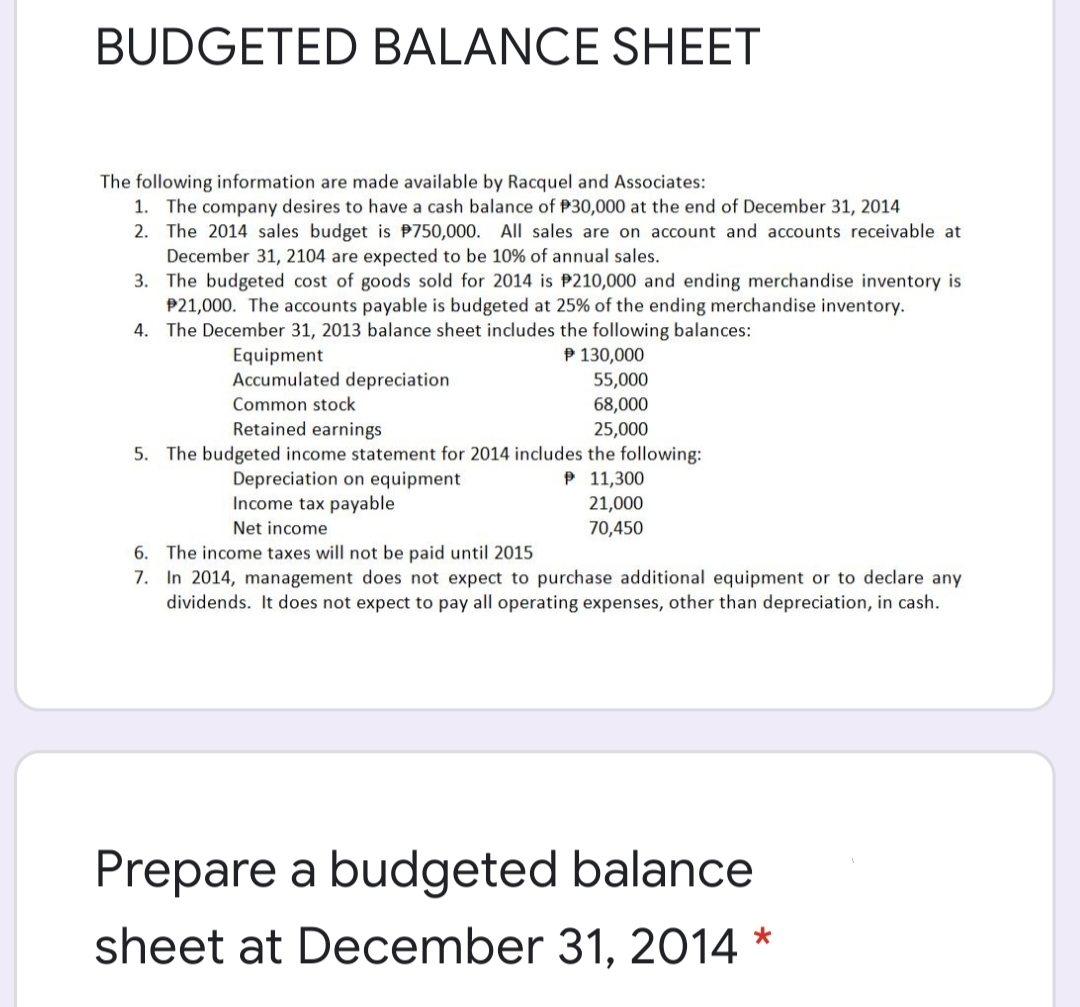

The following information are made available by Racquel and Associates: 1. The company desires to have a cash balance of P30,000 at the end of December 31, 2014 2. The 2014 sales budget is P750,000. All sales are on account and accounts receivable at December 31, 2104 are expected to be 10% of annual sales. 3. The budgeted cost of goods sold for 2014 is P210,000 and ending merchandise inventory is P21,000. The accounts payable is budgeted at 25% of the ending merchandise inventory. 4. The December 31, 2013 balance sheet includes the following balances: P 130,000 Equipment Accumulated depreciation Common stock 55,000 68,000 Retained earnings 25,000 5. The budgeted income statement for 2014 includes the following: P 11,300 Depreciation on equipment Income tax payable 21,000 Net income 70,450 6. The income taxes will not be paid until 2015 7. In 2014, management does not expect to purchase additional equipment or to declare any dividends. It does not expect to pay all operating expenses, other than depreciation, in cash. Prepare a budgeted balance sheet at December 31, 2014 *

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

Step by step

Solved in 2 steps with 2 images