Required: 1) Prepare the journal entries for the transactions including any adjusting journal entries for the month of May 31, 2021. Place your answer under "Requirement 1“ in the "Answer" tab. A reminder to round all final numbers to the nearest dollar. Do not round during calculations. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 2) Prepare an adjusted trial balance as at May 31, 2021. Place your answer under "Requirement 2" in the "Answer" tab. Place your account titles in column H, debits in column I and credits in column J. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 3) Prepare the multi-step Income Statement for the month of May 2021. Ignore income taxes. Place your answer under "Requirement 3" in the "Answer" tab. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 4) Prepare a classified Balance Sheet at at May 31, 2021. Place your answer under "Requirement 4" in the "Answer" tab. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question.

Required: 1) Prepare the journal entries for the transactions including any adjusting journal entries for the month of May 31, 2021. Place your answer under "Requirement 1“ in the "Answer" tab. A reminder to round all final numbers to the nearest dollar. Do not round during calculations. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 2) Prepare an adjusted trial balance as at May 31, 2021. Place your answer under "Requirement 2" in the "Answer" tab. Place your account titles in column H, debits in column I and credits in column J. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 3) Prepare the multi-step Income Statement for the month of May 2021. Ignore income taxes. Place your answer under "Requirement 3" in the "Answer" tab. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question. 4) Prepare a classified Balance Sheet at at May 31, 2021. Place your answer under "Requirement 4" in the "Answer" tab. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter22: Accounting For Changes And Errors.

Section: Chapter Questions

Problem 8RE: At the end of 2019, Framber Company received 8,000 as a prepayment for renting a building to a...

Related questions

Question

100%

please help me with this question. I would be very appreciate if it could be done on excel

Thanks a lot

i'll vote up

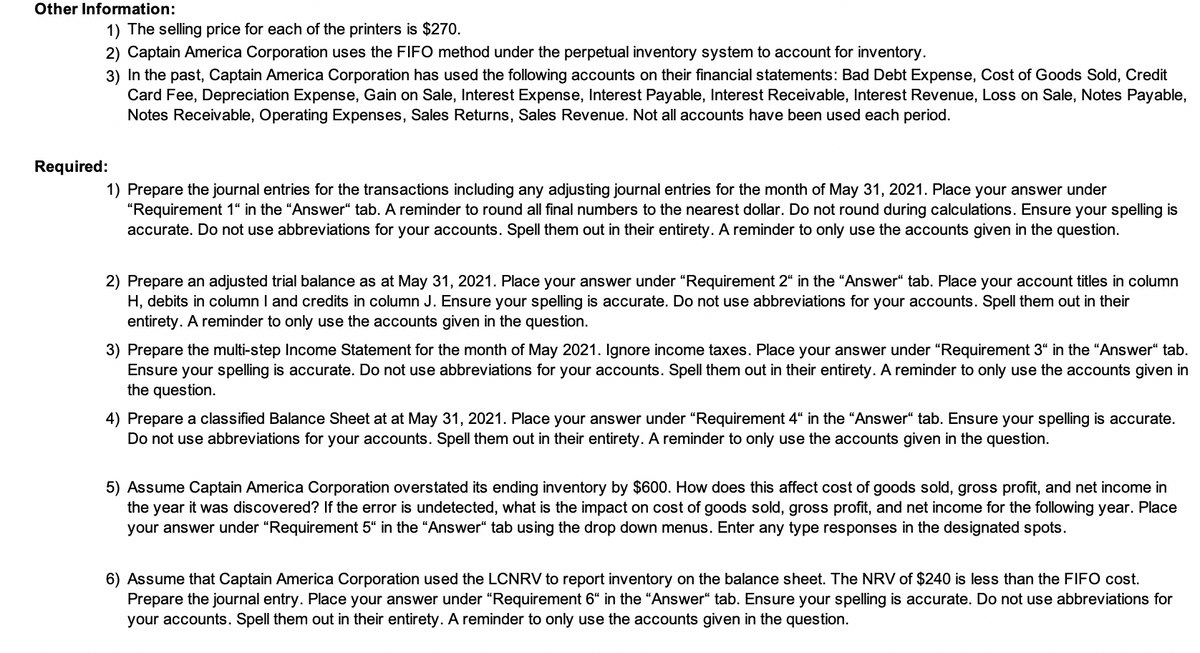

Transcribed Image Text:Other Information:

1) The selling price for each of the printers is $270.

2) Captain America Corporation uses the FIFO method under the perpetual inventory system to account for inventory.

3) In the past, Captain America Corporation has used the following accounts on their financial statements: Bad Debt Expense, Cost of Goods Sold, Credit

Card Fee, Depreciation Expense, Gain on Sale, Interest Expense, Interest Payable, Interest Receivable, Interest Revenue, Loss on Sale, Notes Payable,

Notes Receivable, Operating Expenses, Sales Returns, Sales Revenue. Not all accounts have been used each period.

Required:

1) Prepare the journal entries for the transactions including any adjusting journal entries for the month of May 31, 2021. Place your answer under

"Requirement 1“ in the "Answer“ tab. A reminder to round all final numbers to the nearest dollar. Do not round during calculations. Ensure your spelling is

accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question.

2) Prepare an adjusted trial balance as at May 31, 2021. Place your answer under "Requirement 2“ in the “Answer“ tab. Place your account titles in column

H, debits in column I and credits in column J. Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their

entirety. A reminder to only use the accounts given in the question.

3) Prepare the multi-step Income Statement for the month of May 2021. Ignore income taxes. Place your answer under “Requirement 3“ in the "Answer“ tab.

Ensure your spelling is accurate. Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in

the question.

4) Prepare a classified Balance Sheet at at May 31, 2021. Place your answer under "Requirement 4“ in the "Answer“ tab. Ensure your spelling is accurate.

Do not use abbreviations for your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question.

5) Assume Captain America Corporation overstated its ending inventory by $600. How does this affect cost of goods sold, gross profit, and net income in

the year it was discovered? If the error is undetected, what is the impact on cost of goods sold, gross profit, and net income for the following year. Place

your answer under “Requirement 5“ in the "Answer“ tab using the drop down menus. Enter any type responses in the designated spots.

6) Assume that Captain America Corporation used the LCNRV to report inventory on the balance sheet. The NRV of $240 is less than the FIFO cost.

Prepare the journal entry. Place your answer under "Requirement 6“ in the "Answer“ tab. Ensure your spelling is accurate. Do not use abbreviations for

your accounts. Spell them out in their entirety. A reminder to only use the accounts given in the question.

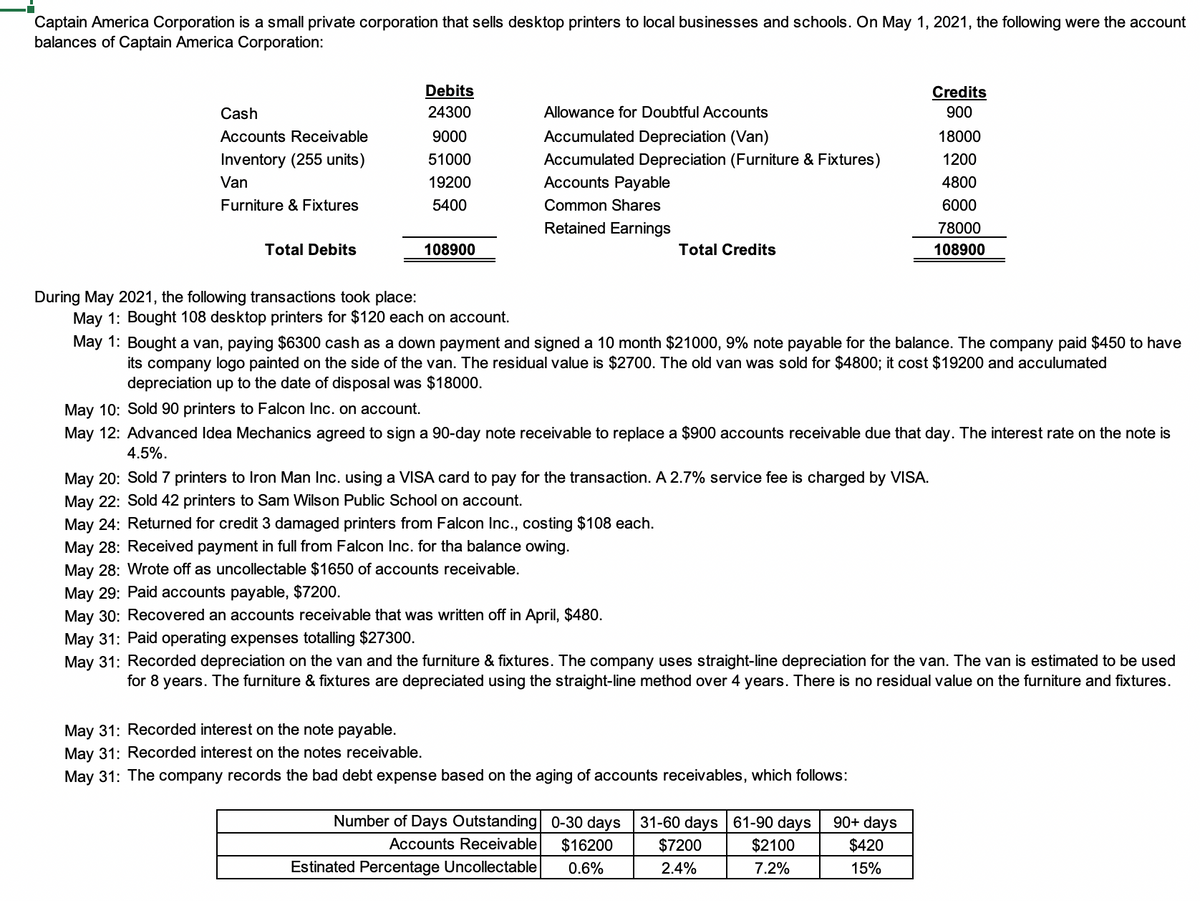

Transcribed Image Text:Captain America Corporation is a small private corporation that sells desktop printers to local businesses and schools. On May 1, 2021, the following were the account

balances of Captain America Corporation:

Debits

Credits

Cash

24300

Allowance for Doubtful Accounts

900

Accounts Receivable

9000

Accumulated Depreciation (Van)

18000

Inventory (255 units)

51000

Accumulated Depreciation (Furniture & Fixtures)

Accounts Payable

1200

Van

19200

4800

Furniture & Fixtures

5400

Common Shares

6000

Retained Earnings

78000

Total Debits

108900

Total Credits

108900

During May 2021, the following transactions took place:

May 1: Bought 108 desktop printers for $120 each on account.

May 1: Bought a van, paying $6300 cash as a down payment and signed a 10 month $21000, 9% note payable for the balance. The company paid $450 to have

its company logo painted on the side of the van. The residual value is $2700. The old van was sold for $4800; it cost $19200 and acculumated

depreciation up to the date of disposal was $18000.

May 10: Sold 90 printers to Falcon Inc. on account.

May 12: Advanced Idea Mechanics agreed to sign a 90-day note receivable to replace a $900 accounts receivable due that day. The interest rate on the note is

4.5%.

May 20: Sold 7 printers to Iron Man Inc. using a VISA card to pay for the transaction. A 2.7% service fee is charged by VISA.

May 22: Sold 42 printers to Sam Wilson Public School on account.

May 24: Returned for credit 3 damaged printers from Falcon Inc., costing $108 each.

May 28: Received payment in full from Falcon Inc. for tha balance owing.

May 28: Wrote off as uncollectable $1650 of accounts receivable.

May 29: Paid accounts payable, $7200.

May 30: Recovered an accounts receivable that was written off in April, $480.

May 31: Paid operating expenses totalling $27300.

May 31: Recorded depreciation on the van and the furniture & fixtures. The company uses straight-line depreciation for the van. The van is estimated to be used

for 8 years. The furniture & fixtures are depreciated using the straight-line method over 4 years. There is no residual value on the furniture and fixtures.

May 31: Recorded interest on the note payable.

May 31: Recorded interest on the notes receivable.

May 31: The company records the bad debt expense based on the aging of accounts receivables, which follows:

Number of Days Outstanding 0-30 days 31-60 days | 61-90 days

90+ days

Accounts Receivable

$16200

$7200

$2100

$420

Estinated Percentage Uncollectable

0.6%

2.4%

7.2%

15%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning