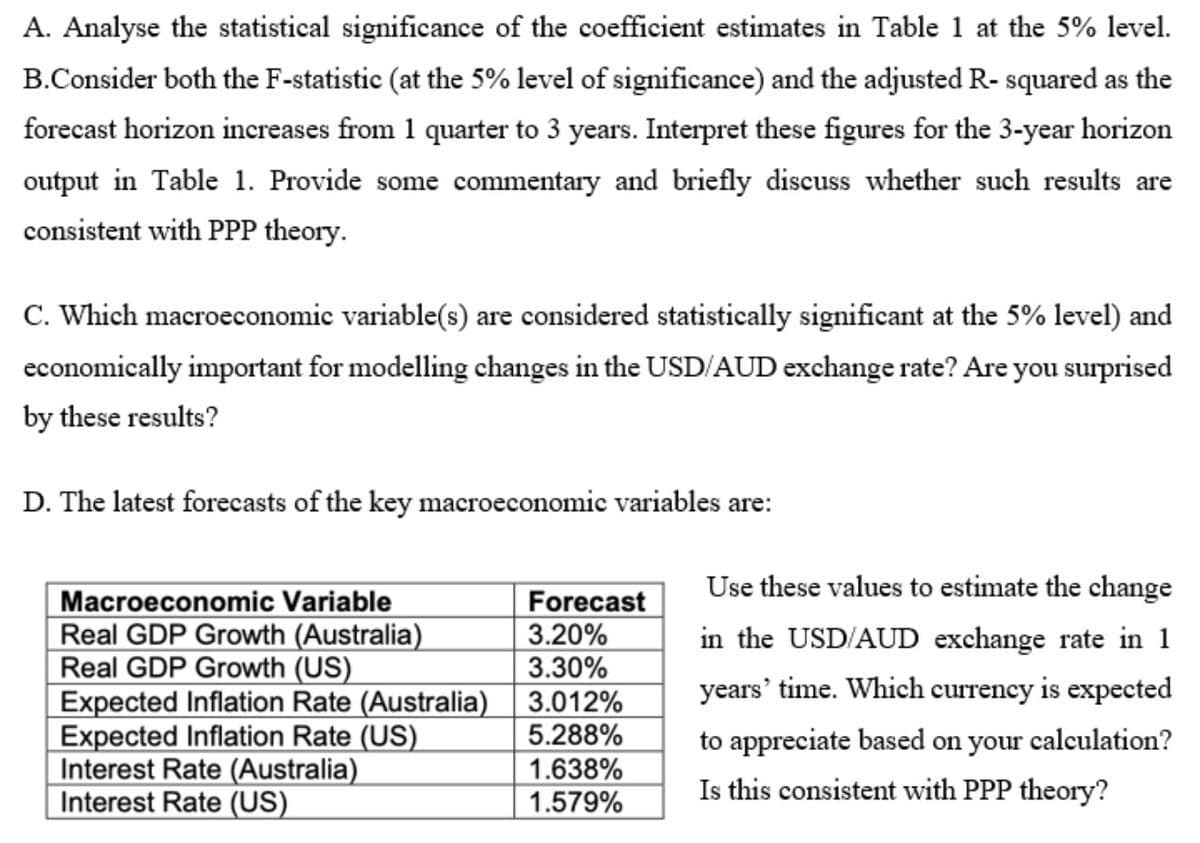

A. Analyse the statistical significance of the coefficient estimates in Table 1 at the 5% lev B.Consider both the F-statistic (at the 5% level of significance) and the adjusted R- squared as t forecast horizon increases from 1 quarter to 3 years. Interpret these figures for the 3-year horiz output in Table 1. Provide some commentary and briefly discuss whether such results a consistent with PPP theory.

A. Analyse the statistical significance of the coefficient estimates in Table 1 at the 5% lev B.Consider both the F-statistic (at the 5% level of significance) and the adjusted R- squared as t forecast horizon increases from 1 quarter to 3 years. Interpret these figures for the 3-year horiz output in Table 1. Provide some commentary and briefly discuss whether such results a consistent with PPP theory.

Linear Algebra: A Modern Introduction

4th Edition

ISBN:9781285463247

Author:David Poole

Publisher:David Poole

Chapter2: Systems Of Linear Equations

Section2.4: Applications

Problem 23EQ:

23. Consider a simple economy with just two industries: farming and manufacturing. Farming consumes...

Related questions

Question

100%

Please solve With the all subparts with the step and explaining solution. Please no reject thank u

Transcribed Image Text:A. Analyse the statistical significance of the coefficient estimates in Table 1 at the 5% level.

B.Consider both the F-statistic (at the 5% level of significance) and the adjusted R- squared as the

forecast horizon increases from 1 quarter to 3 years. Interpret these figures for the 3-year horizon

output in Table 1. Provide some commentary and briefly discuss whether such results are

consistent with PPP theory.

C. Which macroeconomic variable(s) are considered statistically significant at the 5% level) and

economically important for modelling changes in the USD/AUD exchange rate? Are you surprised

by these results?

D. The latest forecasts of the key macroeconomic variables are:

Use these values to estimate the change

Macroeconomic Variable

Real GDP Growth (Australia)

Real GDP Growth (US)

Expected Inflation Rate (Australia)

Expected Inflation Rate (US)

Interest Rate (Australia)

Interest Rate (US)

Forecast

3.20%

3.30%

in the USD/AUD exchange rate in 1

years' time. Which currency is expected

3.012%

5.288%

to appreciate based on your calculation?

1.638%

1.579%

Is this consistent with PPP theory?

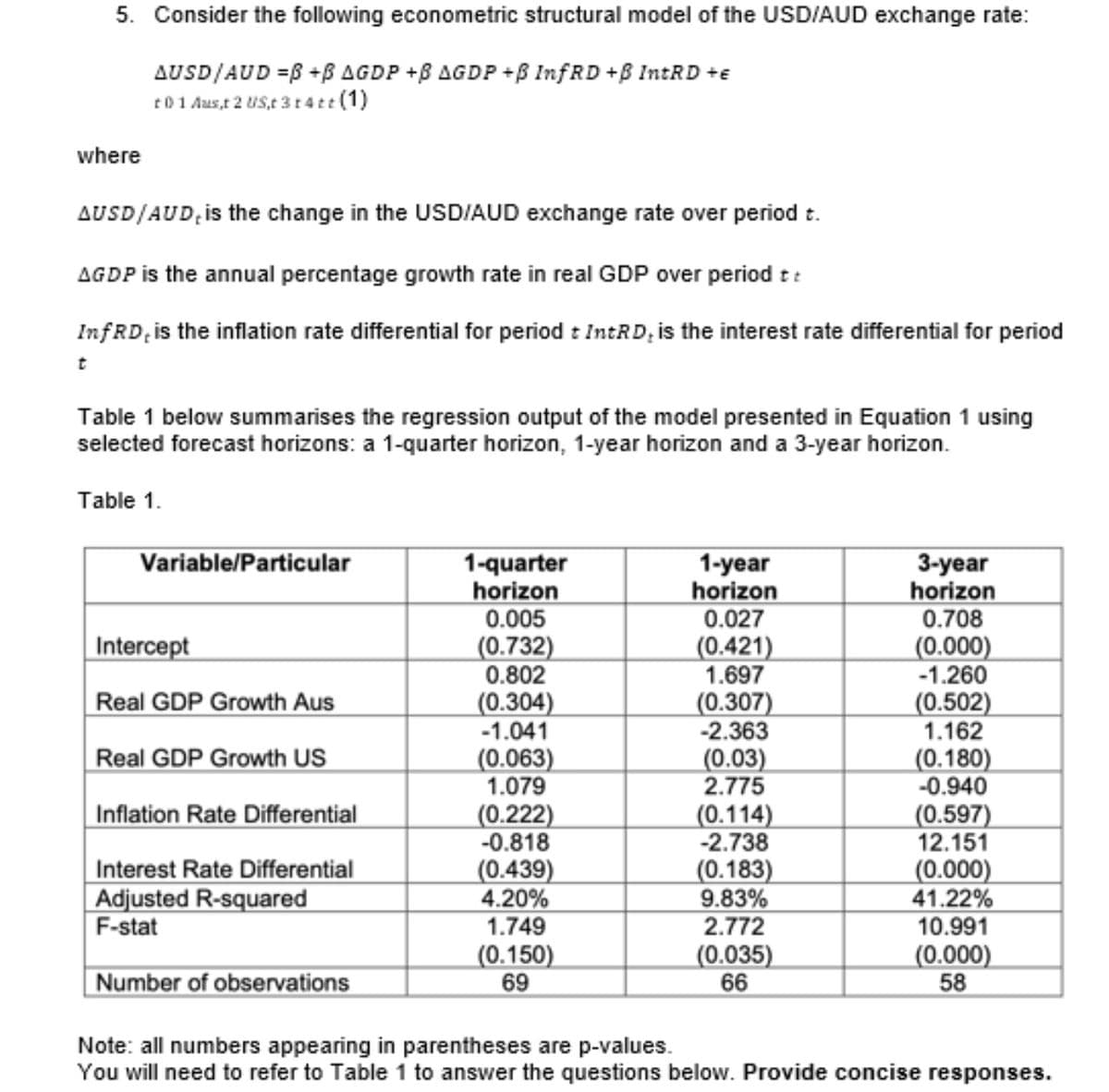

Transcribed Image Text:5. Consider the following econometric structural model of the USD/AUD exchange rate:

AUSD/AUD =B +B AGDP +B AGDP +B InfRD +B INTRD +e

t01 Aus,t 2 US,t 3 t4tt (1)

where

AUSD/AUD, is the change in the USD/AUD exchange rate over period t.

AGDP is the annual percentage growth rate in real GDP over period t:

InfRD, is the inflation rate differential for period : IntRD; is the interest rate differential for period

Table 1 below summarises the regression output of the model presented in Equation 1 using

selected forecast horizons: a 1-quarter horizon, 1-year horizon and a 3-year horizon.

Table 1.

Variable/Particular

1-quarter

horizon

0.005

(0.732)

0.802

1-year

horizon

0.027

3-year

horizon

0.708

Intercept

(0.421)

1.697

(0.000)

-1.260

(0.502)

1.162

Real GDP Growth Aus

(0.304)

-1.041

(0.063)

1.079

(0.307)

-2.363

(0.03)

2.775

Real GDP Growth US

(0.180)

-0.940

Inflation Rate Differential

(0.222)

-0.818

(0.114)

-2.738

(0.183)

9.83%

2.772

(0.597)

12.151

Interest Rate Differential

Adjusted R-squared

F-stat

(0.439)

4.20%

1.749

(0.150)

69

(0.000)

41.22%

10.991

(0.000)

58

Number of observations

(0.035)

66

Note: all numbers appearing in parentheses are p-values.

You will need to refer to Table 1 to answer the questions below. Provide concise responses.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning