Vaughn treats its divisions as profit centers and allows division managers to choose whether to sell or to buy from internal division. Corporate policy requires that all interdivisional sales and purchases be transferred at variable cost. Gamma Division of Vaughn Corp. produces electric motors. This product is currently sold to outside customers but is needed by Omega, another division of Vaughn. Gamma Division's estimated sales and standard cost data for the year ended December 31, based on practical capacity of 60,000 units are as follows: P 7,200,000 3, 300,000 P 3,900,000 1,075,000 P 2,825,000 Sales Less: Variables Cost Contribution Margin Fixed Cost Operating Income Gamma has an opportunity to sell 12,000 units to Omega. Omega can purchase the units it needs from outside supplier for P92 each. Required: Assuming that Gamma can normally sell 57,000 units to outsider customers 1. compute for the minimum transfer price acceptable to Gamma. 2. Compute for the maximum transfer price.

Vaughn treats its divisions as profit centers and allows division managers to choose whether to sell or to buy from internal division. Corporate policy requires that all interdivisional sales and purchases be transferred at variable cost. Gamma Division of Vaughn Corp. produces electric motors. This product is currently sold to outside customers but is needed by Omega, another division of Vaughn. Gamma Division's estimated sales and standard cost data for the year ended December 31, based on practical capacity of 60,000 units are as follows: P 7,200,000 3, 300,000 P 3,900,000 1,075,000 P 2,825,000 Sales Less: Variables Cost Contribution Margin Fixed Cost Operating Income Gamma has an opportunity to sell 12,000 units to Omega. Omega can purchase the units it needs from outside supplier for P92 each. Required: Assuming that Gamma can normally sell 57,000 units to outsider customers 1. compute for the minimum transfer price acceptable to Gamma. 2. Compute for the maximum transfer price.

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter10: Evaluating Decentralized Operations

Section: Chapter Questions

Problem 6PA

Related questions

Question

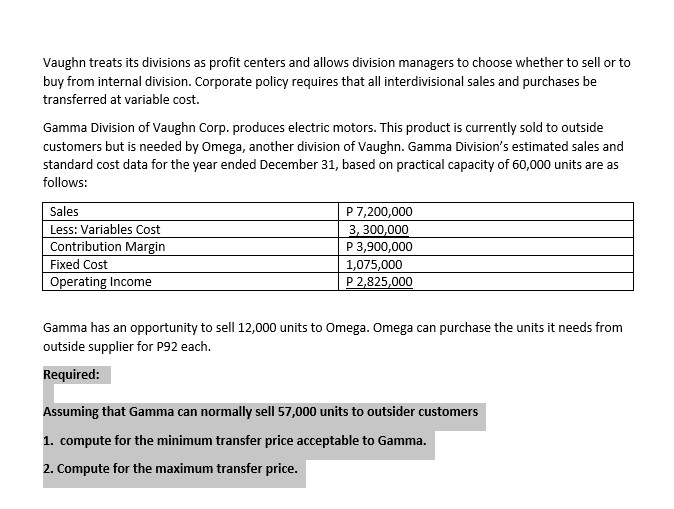

Transcribed Image Text:Vaughn treats its divisions as profit centers and allows division managers to choose whether to sell or to

buy from internal division. Corporate policy requires that all interdivisional sales and purchases be

transferred at variable cost.

Gamma Division of Vaughn Corp. produces electric motors. This product is currently sold to outside

customers but is needed by Omega, another division of Vaughn. Gamma Division's estimated sales and

standard cost data for the year ended December 31, based on practical capacity of 60,000 units are as

follows:

P 7,200,000

3, 300,000

P 3,900,000

1,075,000

P 2,825,000

Sales

Less: Variables Cost

Contribution Margin

Fixed Cost

Operating Income

Gamma has an opportunity to sell 12,000 units to Omega. Omega can purchase the units it needs from

outside supplier for P92 each.

Required:

Assuming that Gamma can normally sell 57,000 units to outsider customers

1. compute for the minimum transfer price acceptable to Gamma.

2. Compute for the maximum transfer price.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College