Prepare adjusting journal entries for the month of December. The insurance policy is for 1 year. List the debit entries before credit entries. If no entry is required, select No Entry.

Prepare adjusting journal entries for the month of December. The insurance policy is for 1 year. List the debit entries before credit entries. If no entry is required, select No Entry.

College Accounting, Chapters 1-27

23rd Edition

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:HEINTZ, James A.

Chapter18: Accounting For Long-term Assets

Section: Chapter Questions

Problem 9SPA: CALCULATING AND JOURNALIZING DEPRECIATION Equipment records for Johnson Machine Co. for the year...

Related questions

Question

Prepare

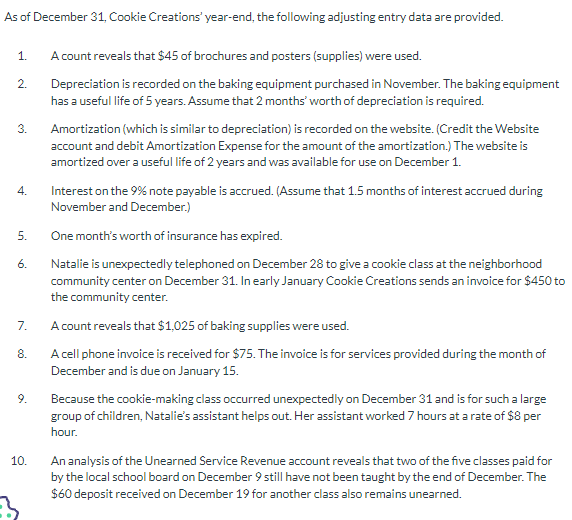

Transcribed Image Text:As of December 31, Cookie Creations' year-end, the following adjusting entry data are provided.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

A count reveals that $45 of brochures and posters (supplies) were used.

Depreciation is recorded on the baking equipment purchased in November. The baking equipment

has a useful life of 5 years. Assume that 2 months' worth of depreciation is required.

Amortization (which is similar to depreciation) is recorded on the website. (Credit the Website

account and debit Amortization Expense for the amount of the amortization.) The website is

amortized over a useful life of 2 years and was available for use on December 1.

Interest on the 9% note payable is accrued. (Assume that 1.5 months of interest accrued during

November and December.)

One month's worth of insurance has expired.

Natalie is unexpectedly telephoned on December 28 to give a cookie class at the neighborhood

community center on December 31. In early January Cookie Creations sends an invoice for $450 to

the community center.

A count reveals that $1,025 of baking supplies were used.

A cell phone invoice is received for $75. The invoice is for services provided during the month of

December and is due on January 15.

Because the cookie-making class occurred unexpectedly on December 31 and is for such a large

group of children, Natalie's assistant helps out. Her assistant worked 7 hours at a rate of $8 per

hour,

An analysis of the Unearned Service Revenue account reveals that two of the five classes paid for

by the local school board on December 9 still have not been taught by the end of December. The

$60 deposit received on December 19 for another class also remains unearned.

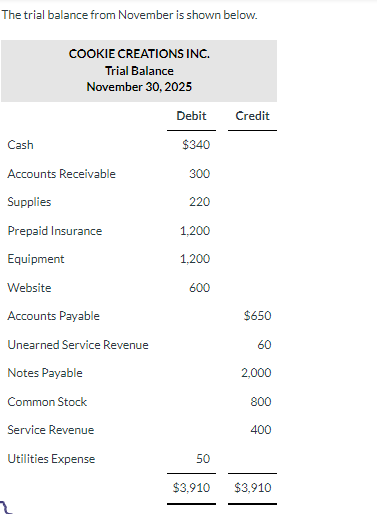

Transcribed Image Text:The trial balance from November is shown below.

COOKIE CREATIONS INC.

Trial Balance

November 30, 2025

Cash

Accounts Receivable

Supplies

Prepaid Insurance

Equipment

Website

Accounts Payable

Unearned Service Revenue

Notes Payable

Common Stock

Service Revenue

Utilities Expense

Debit

$340

300

220

1,200

1.200

600

50

Credit

$650

60

2,000

800

400

$3,910 $3,910

Expert Solution

Step 1

Adjustment Journal Entry

A general ledger entry known as a "adjustment journal entry" is made at the conclusion of an accounting period to report any unrealized income or costs during the time. An adjusting journal entry is necessary to correctly account for a transaction that began in one accounting period and ended in another. Adjusting journal entries can also be used to describe financial statements that fixes an error from a prior accounting period.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

College Accounting, Chapters 1-27 (New in Account…

Accounting

ISBN:

9781305666160

Author:

James A. Heintz, Robert W. Parry

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub