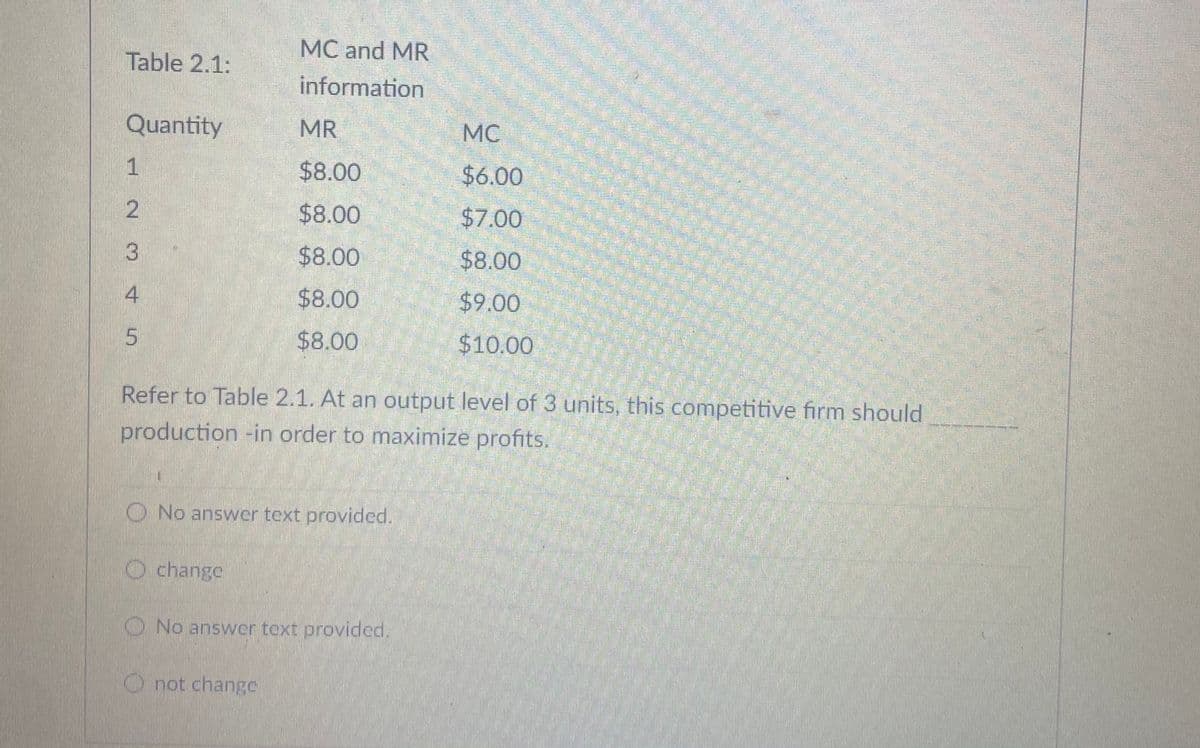

MC and MR Table 2.1: information Quantity MR MC 1 $8.00 $6.00 $8.00 $7.00 3 $8.00 $8.00 4 $8.00 $9.00 5 $8.00 $10.00 Refer to Table 2.1. At an output level of 3 units, this competitive firm should production -in order to maximize profits. O No answer text provided. change ONo answer text provided. O not change

Q: Table 2.1: information Quantity MR MC 1 $8.00 $6.00 $8.00 $7.00 3 $8.00 $8.00 4 $8.00 $9.00 5 $8.00…

A: In a competitive market, price of constant so ot is equal to marginal revenue. Profit is maximized…

Q: PROBLEM Two firms (1 and 2) with total costs TC1(q) = 60q and TC:(q)=120q (hence the marginal costs…

A: The Nash equilibrium for perfect competition is when the competitors charge maximum or more than…

Q: QUESTIONS are based on Carl's Jr case study article 1. Discuss what are potential sources of…

A: SWOT Analysis is a widely used method in organizations to provide better perspective about any…

Q: Vou own a fim in a perfectly competitive industry producing and selling gold necklaces. You know…

A: The profit boost is interactive business firms go through to guarantee the best result and value…

Q: ive

A: Competitiveness of an organization level is being defined as an organization's permanent capability…

Q: 4. Under imperfect competition with with and horizontaly differentiated products, the firm units…

A: "Since you have asked multiple questions, we will solve first question for you .. If you want any…

Q: Table Cost.EX2.2: Costs, Marginal Revenues and Outputs for a Competitive Firm Marginal Marginal…

A: Given information:- As per MC(Marginal Cost) and MR (Marginal Revenue) approach, the maximum…

Q: Why is profit rates in all competitive industries tend toward the same level? What incentive does…

A: Under perfect competition, firms sell homogeneous products and neither the producers nor the…

Q: The total cost functions of all 4 saloon are given a under: Saloon 1 TC1 = 20+5Q1 2 Saloon 2 TC2…

A: Total cost is the cost incurred by the firm in producing the total quantity. The total cost is given…

Q: (Figure: Profit Margin 3) JoJo's company data is in the graph below. JoJo would earn a positive…

A: The firm can obtain profit at the point of production where the price is greater than the average…

Q: 13) The cobalt mining company is perfectly competitive. Each existing firm and every potential…

A:

Q: QUESTION 10 In an increasing cost industry, the long-run market supply curve is because the long run…

A: D) Upward sloping; average cost Explanation: In an increasing-cost industry (when the long-run…

Q: let: MC = 12Q⁵+5Q⁶-4Q⁵-5 MR = 16Q¹⁵+15Q²-12Q⁶-10Q MP = 12X⁵+25X⁷-24X⁴-7X Determine the functions of…

A: In the mention question we have been asked to calculate the total cost, total revenue and total…

Q: MC and MR Table 2.1: information Quantity MR MC 1 $6.00 $2.00 $6.00 $4.00 $6.00 $6.00 4 $6.00 $8.00…

A: In a competitive firm, the price is constant so equal to marginal revenue. Profit is maximised at a…

Q: 2) A perfectly competitive market has demand given by Qp = 4850 – 70P. There are four firms in this…

A:

Q: A. Complete the table. A small firm operating in a purely competitive market, has fixed costs of $45…

A: Answer: (A). Given, Fixed cost = $45 Wage rate (w) = $96 per day Note: here there are two variable…

Q: Karen runs a print shop that makes posters for large companies. It is a very competitive business.…

A: The competitive market is a type of market that has many buyers and sellers, selling homogeneous…

Q: Fill the table below given Perfect Competition Conditions Quantity Demanded/ Produced Total…

A: The cost incurred in the production of final goods and services is known as the total cost. The cost…

Q: 1) For the following firm in a competitive market, COSTS Quantity Produced Total Cost Marginal Cost…

A: In a perfectly competitive market there are large number of firms selling identical products.

Q: Competitive Firm Total Total Output Fixed Variable (Q) Costs (TFC) Costs (TVC) $30.00 $0.00 3 $30.00…

A: Marginal cost is the additional cost incurred with production an additional unit sold. It is the…

Q: opic : Industry equilibrium Question : What determines the number of firms in an industry (a) in…

A: Industry is said to be in equilibrium in short run when it’s total output remains steady. Also when…

Q: Part a) True or False: In a competetive market, a firm's short run supply curve is sloping upwards…

A: a) In a perfectly competitive market, there are a large number of firms who sell identical products.…

Q: The table below shows the costs of a firm that produces handmade pottery vases in a competitive…

A: Competitive market: - it is a market condition where there are many buyers and many sellers in the…

Q: MC and MR Table 2.1: information Quantity MR MC 1 $8.00 $6.00 2 $8.00 $7.00 3. $8.00 $8.00 4. $8.00…

A: In a market, a firm decide its output level on the basis of marginal cost and marginal revenue…

Q: Suppose that the market for chicken momos is perfectly competitive with ten firms producing momos.…

A: A perfectly competitive market consists of a large number of buyers and sellers and each seller…

Q: Figure A Competitive Firm1.2 MC ATC Given P1 = $7.00 P2 = $8.50 P3 =$9.20 Q1= 100.00 AVC P3 P2 P1 MR…

A: In case of Perfect Competition, there are large number of firms selling identical products. The…

Q: ATCAVC 40 30 20 10 10 20 30 40 50 Quantity Figure 9.6 At a market price of $20, this perfectly…

A: please find the answer below.

Q: 12. If a competitive firm is currently producing a level of output at which profit is not maximized,…

A: 12. If a competitive firm is currently producing a level of output at which profit is not maximized,…

Q: MC and MR Table 2.1: information Quantity MR MC $8.00 $6.00 $8.00 $7.00 3. $8.00 $8.00 4 $8.00 $9.00…

A: At an output level of 4 units, the marginal cost is greater than marginal revenue. (MC>MR). The…

Q: Revenue and cost (dollars per unit) MC AVC 50 40 30 20 10 10 30 40 50 Output (units per day) The…

A: For a perfectly competitive firm, prices are given. And it should produce and sell output at this…

Q: 4:21 lLTE Work 3-5 3. Suppose a market is in equilibrium. The area below the demand curve and above…

A: Consumer Surplus: It refers to the difference between the maximum price the buyer is willing to pay…

Q: Table Cost.EX2: Costs and Outputs for a Competitive Firm Total Total Output Fixed Variable (Q) Costs…

A: total cost, in economics, the sum of all costs incurred by a firm in producing a certain level of…

Q: poard s Styles s Font 2. A perfectly competitive firm has the following fixed and variable costs in…

A: In perfectly competitive market, profit is maximized at a point where price is equal to marginal…

Q: TFC IVC TC MC AFC AVC ATC 100 00 100 130 30 1000 50 150 100 45 100 120 40 100 340 240 is 60.0 100…

A: A monopoly is a sole producer of a good in the market thus acting as a price maker whereas in a…

Q: Question 2 100 - 20 and the marginal cost is $4. a. How much output will this firm produce? What…

A: Market with a single firm is a monopoly which has a market power to maximize profit where marginal…

Q: MC and MR Table 2.1: information Quantity MR MC 1 $8.00 $6.00 $8.00 $7.00 3 $8.00 $8.00 4. $8.00…

A: Given At output level Q=3 MR=$8 MC=$8

Q: Output TVC (S) TFC (S) 100 1 40 100 70 100 120 100 4 180 100 5 250 100 6 330 100 This…

A: There are several key elements of a completely competitive market: 1. The market contribution of all…

Q: Explain why firms would or would not worry about future competition in each market. Explain how this…

A: Monopoly producerss don't think much about their potential income because they enforce stringent…

Q: What is the meaning of 'acceptable loss' for a perfectiý competitive firm ? Draw a graph and…

A: Answer in Step 2

Q: Table Cost.EX2: Costs and Outputs for a Competitive Firm Total Total Output Fixed Variable (Q) Costs…

A: The marginal cost is a change in the variable cost.

Q: Figure A Competitive Firm1.2 MC ATC Given P1 =$5.00 P2 = $6.00 P3 =$7.00 Q1 = 100.00 AVC P3 P2 MR P1…

A: In a competitive firm, price is constant so it is equal to marginal revenue. The firm will produce…

Q: 13) The cobalt mining company is perfectly competitive. Each existing firm and every potential…

A: Firms in perfect competition sell identical goods which makes them price takers, that is they accept…

Q: M/c question - Micro 23) When a firm in a competitive market receives $5000 in total revenue, it…

A: "Since you have asked multiple questions, we will solve first question for you .If you want specific…

Q: Figure A Competitive Firm1.2 MC ATC Given Pl =$7.00 P2 = $8.50 P3 =$9.20 Q1=100.00 AVC P3 P2 P1 MR C…

A: Answer: Average fixed cost (AFC): AFC refers to the per-unit fixed cost of production. AFC = Average…

Q: Figure A Competitive Firm1.2 MC ATC Given Pl =$7.00 P2 =S8.50 P3 = S8.80 Q1= 120.00 AVC A P3 P2 P1…

A: Total cost is the sum of variable cost and fixed cost. Fixed cost does not change with change in…

Q: 1.) What are the ways to cut firm's production costs? 2.) What determines the firm's market power…

A: Whenever a business or firm does production, it requires a lot of inputs, and to buy those inputs,…

Q: In competitive markets, there are many small firms with each firm unable to influence the market…

A: Perfect competition: The perfect competitive market is a type of market, with a large number of…

Q: stion 8 A firm in a perfectly competitive industry is currently producing 1,000 units per day at a…

A: Over the long haul, a firm accomplishes equilibrium when it changes its plant/s to deliver yield at…

Q: The table shows total cost and total revenue information for a perfectly (or purely) competitive…

A: In perfect competition there are large number of firms selling homogeneous goods.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

- Return to Figure 9.2. Suppose P0 is 10 and P1 is 11. Suppose a new firm with the same LRAC curve as the incumbent tries to bleak into the market by selling 4,000 units of output. Estimate from the graph what the new firms average cost of producing output would be. If the incumbent continues. to produce 6,000 units, how much output would the two films supply to the market? Estimate what would happen to the market price as a result of the supply of both the incumbent firm and the new entrant. Approximately how much profit would each firm earn? Figure 9.2 Economics of Scale and Natural MonoploySuppose that each firm in a competitive industry has the following costs: Total cost: TC = 50 + q2 Marginal cost: MC = q where q is an individual firms quantity produced. The market demand curve for this product is Demand:QD = 120 P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms in the market. a. What is each firms fixed cost? What is its variable cost? Give the equation for average total cost. b. Graph average-total-cost curve and the marginal-cost curve for q from 5 to 15. At what quantity is average-total-cost curve at its minimum? What is marginal cost and average total cost at that quantity? c Give the equation for each firms supply curve. d. Give the equation for the market supply curve for the short run in which the number of firms is fixed. e. What is the equilibrium price and quantity for this market in the short run? f. In this equilibrium, how much does each firm produce? Calculate each firms profit or loss. Is there incentive for firms to enter or exit? g. In the long run with free entry and exit, what is the equilibrium price and quantity in this market? h. In this long-run equilibrium, how much does each firm produce? How many firms are in the market?Suppose that the market price increases to 6, as Table 8.14 shows. What would happen to the profit-maximizing output level?

- 4. Suppose we have another firm known as Sepanyan Corporation which makes a product known as Yeghias. Suppose the firm’s FC=$8,000 and its TC=$10,000 and its AVC=$5. What is the ATC? a) $25.00 b) $67.50 c) $100.25 d) $200 e) Not enough information 5. Which of the following is true concerning a competitive firm? a) It will produce even when its economic profit is zero b) It prefers not to maximize profits c)t is the only firm in the market d) Its quantity choice will affect the market price e) People’s PED for the firm’s specific product is inelasticSuppose for a single firm thatP = 15TC = 3Q + 2Q2 (a) What is the profit-maximizing quantity? (b) What is the profit at the profit-maximizing quantity? Only typed AnswerThe table below shows the costs of a firm that produces handmade pottery vases in a competitive industry. Output AVC MC 1 3 3 2 2.50 2 3 2.17 1.5 4 1.93 1.2 5 1.74 1 6 1.67 1.3 7 1.71 2 8 2 4 9 2.44 6 10 3 8 The market price for a handmade vase is $3.75. To maximize its profit, this firm should produce vases.

- 4. You are the manager of a firm that produces products X and Y at zero cost. Youknow that different types of consumers value your two products differently, but you are unable toidentify these consumers individually at the time of the sale. In particular, you know there arethree types of consumers (100 of each type) with the following valuations for the two products: Consumer Type Product X Product Y1 $90 $ 602 $70 $1403 $40 $160 a. What are your profits if you charge $40 for product X and $60 for product Y?b. What are your profits if you charge $90 for product X and $160 for product Y?c. What are your profits if you charge $150 for a bundle containing one unit of product X andone unit of product Y?d. What are your profits if you charge $210 for a bundle containing one unit of X and one unit ofY, but also sell the…A purely competitive wheat farmer can sell any wheat he growsfor $10 per bushel. His five acres of land show diminishingreturns because some are better suited for wheat productionthan others. The first acre can produce 1,000 bushels of wheat,the second acre 900, the third 800, and so on. Draw a table withmultiple columns to help you answer the following questions.How many bushels will each of the farmer’s five acres produce?How much revenue will each acre generate? What are the TR and MR for each acre? If the marginal cost of planting and har-vesting an acre is $7,000 per acre for each of the five acres, howm any acres should the farmer plant and harvest? Note:- Don't use pen or paperThe accompanying table presents the expected cost and revenuedata for the Tucker Tomato Farm. The Tuckers produce tomatoesin a greenhouse and sell them wholesale in a price-taker market.a. Fill in the firm’s marginal cost, average variable cost,average total cost, and profit schedules.b. If the Tuckers are profit maximizers, how many tomatoesshould they produce when the market price is $500 perton? Indicate their profits.c. Indicate the firm’s output level and maximum profit if themarket price of tomatoes increases to $550 per ton.d. How many units would the Tucker Tomato Farm produce ifthe price of tomatoes fell to $450 per ton? What would bethe firm’s profits? Should the firm stay in business? Explain.

- 1. Suppose a perfectly competitive firm is operating in short run. The information of MR, Q,ATC and AVC are 15 taka, 60 unit, 45taka and 35 taka respectively. Calculate firm’sprofit/loss and total fixed cost. From these calculations and based on all the giveninformation, can you conclude about the firm’s decision in short run? Explain your reasoningwith the help of a suitable diagram. Show all the relevant information in yourdiagram.[Q=profit maximizing output and MR=marginal revenue]COURSE: MICROECONOMICS - Cournot Model:In the market for a given good there are only 2 firms satisfying the demand, and their respective total cost functions respond to the form: CTi = 10Qi + 5 and the demand is estimated to be: P = 31 - QIf the decision variable for both firms is that the quantity they will produce and realize will be decided simultaneously it is asked to:(a) calculate the profit and reaction function of each firmb) graph market equilibriumc) calculate the profits that both companies will obtain in equilibriumConsider the following production and cost functionsq=〖(10K^(2/5)+5L^(2/5))〗^(5/2)1250=20K+8LWhich implies〖MP〗_K=10〖(10K^(2/5)+5L^(2/5))〗^(3/2) K^(-3/5)〖MP〗_L=5〖(10K^(2/5)+5L^(2/5))〗^(3/2) L^(-3/5)What is the profit maximizing combination of K and L?