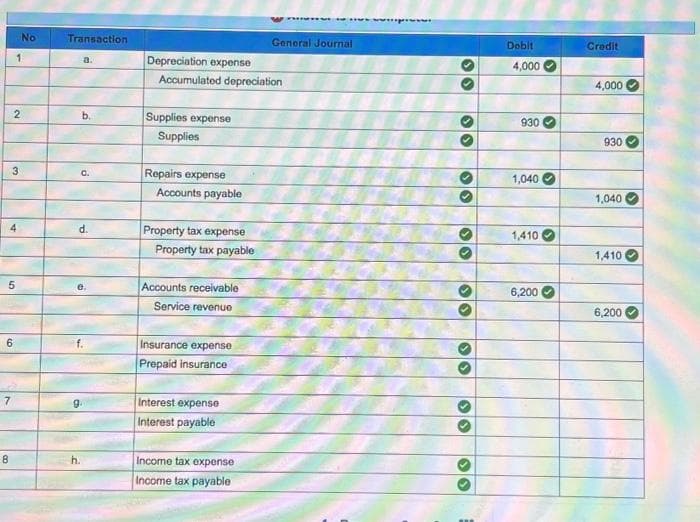

Mellor Towing Company provides hauling and delivery services for other businesses. It is at the end of its accounting year ending December 31. The following data that must be considered were developed from the company's records and related documents: a. On January 1 of the current year, the company purchased a new hauling van at a cash cost of $24,700. Depreciation estimated at $4,000 for the year has not been recorded for the current year. b. During the current year, office supplies amounting to $940 were purchased for cash and debited in full to Supplies. At the end of last year, the count of supplies remaining on hand was $330. The inventory of supplies counted on hand at the end of the current year was $340. c. On December 31 of the current year, Lanie's Garage completed repairs on one of Mellor Towing's trucks at a cost of $1,040; the amount is not yet recorded by Mellor Towing and by agreement will be paid during January of next year. d. On December 31 of the current year, property taxes on land owned during the current year were estimated at $1,410. The taxes have not been recorded and will be paid in the next year when billed. e. On December 31 of the current year, the company completed towing service for an out-of-state company for $6,200 payable by the customer within 30 days. No cash has been collected, and no journal entry has been made for this transaction. f. On July 1 of the current year, a three-year insurance premium on equipment in the amount of $900 was paid and debited in full to Prepaid Insurance on that date. Coverage began on July 1 of the current year. g. On October 1 of the current year, the company borrowed $6,000 from the local bank on a two-year, 11 percent note payable. The principal plus interest is payable at the end of 24 months. h. The income before any of the adjustments or income taxes was $38,000. The company's income tax rate is 30 percent. (Hint: Compute adjusted pre-tax income based on (a) through (g) to determine income tax expense.)

Mellor Towing Company provides hauling and delivery services for other businesses. It is at the end of its accounting year ending December 31. The following data that must be considered were developed from the company's records and related documents: a. On January 1 of the current year, the company purchased a new hauling van at a cash cost of $24,700. Depreciation estimated at $4,000 for the year has not been recorded for the current year. b. During the current year, office supplies amounting to $940 were purchased for cash and debited in full to Supplies. At the end of last year, the count of supplies remaining on hand was $330. The inventory of supplies counted on hand at the end of the current year was $340. c. On December 31 of the current year, Lanie's Garage completed repairs on one of Mellor Towing's trucks at a cost of $1,040; the amount is not yet recorded by Mellor Towing and by agreement will be paid during January of next year. d. On December 31 of the current year, property taxes on land owned during the current year were estimated at $1,410. The taxes have not been recorded and will be paid in the next year when billed. e. On December 31 of the current year, the company completed towing service for an out-of-state company for $6,200 payable by the customer within 30 days. No cash has been collected, and no journal entry has been made for this transaction. f. On July 1 of the current year, a three-year insurance premium on equipment in the amount of $900 was paid and debited in full to Prepaid Insurance on that date. Coverage began on July 1 of the current year. g. On October 1 of the current year, the company borrowed $6,000 from the local bank on a two-year, 11 percent note payable. The principal plus interest is payable at the end of 24 months. h. The income before any of the adjustments or income taxes was $38,000. The company's income tax rate is 30 percent. (Hint: Compute adjusted pre-tax income based on (a) through (g) to determine income tax expense.)

Century 21 Accounting Multicolumn Journal

11th Edition

ISBN:9781337679503

Author:Gilbertson

Publisher:Gilbertson

Chapter6: Work Sheet And Adjusting Entries For A Service Business

Section: Chapter Questions

Problem 1CP

Related questions

Concept explainers

Depreciation Methods

The word "depreciation" is defined as an accounting method wherein the cost of tangible assets is spread over its useful life and it usually denotes how much of the assets value has been used up. The depreciation is usually considered as an operating expense. The main reason behind depreciation includes wear and tear of the assets, obsolescence etc.

Depreciation Accounting

In terms of accounting, with the passage of time the value of a fixed asset (like machinery, plants, furniture etc.) goes down over a specific period of time is known as depreciation. Now, the question comes in your mind, why the value of the fixed asset reduces over time.

Topic Video

Question

![[The following information applies to the questions displayed below.]

Mellor Towing Company provides hauling and delivery services for other businesses. It is at the end of its accounting year

ending December 31. The following data that must be considered were developed from the company's records and

related documents:

a. On January 1 of the current year, the company purchased a new hauling van at a cash cost of $24,700. Depreciation

estimated at $4,000 for the year has not been recorded for the current year.

b. During the current year, office supplies amounting to $940 were purchased for cash and debited in full to Supplies.

At the end of last year, the count of supplies remaining on hand was $330. The inventory of supplies counted on

hand at the end of the current year was $340.

c. On December 31 of the current year, Lanie's Garage completed repairs on one of Mellor Towing's trucks at a cost of

$1,040; the amount is not yet recorded by Mellor Towing and by agreement will be paid during January of next year.

d. On December 31 of the current year, property taxes on land owned during the current year were estimated at $1,410.

The taxes have not been recorded and will be paid in the next year when billed.

e. On December 31 of the current year, the company completed towing service for an out-of-state company for $6,200

payable by the customer within 30 days. No cash has been collected, and no Journal entry has been made for this

transaction.

f. On July 1 of the current year, a three-year insurance premium on equipment in the amount of $900 was paid and

debited in full to Prepaid Insurance on that date. Coverage began on July 1 of the current year.

g. On October 1 of the current year, the company borrowed $6,000 from the local bank on a two-year, 11 percent note

payable. The principal plus interest is payable at the end of 24 months.

h. The income before any of the adjustments or income taxes was $38,000. The company's income tax rate is 30

percent. (Hint: Compute adjusted pre-tax income based on (a) through (g) to determine income tax expense.)

inate the adiveting ontos required for each transaction at December 31 of the current year](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F6ae00e5b-3d71-443b-82e5-17d4bd934d05%2Fb2f64cb7-5e81-4808-83c3-8c2243a42be8%2F0mmzggh_processed.jpeg&w=3840&q=75)

Transcribed Image Text:[The following information applies to the questions displayed below.]

Mellor Towing Company provides hauling and delivery services for other businesses. It is at the end of its accounting year

ending December 31. The following data that must be considered were developed from the company's records and

related documents:

a. On January 1 of the current year, the company purchased a new hauling van at a cash cost of $24,700. Depreciation

estimated at $4,000 for the year has not been recorded for the current year.

b. During the current year, office supplies amounting to $940 were purchased for cash and debited in full to Supplies.

At the end of last year, the count of supplies remaining on hand was $330. The inventory of supplies counted on

hand at the end of the current year was $340.

c. On December 31 of the current year, Lanie's Garage completed repairs on one of Mellor Towing's trucks at a cost of

$1,040; the amount is not yet recorded by Mellor Towing and by agreement will be paid during January of next year.

d. On December 31 of the current year, property taxes on land owned during the current year were estimated at $1,410.

The taxes have not been recorded and will be paid in the next year when billed.

e. On December 31 of the current year, the company completed towing service for an out-of-state company for $6,200

payable by the customer within 30 days. No cash has been collected, and no Journal entry has been made for this

transaction.

f. On July 1 of the current year, a three-year insurance premium on equipment in the amount of $900 was paid and

debited in full to Prepaid Insurance on that date. Coverage began on July 1 of the current year.

g. On October 1 of the current year, the company borrowed $6,000 from the local bank on a two-year, 11 percent note

payable. The principal plus interest is payable at the end of 24 months.

h. The income before any of the adjustments or income taxes was $38,000. The company's income tax rate is 30

percent. (Hint: Compute adjusted pre-tax income based on (a) through (g) to determine income tax expense.)

inate the adiveting ontos required for each transaction at December 31 of the current year

Transcribed Image Text:5

6

7

8

2

3

4

1

No

Transaction

b.

C.

d.

Depreciation expense

Accumulated depreciation

Supplies expense

Supplies

Repairs expense

Accounts payable

Property expense

Property tax payable

Accounts receivable

Service revenue

Insurance expense

Prepaid insurance

Interest expense

Interest payable

General Journal

Income tax expense

Income tax payable

>

33

33

33

>>

>>

m

Dobit

4,000

930

1,040

1,410

6,200

Credit

4,000

930

1,040

1,410

6,200

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning