3. The following costs were accrued for employee services: direct labor, $75,000; indirect labor, $110,000; sales commissions, $90,000; and administrative salaries, $180,000. 4. Sales travel costs were $19,000. 5. Utility costs in the factory were $38,000. 6. Advertising costs were $90,000. 7. Depreciation was recorded for the year, $350,000 (80% relates to factory operations, and 20% relates to selling and administrative activities). 8. Insurance expired during the year, $10,000 (90% relates to factory operations, and the remaining10% relates to selling and administrative activities). 9. Manufacturing overhead was applied to production. Due to greater than expected demand for its products, the company worked 80,000 machine-hours on all jobs during the year. 10. Goods costing $900,000 to manufacture according to their job cost sheets were completed during the year. 11. Goods were sold on account to customers during the year for a total of $1,500,000. The goods cost $870,000 to manufacture according to their job cost sheets. Required: 1. Prepare journal entries to record the transactions. 2. Is Manufacturing Overhead underapplied or overapplied for the year? Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold. Do not allocate the balance between ending inventories and Cost of Goods Sold.

3. The following costs were accrued for employee services: direct labor, $75,000; indirect labor, $110,000; sales commissions, $90,000; and administrative salaries, $180,000. 4. Sales travel costs were $19,000. 5. Utility costs in the factory were $38,000. 6. Advertising costs were $90,000. 7. Depreciation was recorded for the year, $350,000 (80% relates to factory operations, and 20% relates to selling and administrative activities). 8. Insurance expired during the year, $10,000 (90% relates to factory operations, and the remaining10% relates to selling and administrative activities). 9. Manufacturing overhead was applied to production. Due to greater than expected demand for its products, the company worked 80,000 machine-hours on all jobs during the year. 10. Goods costing $900,000 to manufacture according to their job cost sheets were completed during the year. 11. Goods were sold on account to customers during the year for a total of $1,500,000. The goods cost $870,000 to manufacture according to their job cost sheets. Required: 1. Prepare journal entries to record the transactions. 2. Is Manufacturing Overhead underapplied or overapplied for the year? Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold. Do not allocate the balance between ending inventories and Cost of Goods Sold.

Principles of Cost Accounting

17th Edition

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Edward J. Vanderbeck, Maria R. Mitchell

Chapter1: Introduction To Cost Accounting

Section: Chapter Questions

Problem 13E: Cycle Specialists manufactures goods on a job order basis. During the month of June, three jobs were...

Related questions

Question

100%

Hi

Attachment my question

Thank you so much

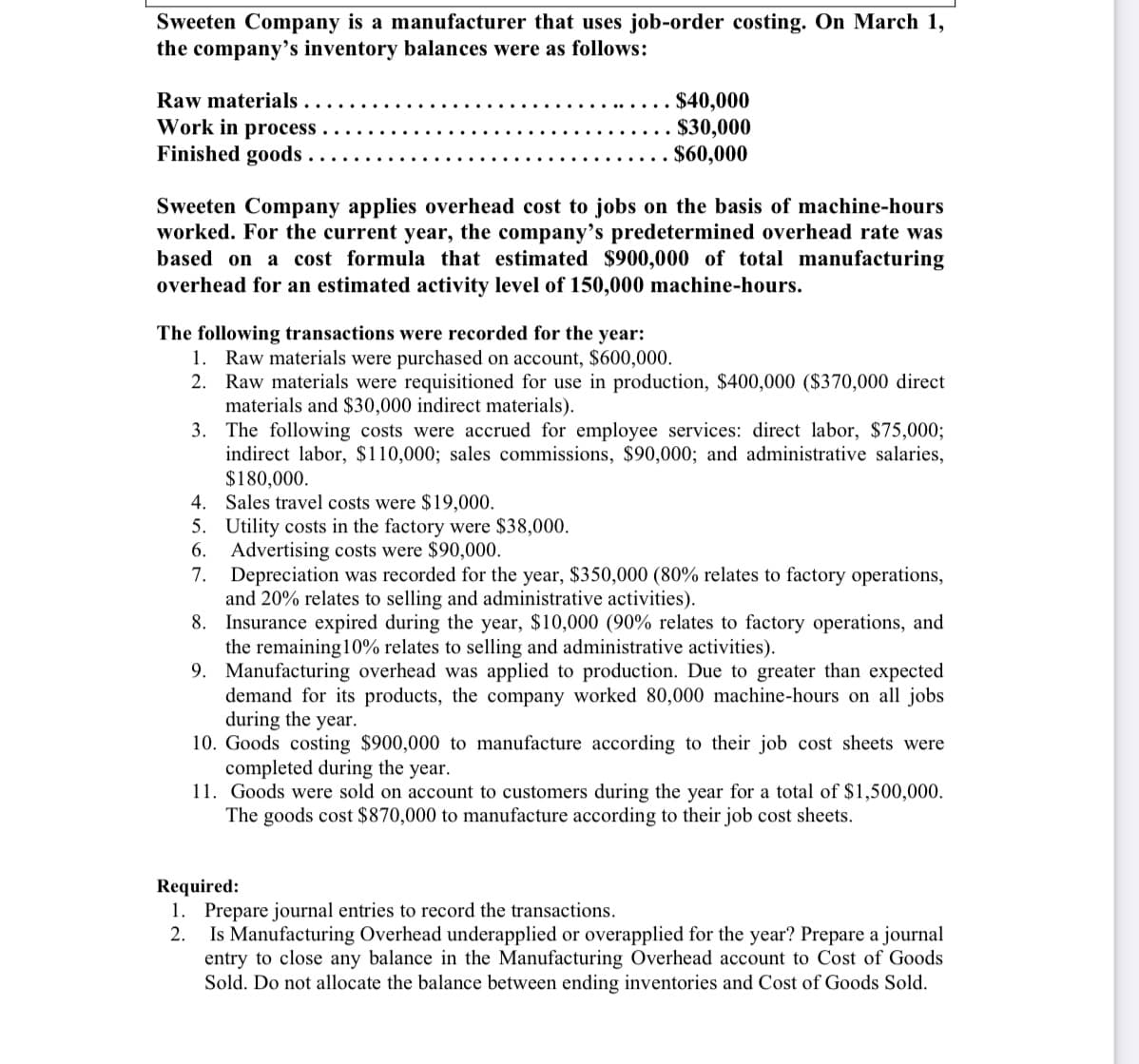

Transcribed Image Text:Sweeten Company is a manufacturer that uses job-order costing. On March 1,

the company's inventory balances were as follows:

Raw materials

Work in process . .

Finished goods

$40,000

$30,000

$60,000

Sweeten Company applies overhead cost to jobs on the basis of machine-hours

worked. For the current year, the company's predetermined overhead rate was

based on a cost formula that estimated $900,000 of total manufacturing

overhead for an estimated activity level of 150,000 machine-hours.

The following transactions were recorded for the year:

1. Raw materials were purchased on account, $600,000.

2. Raw materials were requisitioned for use in production, $400,000 ($370,000 direct

materials and $30,000 indirect materials).

3. The following costs were accrued for employee services: direct labor, $75,000;

indirect labor, $110,000; sales commissions, $90,000; and administrative salaries,

$180,000.

4. Sales travel costs were $19,000.

5. Utility costs in the factory were $38,000.

6. Advertising costs were $90,000.

7. Depreciation was recorded for the year, $350,000 (80% relates to factory operations,

and 20% relates to selling and administrative activities).

8. Insurance expired during the year, $10,000 (90% relates to factory operations, and

the remaining10% relates to selling and administrative activities).

9. Manufacturing overhead was applied to production. Due to greater than expected

demand for its products, the company worked 80,000 machine-hours on all jobs

during the year.

10. Goods costing $900,000 to manufacture according to their job cost sheets were

completed during the year.

11. Goods were sold on account to customers during the year for a total of $1,500,000.

The goods cost $870,000 to manufacture according to their job cost sheets.

Required:

1. Prepare journal entries to record the transactions.

2.

Is Manufacturing Overhead underapplied or overapplied for the year? Prepare a journal

entry to close any balance in the Manufacturing Overhead account to Cost of Goods

Sold. Do not allocate the balance between ending inventories and Cost of Goods Sold.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College