uld of Ajax Division of Soap Corporation produces soap, 20 percent of which are sold to Axion Division of Soap Corporation. The remainder is sold to outside customers. SoapP treats its divisions as profit centers and allows division managers to choose their sources of sale and the supply. Corporate policy requires that all interdivisional sales and purchases be recorded at variable cost as transfer price. Aiax Division's estimated sales and standard cost data for the year ending December 31, 2000, based on capacity of 100,000 units, are as follows: Axion Outsiders P8,000,000 (3,6000,00) (1,200,000) 320,0000 80,000 Sales P900,000 (P900,000) (300,000) (300,000) 20,000 Variable costs Fixed costs Gross margin Unit sales price of P75 per unit. Axion can purchase its requirements from an outside supplier at a price of P85 per unit. Required: Ajax has an opportunity to sell the 20,000 units shown above to an outside customer at a 1. Assuming that Ajax Division desires to maximize its gross margin, should Ajax take on the new customer and drop its sales to Axion in the current year? Why? 2. Assume, instead, that Soap Corporation permits division managers to negotiate the transfer price for the year. The managers agreed on a tentative transfer price of P75 per unit, to be reduced based on an equal sharing of the additional gross margin to Ajax resulting from the sale to Axion of 20,000 units at P75 per unit. What would be the actual transfer price for the year? 3. Assume now that Ajax Division has an opportunity to sell the 20,000 units that Axior Division would buy to the same customers that are buying the other 80,000 uni produced by Ajax. Ajax Division could sell all 100,000 units to outside customers a price of P100. What actions by each division manager are in the best interest Soap Corporation?

uld of Ajax Division of Soap Corporation produces soap, 20 percent of which are sold to Axion Division of Soap Corporation. The remainder is sold to outside customers. SoapP treats its divisions as profit centers and allows division managers to choose their sources of sale and the supply. Corporate policy requires that all interdivisional sales and purchases be recorded at variable cost as transfer price. Aiax Division's estimated sales and standard cost data for the year ending December 31, 2000, based on capacity of 100,000 units, are as follows: Axion Outsiders P8,000,000 (3,6000,00) (1,200,000) 320,0000 80,000 Sales P900,000 (P900,000) (300,000) (300,000) 20,000 Variable costs Fixed costs Gross margin Unit sales price of P75 per unit. Axion can purchase its requirements from an outside supplier at a price of P85 per unit. Required: Ajax has an opportunity to sell the 20,000 units shown above to an outside customer at a 1. Assuming that Ajax Division desires to maximize its gross margin, should Ajax take on the new customer and drop its sales to Axion in the current year? Why? 2. Assume, instead, that Soap Corporation permits division managers to negotiate the transfer price for the year. The managers agreed on a tentative transfer price of P75 per unit, to be reduced based on an equal sharing of the additional gross margin to Ajax resulting from the sale to Axion of 20,000 units at P75 per unit. What would be the actual transfer price for the year? 3. Assume now that Ajax Division has an opportunity to sell the 20,000 units that Axior Division would buy to the same customers that are buying the other 80,000 uni produced by Ajax. Ajax Division could sell all 100,000 units to outside customers a price of P100. What actions by each division manager are in the best interest Soap Corporation?

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter10: Decentralization: Responsibility Accounting, Performance Evaluation, And Transfer Pricing

Section: Chapter Questions

Problem 4CE

Related questions

Question

100%

Please Answer No. 2

Provide a complete solution. Thank You

Transcribed Image Text:brication

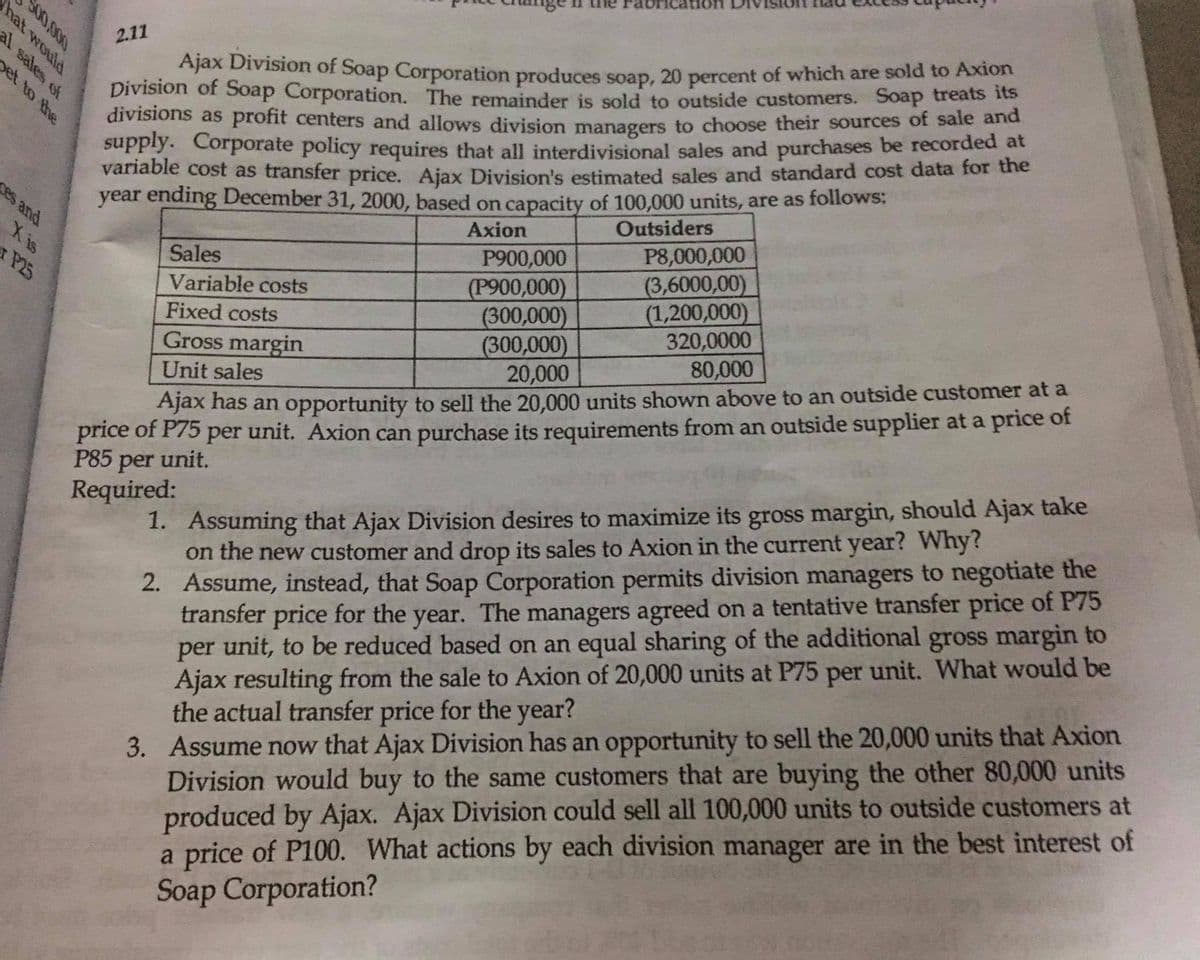

Ajax Division of Soap Corporation produces soap, 20 percent of which are sold to Axion

Division of Soap Corporation. The remainder is sold to outside customers. Soap treats its

divisions as profit centers and allows division managers to choose their sources of sale and

supply. Corporate policy requires that all interdivisional sales and purchases be recorded at

variable cost as transfer price. Ajax Division's estimated sales and standard cost data for the

year ending December 31, 2000, based on capacity of 100,000 units, are as follows:

2.11

pet to the

ses and

Outsiders

Axion

Xis

P8,000,000

Sales

P900,000

(3,6000,00)

(1,200,000)

320,0000

80,000

xP25

(P900,000)

(300,000)

(300,000)

20,000

Variable costs

Fixed costs

Gross margin

Unit sales

price of P75 per unit. Axion can purchase its requirements from an outside supplier at a price of

P85 unit.

Ajax nas an opportunity to sell the 20,000 units shown above to an outside customer at a

1. Assuming that Ajax Division desires to maximize its gross margin, should Ajax take

on the new customer and drop its sales to Axion in the current year? Why?

2. Assume, instead, that Soap Corporation permits division managers to negotiate the

transfer price for the year. The managers agreed on a tentative transfer price of P75

per unit, to be reduced based on an equal sharing of the additional gross margin to

Ajax resulting from the sale to Axion of 20,000 units at P75 per unit. What would be

the actual transfer price for the year?

3. Assume now that Ajax Division has an opportunity to sell the 20,000 units that Axion

Division would buy to the same customers that are buying the other 80,000 units

produced by Ajax. Ajax Division could sell all 100,000 units to outside customers at

a price of P100. What actions by each division manager are in the best interest of

Soap Corporation?

per

Required:

S00,000

hat would

al sales of

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College