Videos

Withdrawal of a Partner under Various Alternatives

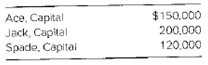

The

The partners allocate partnership income and loss in the ratio 20:30:50, respectively.

Required

Record Spade’s withdrawal under each of the following independent situations.

- Jack acquired Spade’s capital interest for $150,000 in a personal transaction. Partnership assets were not revalued, and partnership

goodwill was not recognized. - Assume the same facts as in part a except that partnership goodwill applicable to the entire business was recognized by the partnership.

- Spade received $180,000 of partnership cash upon retirement. Capital of the partnership after Spade’s retirement was $290,000.

- Spade received $60,000 of cash and partnership land with a fair value of $120,000. The carrying amount of the land on the partnership books was $100,000. Capital of the partnership after Spade’s retirement was $310,000.

- Spade received $150,000 of partnership cash upon retirement. The partnership recorded the portion of goodwill attributable to Spade.

- Assume the same facts as in part e except that partnership goodwill attributable to all partners was recorded.

- Because of limited cash n the partnership, Spade received land with a fair value of $100,000 and a partnership note payable for $50,000. The land’s carrying amount on the partnership books was $60,000. Capital of the partnership after Spade’s retirement was $360,000.

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 1

The entry when J acquired S capital interest for $150,000 no assets were revalued.

Answer to Problem 15.15P

| Debit | Credit | |

| S Capital Account | 120,000 | |

| J Capital Account | 120,000 |

Explanation of Solution

J acquired S interest in a personal transaction as no assets were revalued the excess amount is treated as personal transaction, hence will not be recognized. Only the S capital balance will be transferred to J.

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 2

The entry when J acquired S capital interest for $150,000 no assets were revalued but goodwill is recogized.

Answer to Problem 15.15P

| Debit | Credit | |

| Goodwill | 60,000 | |

| A’s capital | 12,000 | |

| J’s capital | 18,000 | |

| S’s capital | 30,000 | |

| S capital | 150,000 | |

| J capital | 150,000 |

Explanation of Solution

Valuation of goodwill:

| Amount $ | |

| Amount Paid by J for S capital | 150,000 |

| Less: S capital interest | (120,000) |

| Goodwill attributed to S | 30,000 |

Implied value of goodwill:

As S share of profit and loss is 50%

Implied value of total goodwill will be $30,000 / .50 =

$60,000

A’s share of goodwill $60,000 x .20 =

$12,000

J’s share of goodwill $60,000 x .30 =

$18,000

S capital will be debited with $150,000($120,000 + 30,000).

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 3

The entry when S received $180,000 upon retirement. Capital of partnership after S retirement is 290,000.

Answer to Problem 15.15P

| Debit | Credit | |

| S capital | 180,000 | |

| A’s capital | 24,000 | |

| J’s capital | 36,000 | |

| Cash | 180,000 |

Explanation of Solution

Calculation of bonus paid to S

| Amount $ | |

| Amount paid to S, on retirement | 180,000 |

| Less: S capital interest | (120,000) |

| Bonus paid − to be allocated to A and J in 40:60 ratio | 60,000 |

Allocation of bonus:

60,000 x .40

= 24,000

60,000 x .60

= 36,000

Capital balance after retirement

| Amount $ | |

| A’s capital account ($150,000 − 24,000) | 126,000 |

| J’s capital account ($150,000 - $36,000) | 164,000 |

| Total capital | 290,000 |

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 4

The entry when S received $60,000 of cash and partnership land with fair value of $120,000. The carrying amount of land is $100,000. Capital after S retirement was $310,000

Answer to Problem 15.15P

| Debit | Credit | |

| Land revaluation entry | ||

| Land | 20,000 | |

| A capital ($20,000 x .20) | 4,000 | |

| J’s capital ($20,000 x .30) | 6,000 | |

| S’s capital ($20,000 x .50) | 10,000 | |

| S capital | 130,000 | |

| A capital | 20,000 | |

| J capital | 30,000 | |

| Cash | 60,000 | |

| Land | 120,000 |

Explanation of Solution

Calculation of bonus to S

| A | J | S | |

| Profit ratio | 20% | `30% | 50% |

| Capital balance before S retirement | $150,000 | 200,000 | 120,000 |

| Gain recognized on transfer of land | 4,000 | 6,000 | 10,000 |

| Capital balance | 154,000 | 206,000 | 130,000 |

| S | |

| Amount paid to S 60,000 + 120,000 | 180,000 |

| S capital interest after revaluation of land | (130,000) |

| Bonus | 50,000 |

A’s share of bonus to S $20,000 ($50,000 x .40)

J’s share of bonus to S $30,000 ($50,000 x.60)

Balance of capital after retirement:

| S | |

| A’s capital ($154,000 - $20,000) | 134,000 |

| J’s capital ($206,000 - $30,000) | 176,000 |

| Total capital | 310,000 |

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 5

The entry when S received $150,000 cash and partnership recorded portion of goodwill attributable to S

Answer to Problem 15.15P

| Debit | Credit | |

| S capital | 120,000 | |

| Goodwill | 30,000 | |

| Cash | 150,000 |

Explanation of Solution

Valuation of goodwill:

| Amount $ | |

| Amount Paid to S | 150,000 |

| Less: S capital interest | (120,000) |

| Goodwill attributed to S | 30,000 |

Amount of goodwill debited to S capital and cash paid to S credited

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 6

The entry when S was given $150,000 goodwill applicable to entire business was recorded.

