ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

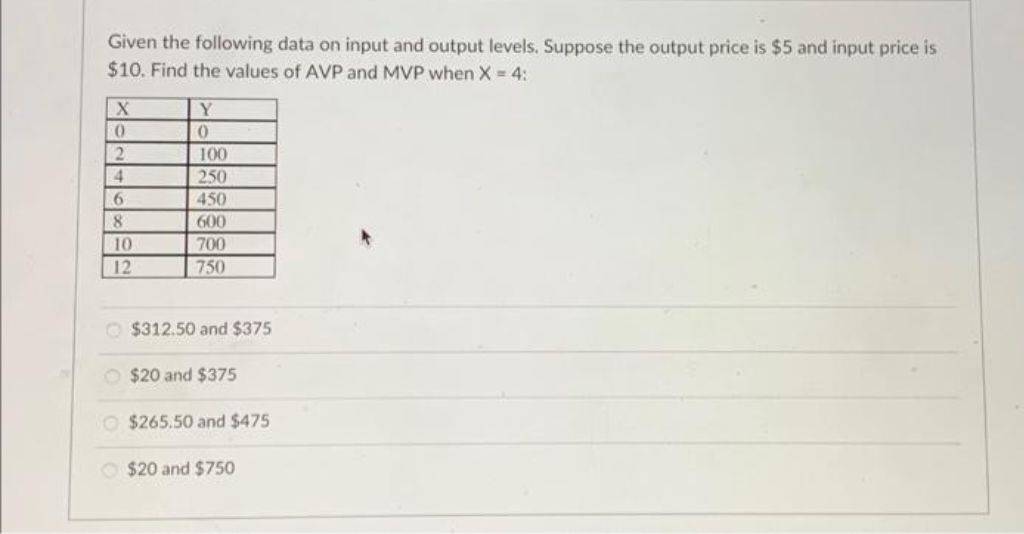

Transcribed Image Text:Given the following data on input and output levels. Suppose the output price is $5 and input price is

$10. Find the values of AVP and MVP when X = 4:

X

0

2

4

6

8

10

12

Y

0

100

250

450

600

700

750

$312.50 and $375

$20 and $375

$265.50 and $475

$20 and $750

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The tapie pelow Cotains pricerdemand and total cOSt data Tor the production of treadmilis, where p is the wholesale price (in dollars) of a treadmill for an annual demand of x treadmills, and C is the total cost (in dollars) of producing x treadmills. p ($) C ($) 2,910 1,450 3,634,000 3,415 1,275 3,782,000 4,645 1,123 4,185,000 5,330 918 4,290,000 Use this data to find a linear regression equation for price-demand data, using x as the independent variable: p= ax + b, where a is rounded to 1 decimal place and 6 is rounded to the nearest integer. Use this data to find a linear regression model for the cost data, using x as the independent variable: C(x) = cx + d, where c is rounded to the nearest integer and d is.rounded to the nearest 10,000. To Do Notifications Dashboard Calendararrow_forwardAccording to the information below, which of the following is (are) true? Units of variable input (I) Units of output (Q) 1,000 ТC TVC 200 $30,000 $25,000 TFC $55,000 b. AVC $30 The price of the variable input is $125/unit а. с. d. a. and carrow_forwardThe Nike accounting firm analyzes the price-demand relationship toconclude that x thousand shoes will sell if offered for a unit price (in dollars) of p(x) = 130−0.1x. Suppose further that the total cost of production was tracked to be $530,000 up until production of the first thousand shoes, and that this cost increased linearly to $560,000 by the time of production ofthe 2000th shoe. Find the following quantities, and interpret your results(describe what these quantities represent). a) Marginal revenue when x= 100 b) Average profit when x= 500arrow_forward

- Yummy Gummies, Inc. makes boxes of individually packaged gummies. The company has a cost function given by C(x) dollars when x boxes of Yummy Gummies are made. If C '(100) = $3.50 per box, which of the following can we conclude from this information? %3D O The approximate cost of making the 100" box of Yummy Gummies is $3.50. O The exact cost of making the 99h box of Yummy Gummies is $3.50. The approximate cost of making the 101“ box of Yummy Gummies is $3.50. O The approximate cost of making the 99 box of Yummy Gummies is $3.50. O The exact cost of making the 101st box of Yummy Gummies is $3.50.arrow_forwardHow to calculate Samsung's cost (C(Q)) of producing 1, 2,...15?arrow_forwardtype plzarrow_forward

- Am. 111.arrow_forwardFill in the missing data to solve this problem. Variable Total Average MarginalInput Product Product Product4 ? 70 ----5 ? ? 406 350 ? ? What is the total product for 5 units of input, and what is the marginal product for 6 units of input?arrow_forward3. Suppose that the feasible region of a cost minimization linear programming problem has three corners points of (5,8), (10,5), and (4,10). If the objective function is given as: Minimize Z = 2X + Y Which of the following represents an iso-cost line? Select one: a. X + 2Y = 10 b. X – Y = 10 c. 2X – Y = 10 d. 2X + Y = 10 e. none of the other options.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education