Demand Supply P. $0 $0 900 150 750 250 700 4 300 6. 600 6. 350 8 550 400 10 450 10 12 450 12 250 550 14 100 14 700 a. What is equilibrium price and quantity in a market system with no interferences? Equilibrium price: $[ Equilibrium quantity: units b. If this wore a third-party-payer markot where the consumer pays $8, what is the quantity demanded? What is the price charged by the soller? Quantity demanded: units The price charged by the seller:

Demand Supply P. $0 $0 900 150 750 250 700 4 300 6. 600 6. 350 8 550 400 10 450 10 12 450 12 250 550 14 100 14 700 a. What is equilibrium price and quantity in a market system with no interferences? Equilibrium price: $[ Equilibrium quantity: units b. If this wore a third-party-payer markot where the consumer pays $8, what is the quantity demanded? What is the price charged by the soller? Quantity demanded: units The price charged by the seller:

Micro Economics For Today

10th Edition

ISBN:9781337613064

Author:Tucker, Irvin B.

Publisher:Tucker, Irvin B.

Chapter4: Markets In Action

Section: Chapter Questions

Problem 3SQ

Related questions

Question

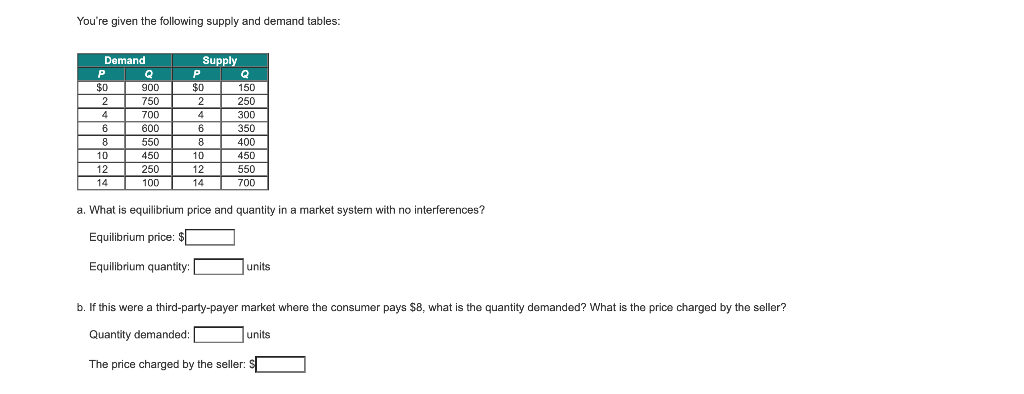

Transcribed Image Text:You're given the following supply and demand tables:

Demand

Supply

$0

900

$0

150

2

4

6

2

750

250

4

700

300

6

600

350

8

550

8

400

10

450

10

450

12

250

12

550

14

100

14

700

a. What is equilibrium price and quantity in a market system with no interferences?

Equilibrium price: $

Equilibrium quantity:

units

b. If this were a third-party-payer market where the consumer pays $8, what is the quantity demanded? What is the price charged by the seller?

Quantity demanded:

units

The price charged by the seller: S

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc