MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

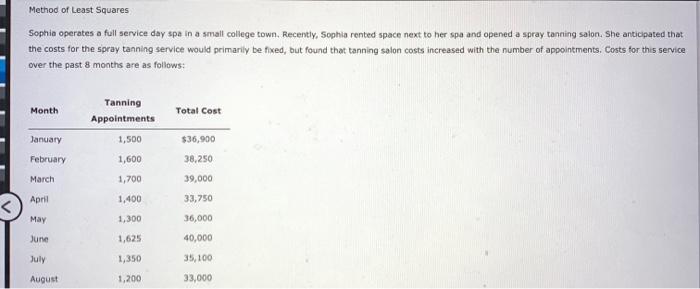

Method of Least Squares Sophia operates a full service day spa in a small college town. Recently, Sophia rented space next to her spa and opened a spray tanning salon. She anticipated that the costs for the spray tanning service would primarily be fixed, but found that tanning salon costs increased with the number of appointments. Costs for this service over the past 8 months are as follows: Month January February March April May June July August Tanning Appointments 1,500 1,600 1,700 1,400 1,300 1,625 1,350 1,200 Total Cost $36,900 38,250 39,000 33,750 36,000 40,000 35,100 33,000

Transcribed Image Text:Method of Least Squares

Sophia operates a full service day spa in a small college town. Recently, Sophia rented space next to her spa and opened a spray tanning salon. She anticipated that

the costs for the spray tanning service would primarily be fixed, but found that tanning salon costs increased with the number of appointments. Costs for this service

over the past 8 months are as follows:

Month

January

February

March

April

May

June

July

August

Tanning

Appointments

1,500

1,600

1,700

1,400

1,300

1,625

1,350

1,200

Total Cost

$36,900

38,250

39,000

33,750

36,000

40,000

35,100

33,000

Transcribed Image Text:Required:

1. Using a computer spreadsheet program such as Excel, run a regression on these data. Based on the regression output, select the cost formula for tanning. Round

the fixed cost to the nearest dollar and the variable rate to the nearest cent.

2. Using the computed formula, what is the predicted cost of tanning services for September for 1,550 appointments? