This question: 1 point(s) possible The table shows the demand and supply schedules for boxes of chocolates on an average week. If the price of chocolates is $17.00 a box, what is the situation in the market? How is market equilibrium restored? Quantity Price Quantity demanded supplied (boxes per week) 1,600 (dollars per box) 13.00 1,200 The of chocolates is eliminated as the price of a box of chocolates 14.00 1,500 1,300 15.00 1,400 1,400 A. surplus; falls 16.00 1,300 1,500 17.00 1,200 1,100 1,600 OB. shortage; falls 18.00 1,700 O C. shortage; rises O D. surplus; first falls and then rises O E. surplus; rises As the market moves to its new equilibrium, the quantity supplied and the quantity demanded O A. increases; decreases O B. decreases; increases O C. decreases; decreases O D. decreases; does not change O E. increases; increases O Time Remaining: 01:01:03

This question: 1 point(s) possible The table shows the demand and supply schedules for boxes of chocolates on an average week. If the price of chocolates is $17.00 a box, what is the situation in the market? How is market equilibrium restored? Quantity Price Quantity demanded supplied (boxes per week) 1,600 (dollars per box) 13.00 1,200 The of chocolates is eliminated as the price of a box of chocolates 14.00 1,500 1,300 15.00 1,400 1,400 A. surplus; falls 16.00 1,300 1,500 17.00 1,200 1,100 1,600 OB. shortage; falls 18.00 1,700 O C. shortage; rises O D. surplus; first falls and then rises O E. surplus; rises As the market moves to its new equilibrium, the quantity supplied and the quantity demanded O A. increases; decreases O B. decreases; increases O C. decreases; decreases O D. decreases; does not change O E. increases; increases O Time Remaining: 01:01:03

Principles of Microeconomics (MindTap Course List)

8th Edition

ISBN:9781305971493

Author:N. Gregory Mankiw

Publisher:N. Gregory Mankiw

Chapter4: The Market Forces Of Supply And Demand

Section: Chapter Questions

Problem 6CQQ

Related questions

Question

Question 10 r

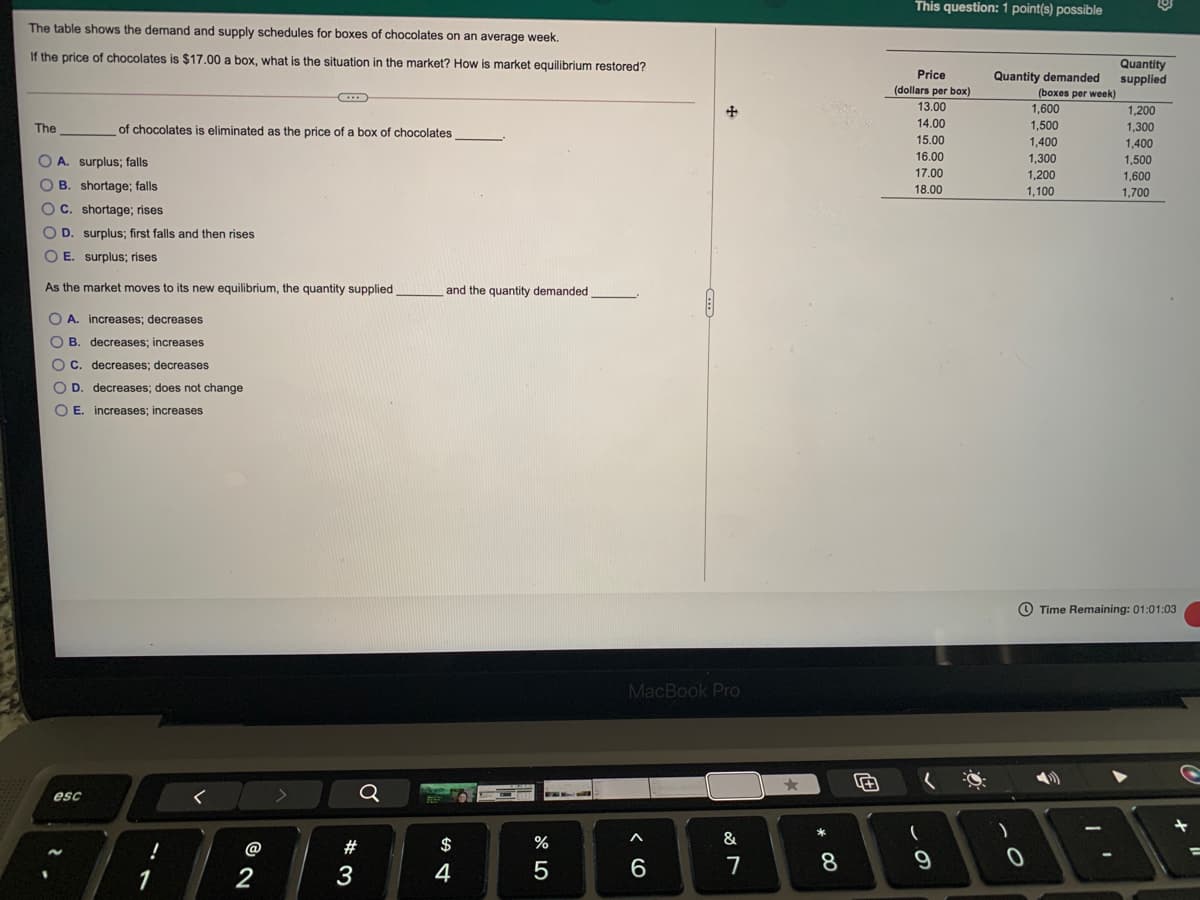

Transcribed Image Text:This question: 1 point(s) possible

The table shows the demand and supply schedules for boxes of chocolates on an average week.

If the price of chocolates is $17.00 a box, what is the situation in the market? How is market equilibrium restored?

Quantity

supplied

Price

Quantity demanded

(dollars per box)

(boxes per week)

13.00

1,600

1,200

The

of chocolates

eliminated as the price of a box of chocolates

14.00

1,500

1,300

15.00

1,400

1,400

OA. surplus; falls

16.00

1,300

1,500

17.00

1,200

1,600

O B. shortage; falls

18.00

1,100

1,700

O C. shortage; rises

O D. surplus; first falls and then rises

O E. surplus; rises

As the market moves to its new equilibrium, the quantity supplied

and the quantity demanded

O A. increases; decreases

O B. decreases; increases

O C. decreases; decreases

O D. decreases; does not change

O E.

increases; increases

O Time Remaining: 01:01:03

MacBook Pro

esc

$

&

@

7

8

1

3

4

O 0 0 0

Expert Solution

Step 1

Equilibrium refers to the situation where the quantity demanded by the consumers is equal to the quantity supplied by the producers. This mean that the consumers want to consume exactly the same amount of goods which the producers want to produce. The point where the supply and demand curves cross is known as the equilibrium point. The price at this point is called equilibrium price and the quantity exchanged is called equilibrium quantity.

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Microeconomics (MindTap Course List)

Economics

ISBN:

9781305971493

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou…

Economics

ISBN:

9781285165875

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Microeconomics (MindTap Course List)

Economics

ISBN:

9781305971493

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou…

Economics

ISBN:

9781285165875

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics (MindTap Course List)

Economics

ISBN:

9781305585126

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning