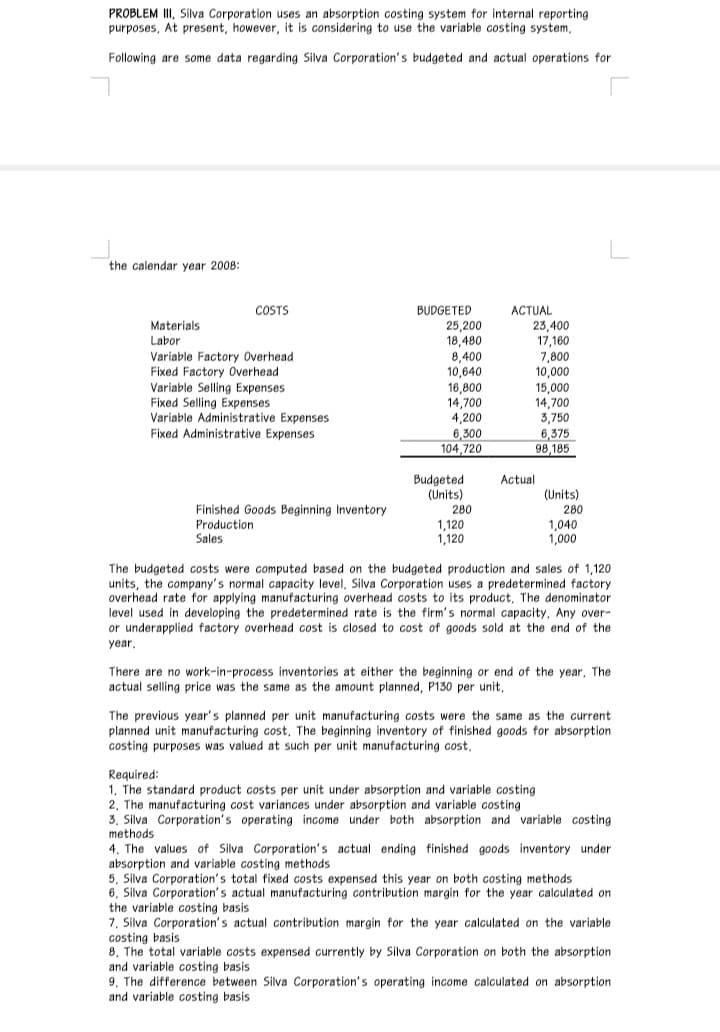

PROBLEM I, Silva Corporation uses an absorption costing system for internal reporting purposes, At present, however, it is considering to use the variable costing system, Following are some data regarding Silva Corporation's budgeted and actual operations for

PROBLEM I, Silva Corporation uses an absorption costing system for internal reporting purposes, At present, however, it is considering to use the variable costing system, Following are some data regarding Silva Corporation's budgeted and actual operations for

PROBLEM I, Silva Corporation uses an absorption costing system for internal reporting purposes, At present, however, it is considering to use the variable costing system, Following are some data regarding Silva Corporation's budgeted and actual operations for

Transcribed Image Text:PROBLEM III, Silva Corporation uses an absorption costing system for internal reporting

purposes, At present, however, it is considering to use the variable costing system,

Following are some data regarding Silva Corporation's budgeted and actual operations for

the calendar year 2008:

BUDGETED

25,200

18,480

8,400

10,640

16,800

14,700

4,200

6,300

104,720

COSTS

ACTUAL

23,400

17,160

7,800

10,000

15,000

14,700

3,750

6,375

98,185

Materials

Labor

Variable Factory Overhead

Fixed Factory Overhead

Variable Selling Expenses

Fixed Selling Expenses

Variable Administrative Expenses

Fixed Administrative Expenses

Actual

Budgeted

(Units)

(Units)

Finished Goods Beginning Inventory

Production

Sales

280

280

1,120

1,120

1,040

1,000

The budgeted costs were computed based on the budgeted production and sales of 1,120

units, the company's normal capacity level, Silva Corporation uses a predetermined factory

overhead rate for applying manufacturing overhead costs to its product, The denominator

level used in developing the predetermined rate is the firm's normal capacity. Any over-

or underapplied factory overhead cost is closed to cost of goods sold at the end of the

year,

There are no work-in-process inventories at either the beginning or end of the year, The

actual selling price was the same as the amount planned, P130 per unit,

The previous year's planned per unit manufacturing costs were the same as the current

planned unit manufacturing cost, The beginning inventory of finished goods for absorption

costing purposes was valued at such per unit manufacturing cost,

Required:

1, The standard product costs per unit under absorption and variable costing

2, The manufacturing cost variances under absorption and variable costing

3, Silva Corporation's operating income under both absorption and variable costing

methods

4, The values of Silva Corporation's actual ending finished goods inventory under

absorption and variable costing methods

5, Silva Corporation's total fixed costs expensed this year on both costing methods

6, Silva Corporation's actual manufacturing contribution margin for the year calculated on

the variable costing basis

7, Silva Corporation's actual contribution margin for the year calculated on the variable

costing basis

8, The total variable costs expensed currently by Silva Corporation on both the absorption

and variable costing basis

9, The difference between Silva Corporation's operating income calculated on absorption

and variable costing basis

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.