Answer to Problem 15.15P

| Debit | Credit | |

| Goodwill | 60,000 | |

| A’s capital | 12,000 | |

| J’s capital | 18,000 | |

| S’s capital | 30,000 | |

| S capital | 150,000 | |

| J capital | 150,000 |

Explanation of Solution

Valuation of goodwill:

| Amount $ | |

| Amount Paid by J for S capital | 150,000 |

| Less: S capital interest | (120,000) |

| Goodwill attributed to S | 30,000 |

Implied value of goodwill:

As S share of profit and loss is 50%

Implied value of total goodwill will be $30,000 / .50 =

$60,000

A’s share of goodwill $60,000 x .20 =

$12,000

J’s share of goodwill $60,000 x .30 =

$18,000

S capital will be debited with $150,000($120,000 + 30,000).

Disassociation of a partner: when a partner withdraws or retire from a partnership, that partner is disassociated from the partnership. In most cases the partnership purchases the disassociated partner’s interest in the partnership for a buyout price. Section 701 of UPA 1997 states that the buyout price is the estimated amount if, the partnership assets were sold at a price equal to the higher of the liquidation value or the value based on a sale of entire business as a going concern without the disassociated partner and the partnership was wound up and all partnership obligations settled. The partnership must pay interest to the disassociated partner from the date of disassociation to date of payment.

Requirement 7

The entry when S received land at fair value of $100,000 and notes payable of $50,000. Carrying amount of land was $60,000. Capital after S retirement was $360,000

Answer to Problem 15.15P

| Debit | Credit | |

| Land | 40,000 | |

| A’s capital ($40,000 x .20) | 8,000 | |

| J’s capital ($40,000 x .30) | 12,000 | |

| S’s capital ($40,000 x .50) | 20,000 | |

| S capital | 140,000 | |

| A capital ($10,000 x .40) | 4,000 | |

| J capital ($10,000 x 60) | 6,000 | |

| Land | 100,000 | |

| Notes payable | 50,000 |

Explanation of Solution

Calculation of bonus paid to S

| A | J | S | |

| Profit ratio | 20% | `30% | 50% |

| Capital balance before S retirement | 150,000 | 200,000 | 120,000 |

| Allocation of gain on transfer of land | 8,000 | 12,000 | 20,000 |

| Capital balance | 158,000 | 212,000 | 140,000 |

Bonus paid to S $10,000 (150,000 − 140,000)

Capital balance after S retirement

| Amount $ | |

| A’s capital ($158,000 − 4,000) | 154,000 |

| J’s capital (212,000 − 6,000) | 206,000 |

| Total capital | 360,000 |

Want to see more full solutions like this?

Chapter 15 Solutions

Advanced Financial Accounting

- ENTRIES FOR DISSOLUTION OF PARTNERSHIP Cummings and Stickel Construction Company, a partnership, is operating a general contracting business. Ownership of the company is divided among the partners, Katie Cummings, Julie Stickel, Roy Hewson, and Patricia Weber. Profits and losses are shared equally. The books are kept on the calendar-year basis. On August 10, after the business had been in operation for several years, Patricia Weber passed away. Mr. Weber wished to sell his wifes interest for 30,000. After the books were closed, the partners capital accounts had credit balances as follows: REQUIRED 1. Prepare the general journal entry required to enter the check issued to Mr. Weber in payment of his deceased wifes interest in the partnership. According to the partnership agreement, the difference between the amount paid to Mr. Weber and the book value of Patricia Webers capital account is allocated to the remaining partners based on their ending capital account balances. 2. Assume instead that Mr. Weber is paid 60,000 for the book value of Patricia Webers capital account. Prepare the necessary journal entry. 3. Assume instead that Julie Stickel (with the consent of the remaining partners) purchased Webers interest for 70,000 and gave Mr. Weber a personal check for that amount. Prepare the general journal entry for the partnership only.arrow_forwardThe partnership of Magda and Sue shares profits and losses in a 50:50 ratio after Mary receives a $7,000 salary and Sue receives a $6,500 salary. Prepare a schedule showing how the profit and loss should be divided, assuming the profit or loss for the year is: A. $10,000 B. $5,000 C. ($12,000) In addition, show the resulting entries to each partners capital account.arrow_forwardSTATEMENT OF PARTNER SHIP LIQUIDATION WITH LOSS After several years of operations, the partnership of Nelson, Pope, and Williams is to be liquidated. After making closing entries on March 31, 20--, the following accounts remain open: REQUIRED 1. Prepare a statement of partnership liquidation for the period July 120, 20--, showing the following: (a) The sale of noncash assets on July 1 (b) The allocation of any gain or loss to the partners on July 1 (c) The payment of the liabilities on July 15 (d) The distribution of cash to the partners on July 20 2. Journalize these four transactions in a general journal.arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage