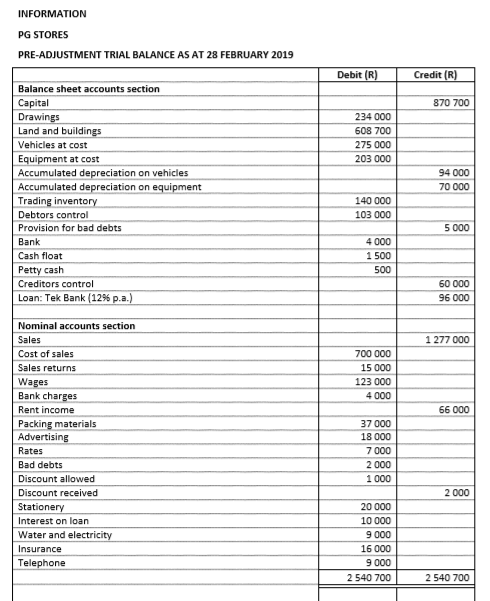

INFORMATION PG STORES PRE-ADJUSTMENT TRIAL BALANCE AS AT 28 FEBRUARY 2019 Debit (R) Credit (R) Balance sheet accounts section Capital Drawings Land and buildings Vehicles at cost 870 700 234 000 608 700 275 000 Equipment at cost Accumulated depreciation on vehicles 203 000 94 000 Accumulated depreciation on equipment Trading inventory Debtors control 70 000 140 000 103 000 Provision for bad debts 5 000 Bank 4 000 Cash float 1 500 Petty cash 500 Creditors control 60 000 Loan: Tek Bank (12% p.a.) 96 000 Nominal accounts section Sales 1 277 000 Cost of sales 700 000 Sales returns 15 000 Wages Bank charges 123 000 4 000 Rent income 66 000 Packing materials Advertising 37 000 18 000 7 000 2 000 Rates Bad debts Discount allowed 1 000 Discount received 2 000 20 000 Stationery Interest on loan 10 000 Water and electricity 9 000 Insurance 16 000 Telephone 9 000 2 540 700 2 540 700 QUESTION 1 P. Gumede is the proprietor of PG Stores. He commenced trading on 01 March 2017. At the end of the second year of trading, his bookkeeper resigned unexpectedly and Mr Gumede found that the financial statements for the year ended 28 February 2019 were incomplete. He requires your assistance in completing them. The pre-adjustment trial balance, adjustments and additional information that were extracted from the accounting records as at 28 February 2019 are presented below. REQUIRED Complete the financial statements (that appear after the adjustments and additional information) with the missing amounts and details. The entire statements must be submitted. Where applicable, show your workings in brackets. Note: The notes to the financial statements and Statement Of Changes In Equity are not required.

Good day, please assist with the calculation of below question.

ADJUSTMENTS AND ADDITIONAL INFORMATION

1. No entry was made for trading inventory that was taken by the proprietor for his personal use,

R2 000.

2. Inventories on 28 February 2019 according to physical stocktaking were as follows:

2.1 Trading inventory R135 000

2.2 Stationery R2 000

3. The telephone account of R1 000 for February 2019 was erroneously paid twice, on 25

February 2019 and 27 February 2019.

4. Rent has been received up to 31 January 2019.

5. A debtor, P. Peter, was declared insolvent. On 28 February 2019, his insolvent estate paid a

first and final dividend of 60 cents in the Rand. An amount of R1 800 was received and

recorded. The balance of his account must now be written off.

6. The provision for

7. The insurance total includes an amount of R7 200 that was paid for the period 01 November

2018 to 31 October 2019.

8. Interest on loan for February 2019 has not yet been paid. Interest is not capitalised.

Note: A repayment of R18 000 (excluding interest) is expected to be made in March 2019 to

reduce the loan balance.

9.

9.1 On vehicles at 20% per annum using the diminishing balance method.

9.2 On equipment at 15% per annum on cost. Note: Equipment with a cost price of R20 000 was

purchased and recorded on 01 December 2018.

REFER TO THE INCOMPLETE FINANCIAL STATEMENTS THAT FOLLOW AND FILL IN THE MISSING

AMOUNTS AND DETAILS. WHERE APPLICABLE, SHOW YOUR WORKINGS IN BRACKETS.

HIGHLIGHT YOUR ANSWERS FOR THE MISSING AMOUNTS OR SHOW THEM IN BOLD PRINT.

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 4 images