Refrigerator-High Volume 900 9 120 6,000 Prior to conducting the study, the factory overhead allocation was based on a single machine hour rate. The machine hour rate was $200 per hour. After conducting the activity-based costing study, assume that three activities were used to allocate the factory overhead. The new activity rate information is assumed to be as follows: Sales Order Machining Activity Setup Activity Processing Activity Activity rate $160 $240 $55 a. Complete the following table, using the single machine hour rate to determine the per-unit factory overhead for each refrigerator (Column A) and the three activity- based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity- based rate methods (Column C). If required, round all per unit answers to the nearest cent. Round percents to one decimal place. For column C, use the minus sign to indicate a negative or

Refrigerator-High Volume 900 9 120 6,000 Prior to conducting the study, the factory overhead allocation was based on a single machine hour rate. The machine hour rate was $200 per hour. After conducting the activity-based costing study, assume that three activities were used to allocate the factory overhead. The new activity rate information is assumed to be as follows: Sales Order Machining Activity Setup Activity Processing Activity Activity rate $160 $240 $55 a. Complete the following table, using the single machine hour rate to determine the per-unit factory overhead for each refrigerator (Column A) and the three activity- based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity- based rate methods (Column C). If required, round all per unit answers to the nearest cent. Round percents to one decimal place. For column C, use the minus sign to indicate a negative or

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter4: Activity-based Costing

Section: Chapter Questions

Problem 16E

Related questions

Question

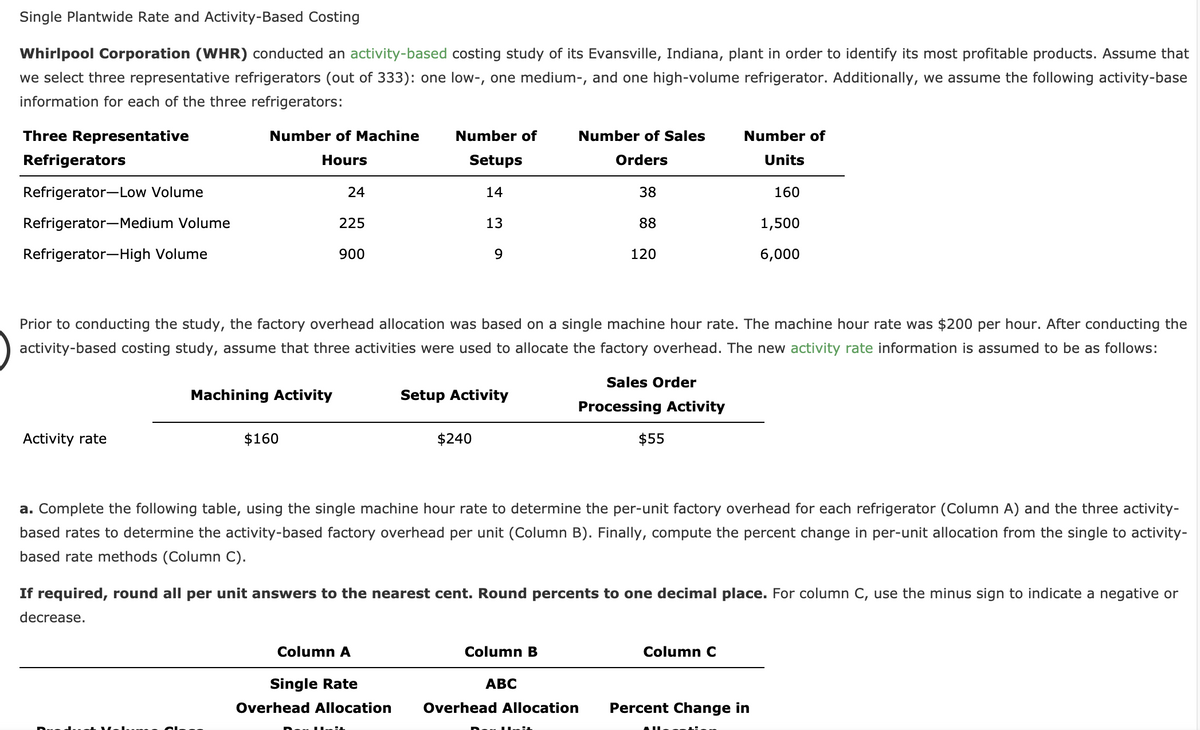

Transcribed Image Text:Single Plantwide Rate and Activity-Based Costing

Whirlpool Corporation (WHR) conducted an activity-based costing study of its Evansville, Indiana, plant in order to identify its most profitable products. Assume that

we select three representative refrigerators (out of 333): one low-, one medium-, and one high-volume refrigerator. Additionally, we assume the following activity-base

information for each of the three refrigerators:

Three Representative

Number of Machine

Number of

Number of Sales

Number of

Refrigerators

Hours

Setups

Orders

Units

Refrigerator-Low Volume

24

14

38

160

Refrigerator-Medium Volume

225

13

88

1,500

Refrigerator-High Volume

900

120

6,000

Prior to conducting the study, the factory overhead allocation was based on a single machine hour rate. The machine hour rate was $200 per hour. After conducting the

activity-based costing study, assume that three activities were used to allocate the factory overhead. The new activity rate information is assumed to be as follows:

Sales Order

Machining Activity

Setup Activity

Processing Activity

Activity rate

$160

$240

$55

a. Complete the following table, using the single machine hour rate to determine the per-unit factory overhead for each refrigerator (Column A) and the three activity-

based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity-

based rate methods (Column C).

If required, round all per unit answers to the nearest cent. Round percents to one decimal place. For column C, use the minus sign to indicate a negative or

decrease.

Column A

Column B

Column C

Single Rate

АВС

Overhead Allocation

Overhead Allocation

Percent Change in

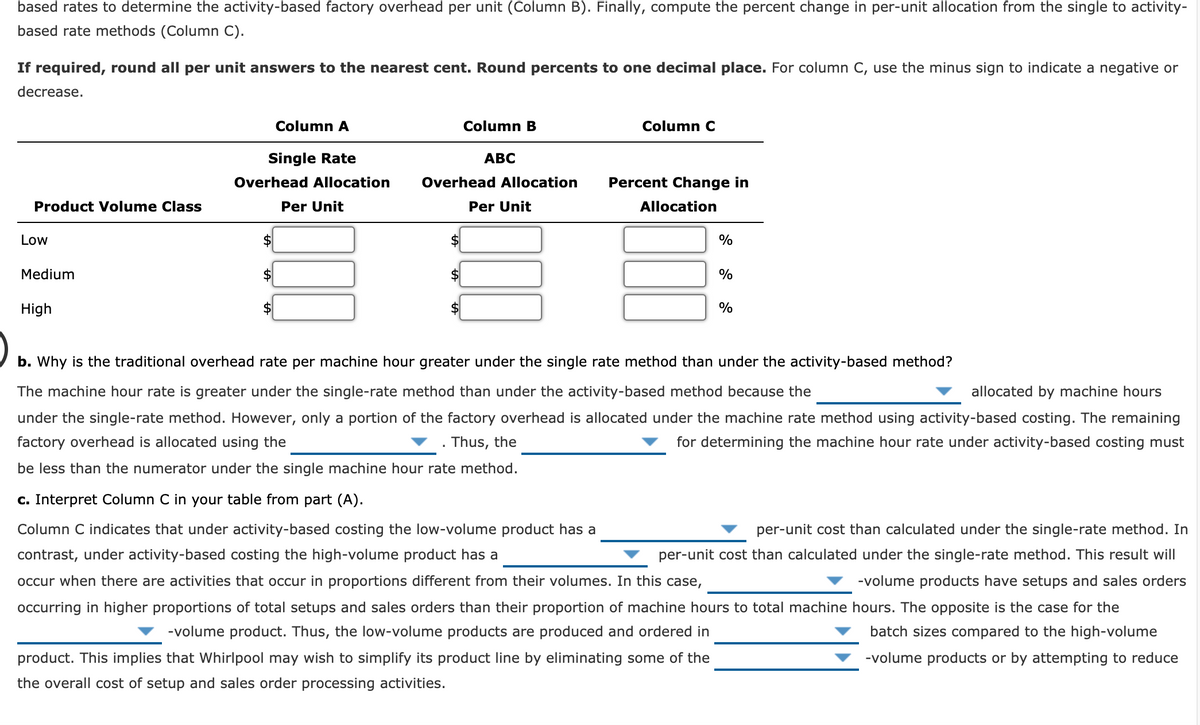

Transcribed Image Text:based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity-

based rate methods (Column C).

If required, round all per unit answers to the nearest cent. Round percents to one decimal place. For column C, use the minus sign to indicate a negative or

decrease.

Column A

Column B

Column C

Single Rate

АВС

Overhead Allocation

Overhead Allocation

Percent Change in

Product Volume Class

Per Unit

Per Unit

Allocation

Low

$

$

%

Medium

$

%

High

2$

%

b. Why is the traditional overhead rate per machine hour greater under the single rate method than under the activity-based method?

The machine hour rate is greater under the single-rate method than under the activity-based method because the

allocated by machine hours

under the single-rate method. However, only a portion of the factory overhead is allocated under the machine rate method using activity-based costing. The remaining

factory overhead is allocated using the

Thus, the

for determining the machine hour rate under activity-based costing must

be less than the numerator under the single machine hour rate method.

c. Interpret Column C in your table from part (A).

Column C indicates that under activity-based costing the low-volume product has a

per-unit cost than calculated under the single-rate method. In

contrast, under activity-based costing the high-volume product has a

per-unit cost than calculated under the single-rate method. This result will

occur when there are activities that occur in proportions different from their volumes. In this case,

-volume products have setups and sales orders

occurring in higher proportions of total setups and sales orders than their proportion of machine hours to total machine hours. The opposite is the case for the

-volume product. Thus, the low-volume products are produced and ordered in

batch sizes compared to the high-volume

product. This implies that Whirlpool may wish to simplify its product line by eliminating some of the

-volume products or by attempting to reduce

the overall cost of setup and sales order processing activities.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning