3. The day prior to the release of yearly profits, a stock has price equal to 1. An investor is deciding whether to buy the stock or not. The investor has a wealth equal to 10. Yearly profits can be high with probability 0.4 or low with probability 0.6. If profits are high, the price will double on the following day; if profits are low, the price will halve on the following day. If the investor does not buy the stock, her wealth remains unchanged. If the inverstors buys the stock, she will sell the stock on the following day (regardless of whether the profits are high or low) and she will accrue the relative profit or loss. In other words, she cannot hold the stock for more than one day. The investor does not discount the future and she abides von-Neumann and Morgenstern axioms. Her vNM utility index over money is u (1) = x with BE (0, 2). • Write down the two possible gambles faced by the investor. • Does the investor buy the stock or not? Explain. • Compute the Arrow-Pratt measure of risk aversion. How does it relate to your previous reply?

3. The day prior to the release of yearly profits, a stock has price equal to 1. An investor is deciding whether to buy the stock or not. The investor has a wealth equal to 10. Yearly profits can be high with probability 0.4 or low with probability 0.6. If profits are high, the price will double on the following day; if profits are low, the price will halve on the following day. If the investor does not buy the stock, her wealth remains unchanged. If the inverstors buys the stock, she will sell the stock on the following day (regardless of whether the profits are high or low) and she will accrue the relative profit or loss. In other words, she cannot hold the stock for more than one day. The investor does not discount the future and she abides von-Neumann and Morgenstern axioms. Her vNM utility index over money is u (1) = x with BE (0, 2). • Write down the two possible gambles faced by the investor. • Does the investor buy the stock or not? Explain. • Compute the Arrow-Pratt measure of risk aversion. How does it relate to your previous reply?

Chapter7: Uncertainty

Section: Chapter Questions

Problem 7.7P

Related questions

Question

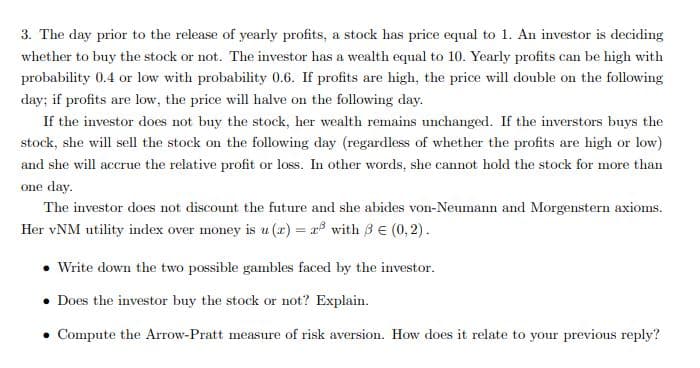

Transcribed Image Text:3. The day prior to the release of yearly profits, a stock has price equal to 1. An investor is deciding

whether to buy the stock or not. The investor has a wealth equal to 10. Yearly profits can be high with

probability 0.4 or low with probability 0.6. If profits are high, the price will double on the following

day; if profits are low, the price will halve on the following day.

If the investor does not buy the stock, her wealth remains unchanged. If the inverstors buys the

stock, she will sell the stock on the following day (regardless of whether the profits are high or low)

and she will accrue the relative profit or loss. In other words, she cannot hold the stock for more than

one day.

The investor does not discount the future and she abides von-Neumann and Morgenstern axioms.

Her vNM utility index over money is u (x) = r with 3 E (0,2).

• Write down the two possible gambles faced by the investor.

• Does the investor buy the stock or not? Explain.

• Compute the Arrow-Pratt measure of risk aversion. How does it relate to your previous reply?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Recommended textbooks for you

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning