Determine the effects of 5 351 for the following taxpayers. If an amount is zero, enter "0". a. Grady exchanges qualified property, basis of $12,000 and fair market value of $18,000, for 60% of the stock of Eadie Corporation. The other 40% of the stock is owned by Pedro, who acquired it five years ago. the control of the corporation requirement, Grady has income of s Because this transaction does not meet 18,000 basis in his shares of stock. b. Trey, Amy, and Erin incorporate their businesses by forming Whitehead Corporation. As part of a prearranged plan, Trey exchanges his qualified property (basis $500; fair market value $1,000) for 100 shares in Whitehead on May 9, 2021. Amy exchanges her qualified property (basis $1,800; fair market value $2,000) for 200 shares of Whitehead Corporation stock on May 12, 2021, and Erin exchanges her qualified property (basis $2,000; fair market value $3,000) for 300 shares in Green on March 5, 2021. the control of the corporation requirement, Trey has income of $ basis in his shares of stock, Amy has income of s and S and basis in her shares of stock. Because this transaction 6,000 and Erin has income of s and basis in her shares of stock, and i

Determine the effects of 5 351 for the following taxpayers. If an amount is zero, enter "0". a. Grady exchanges qualified property, basis of $12,000 and fair market value of $18,000, for 60% of the stock of Eadie Corporation. The other 40% of the stock is owned by Pedro, who acquired it five years ago. the control of the corporation requirement, Grady has income of s Because this transaction does not meet 18,000 basis in his shares of stock. b. Trey, Amy, and Erin incorporate their businesses by forming Whitehead Corporation. As part of a prearranged plan, Trey exchanges his qualified property (basis $500; fair market value $1,000) for 100 shares in Whitehead on May 9, 2021. Amy exchanges her qualified property (basis $1,800; fair market value $2,000) for 200 shares of Whitehead Corporation stock on May 12, 2021, and Erin exchanges her qualified property (basis $2,000; fair market value $3,000) for 300 shares in Green on March 5, 2021. the control of the corporation requirement, Trey has income of $ basis in his shares of stock, Amy has income of s and S and basis in her shares of stock. Because this transaction 6,000 and Erin has income of s and basis in her shares of stock, and i

Chapter14: Choice Of Business Entity—operations And Distributions

Section: Chapter Questions

Problem 54P

Related questions

Question

N3.

Account

please answer asap

drop down options are: meets or does not meet

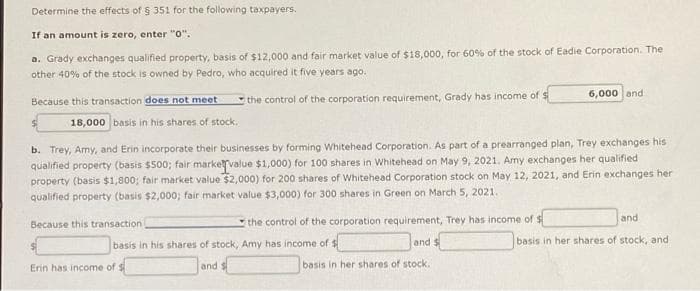

Transcribed Image Text:Determine the effects of § 351 for the following taxpayers.

If an amount is zero, enter "0".

a. Grady exchanges qualified property, basis of $12,000 and fair market value of $18,000, for 60% of the stock of Eadie Corporation. The

other 40% of the stock is owned by Pedro, who acquired it five years ago.

the control of the corporation requirement, Grady has income of $

Because this transaction does not meet

18,000 basis in his shares of stock.

b. Trey, Amy, and Erin incorporate their businesses by forming Whitehead Corporation. As part of a prearranged plan, Trey exchanges his

qualified property (basis $500; fair market value $1,000) for 100 shares in Whitehead on May 9, 2021. Amy exchanges her qualified

property (basis $1,800; fair market value $2,000) for 200 shares of Whitehead Corporation stock on May 12, 2021, and Erin exchanges her

qualified property (basis $2,000; fair market value $3,000) for 300 shares in Green on March 5, 2021.

the control of the corporation requirement, Trey has income of $

and $

basis in her shares of stock.

Because this transaction

basis in his shares of stock, Amy has income of $

and

6,000 and

Erin has income of $

and

basis in her shares of stock, and

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you