3 hour of direct labor. Instructions Determine (A) the direct materials price variance, direct materials quantity variance, and total direct materials cost variance; (B) the direct labor rate variance, direct labor time variance, and total direct labor cost variance; and (C) the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance.arrow_forwardStandard cost summary; materials and labor cost variances Perkins Processors Inc. produces an average of 10,000 units each month. The factory standards are 20,000 hours of direct labor and 10,000 pounds of materials for this volume. The standard cost of direct labor is 9.00 per hour, and the standard cost of materials is 4.00 per pound. The standard factory overhead at this level of production is 20,000. During the current month the production and cost reports reflected the following information: On the basis of this information: 1. Prepare a standard cost summary. 2. Calculate the materials (use the materials purchase price variance) and labor cost variances, and indicate whether they are favorable or unfavorable, using the formulas on pages 421422 and 424.arrow_forwardCalculation of materials and labor variances Fritz Corp. manufactures and sells a single product. The company uses a standard cost system. The standard cost per unit of product follows: The charges to the manufacturing department for November, when 5,000 units were produced, follow: The Purchasing department normally buys about the same quantity as is used in production during a month. In November, 5,500 lb were purchased at a price of $2.90 per pound. Required: Calculate the following from standard costs for the data given, using the formulas on pages 421–422 and 424: Materials quantity variance. Materials purchase price variance (at time of purchase). Labor efficiency variance. Labor rate variance. Give some reasons as to why both the materials quantity variance and labor efficiency variance might be unfavorable.arrow_forward

- Cost and production data for Binghamton Beverages Inc. are presented as follows: Required: Calculate net variances for materials, labor, and factory overhead. Calculate specific materials and labor variances by department, using the diagram format in Figure 8-4. Comment on the possible causes for each of the variances that you computed. Make all journal entries to record production costs in Work in Process and Finished Goods. Determine the balance of ending Work in Process in each department. Assume that 4,000 units were sold at $40 each. Calculate the gross margin based on standard cost. Calculate the gross margin based on actual cost. Why does the gross margin at actual cost differ from the gross margin at standard cost. As the plant controller, you present the variance report in Item 1 above to Paul Crooke, the plant manager. After reading it, Paul states: “If we present this performance report to corporate with that large unfavorable labor variance in Blending, nobody in the plant will receive a bonus. Those standard hours of 5,500 are way too tight for this production process. Fifty-eight hundred hours would be more reasonable, and that would result in a favorable labor efficiency variance that would more than offset the unfavorable labor rate variance. Please redo the variance calculations using 5,800 hours as the standard.” You object, but Paul ends the conversation with, “That is an order.” What standards of ethical professional practice would be violated if you adhered to Paul’s order? How would you attempt to resolve this ethical conflict?arrow_forwardGeorgia Gasket Co. budgets 8,000 direct labor hours for the year. The total overhead budget is expected to amount to 20,000. The standard cost for a unit of the companys product estimates the variable overhead as follows: The actual data for the period follow: Using the four-variance method, calculate the overhead variances. (Hint: First compute the budgeted fixed overhead rate.)arrow_forwardCalculating factory overhead: two variances Munoz Manufacturing Co. normally produces 10,000 units of product X each month. Each unit requires 2 hours of direct labor, and factory overhead is applied on a direct labor hour basis. Fixed costs and variable costs in factory overhead at the normal capacity are 2.50 and 1.50 per direct labor hour, respectively. Cost and production data for May follow: a. Calculate the flexible-budget variance. b. Calculate the production-volume variance. c. Was the total factory overhead under- or overapplied? By what amount?arrow_forward

- Materials and labor variances Fausto Fabricators Inc. uses a standard cost system to account for its single product. The standards established for the product include the following: The following operating data came from the records for the month: In process, beginning inventory, none. In process, ending inventory, 800 units, 80% complete as to labor; material is issued at the beginning of processing. Completed during the month, 5,600 units. Materials issued to production were 51,680 lb @ .55 per pound. Direct labor was 384,000 for 40,000 hours worked. Required: Calculate the following variances, using the diagram format in Figure 8-4. 1. Materials price. 2. Materials quantity. 3. Net materials variance. 4. Labor rate. 5. Labor efficiency. 6. Net labor variance. (Hint: Before determining the standard quantity for materials and labor, you must first compute the equivalent units of production for materials and labor.)arrow_forwardCalculating factory overhead: two variances Monrovia Manufacturing Inc. normally produces 10,000 units of product A each month. Each unit requires 4 hours of direct labor, and factory overhead is applied on a direct labor hour basis. Fixed costs and variable costs in factory overhead at the normal capacity are 10 and 5 per unit, respectively. Cost and production data for June follow: a. Calculate the flexible-budget variance. b. Calculate the production-volume variance. c. Was the total factory overhead under- or overapplied? By what amount?arrow_forwardCarlo Lee Corp. has established the following standard cost per unit: Although 10,000 units were budgeted, only 8,800 units were produced. The purchasing department bought 55,000 lb of materials at a cost of $123,750. Actual pounds of materials used were 54,305. Direct labor cost was $186,550 for 18,200 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forward

- Factory overhead cost variance report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 20,000 hours for production: Tannin has available 25,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 22,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Construct a factory overhead cost variance report for the Trim Department for July.arrow_forwardAt the beginning of the year, Lopez Company had the following standard cost sheet for one of its chemical products: Lopez computes its overhead rates using practical volume, which is 80,000 units. The actual results for the year are as follows: (a) Units produced: 79,600; (b) Direct labor: 158,900 hours at 18.10; (c) FOH: 831,000; and (d) VOH: 112,400. Required: 1. Compute the variable overhead spending and efficiency variances. 2. Compute the fixed overhead spending and volume variances.arrow_forwardThe normal capacity of a manufacturing plant is 30,000 direct labor hours or 20,000 units per month. Standard fixed costs are 6,000, and variable costs are 12,000. Data for two months follow: For each month, make a single journal entry to charge overhead to Work in Process, to close Factory Overhead, and to record variances. Indicate the types of variances and state whether each is favorable or unfavorable. (Hint: You must first compute the flexible-budget and production-volume variances.)arrow_forward

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College