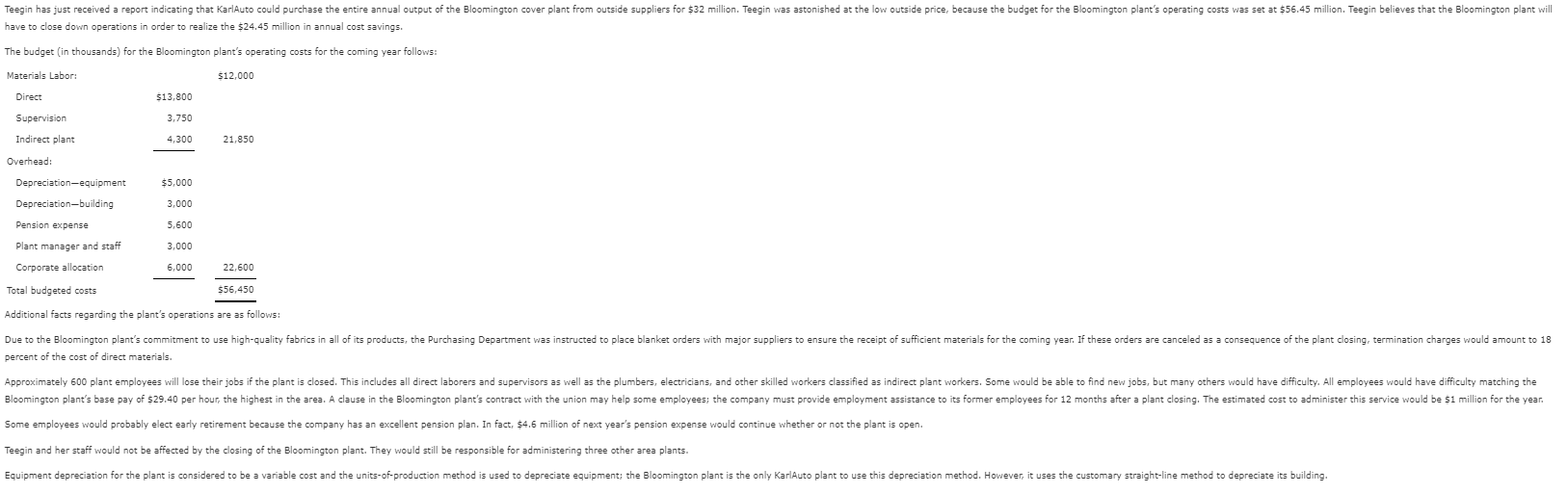

Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant's operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the $24.45 million in annual cosst savings. The budget (in thousands) for the Bloomington plant's operating costs for the coming year follows: Materials Labor: $12,000 Direct $13,800 Supervision 3,750 Indirect plant 21,850 4,300 Overhead: $5,000 Depreciation-equipment Depreciation-building 3,000 Pension expense 5,600 Plant manager and staff 3,000 Corporate allocation 6,000 22,600 Total budgeted costs $56,450 Additional facts regarding the plant's operations are as follows: Due to the Bloomington plant's commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials Approximately 600 plant employees will lose their jobs if the plant closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plant's base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant's contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year. Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year's pension expense would continue whether or not the plant is open. Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants. Equipment depreciation for the plant is considered to be a variable cost and the units-of-production method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building. Required: Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Enter all answers as positive amounts. If an amount box does not require an entry, enter "O" for your answer. Enter all amounts in thousands. For example,, $3 million would be entered as "3,000". KarlAuto Corporation Quantitative Analysis Plant Shutdown (Buy Covers) Continue Operations (Make Covers) Cost Item First vear (in thousands): Materials Labor Pension expense Cost of buying Total relevant costs Following years (in thousands): Materials Labor Pension expense Cost of buying Total recurring costs

Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant's operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the $24.45 million in annual cosst savings. The budget (in thousands) for the Bloomington plant's operating costs for the coming year follows: Materials Labor: $12,000 Direct $13,800 Supervision 3,750 Indirect plant 21,850 4,300 Overhead: $5,000 Depreciation-equipment Depreciation-building 3,000 Pension expense 5,600 Plant manager and staff 3,000 Corporate allocation 6,000 22,600 Total budgeted costs $56,450 Additional facts regarding the plant's operations are as follows: Due to the Bloomington plant's commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials Approximately 600 plant employees will lose their jobs if the plant closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plant's base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant's contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year. Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year's pension expense would continue whether or not the plant is open. Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants. Equipment depreciation for the plant is considered to be a variable cost and the units-of-production method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building. Required: Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Enter all answers as positive amounts. If an amount box does not require an entry, enter "O" for your answer. Enter all amounts in thousands. For example,, $3 million would be entered as "3,000". KarlAuto Corporation Quantitative Analysis Plant Shutdown (Buy Covers) Continue Operations (Make Covers) Cost Item First vear (in thousands): Materials Labor Pension expense Cost of buying Total relevant costs Following years (in thousands): Materials Labor Pension expense Cost of buying Total recurring costs

Chapter11: Cash Flow Estimation And Risk Analysis

Section: Chapter Questions

Problem 1dM

Related questions

Question

Transcribed Image Text:Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant's operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will

have to close down operations in order to realize the $24.45 million in annual cosst savings.

The budget (in thousands) for the Bloomington plant's operating costs for the coming year follows:

Materials Labor:

$12,000

Direct

$13,800

Supervision

3,750

Indirect plant

21,850

4,300

Overhead:

$5,000

Depreciation-equipment

Depreciation-building

3,000

Pension expense

5,600

Plant manager and staff

3,000

Corporate allocation

6,000

22,600

Total budgeted costs

$56,450

Additional facts regarding the plant's operations are as follows:

Due to the Bloomington plant's commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18

percent of the cost of direct materials

Approximately 600 plant employees will lose their jobs if the plant

closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the

Bloomington plant's base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant's contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year.

Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year's pension expense would continue whether or not the plant is open.

Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants.

Equipment depreciation for the plant is considered to be a variable cost and the units-of-production method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building.

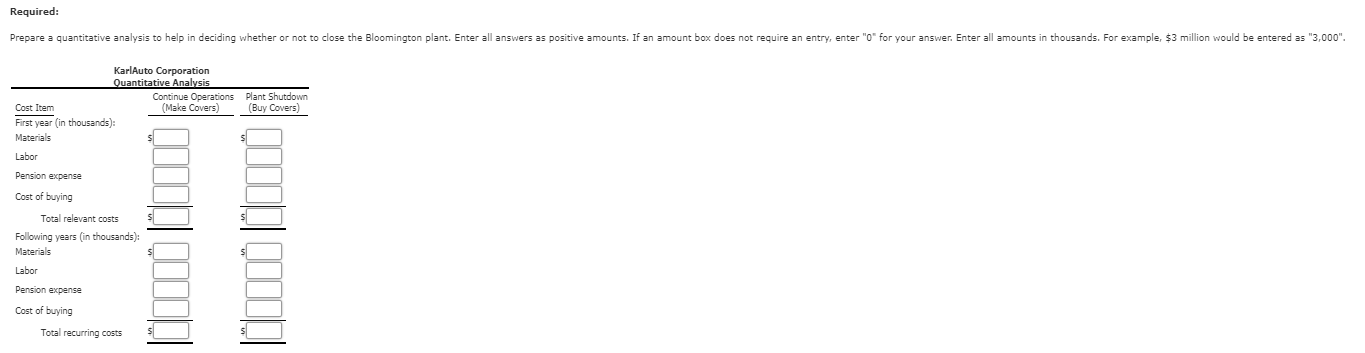

Transcribed Image Text:Required:

Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Enter all answers as positive amounts. If an amount box does not require an entry, enter "O" for your answer. Enter all amounts in thousands. For example,, $3 million would be entered as "3,000".

KarlAuto Corporation

Quantitative Analysis

Plant Shutdown

(Buy Covers)

Continue Operations

(Make Covers)

Cost Item

First vear (in thousands):

Materials

Labor

Pension expense

Cost of buying

Total relevant costs

Following years (in thousands):

Materials

Labor

Pension expense

Cost of buying

Total recurring costs

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Recommended textbooks for you

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning