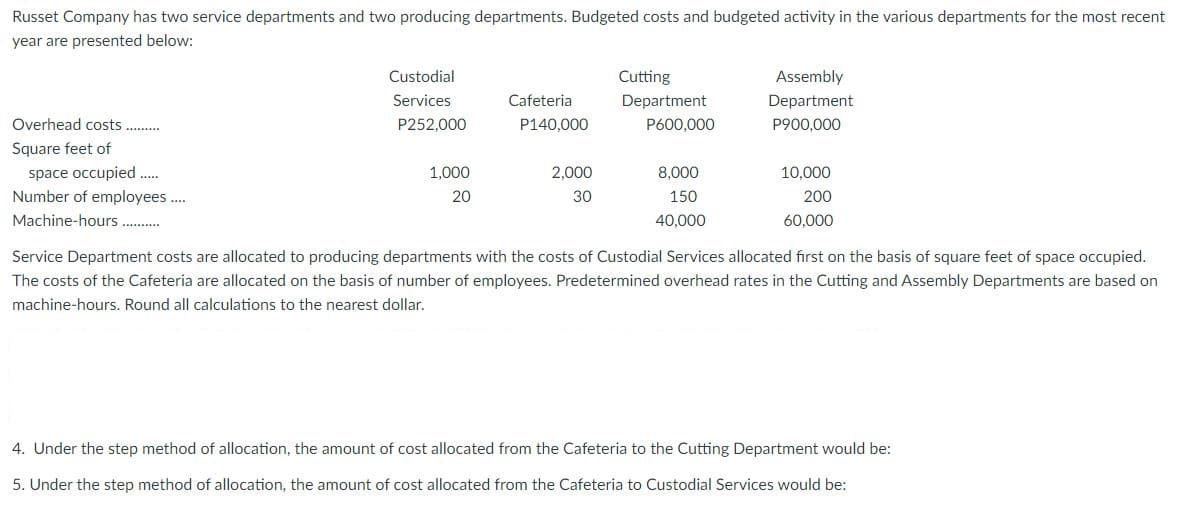

Russet Company has two service departments and two producing departments. Budgeted costs and budgeted activity in the various departments for the most recent year are presented below: Custodial Cutting Assembly Services Cafeteria Department Department Overhead costs P252,000 P140,000 P600,000 P900,000 .... Square feet of space occupied. Number of employees... 1,000 2,000 8,000 10,000 20 30 150 200 Machine-hours . 40,000 60,000 Service Department costs are allocated to producing departments with the costs of Custodial Services allocated first on the basis of square feet of space occupied. The costs of the Cafeteria are allocated on the basis of number of employees. Predetermined overhead rates in the Cutting and Assembly Departments are based on machine-hours. Round all calculations to the nearest dollar. 4. Under the step method of allocation, the amount of cost allocated from the Cafeteria to the Cutting Department would be: 5. Under the step method of allocation, the amount of cost allocated from the Cafeteria to Custodial Services would be:

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images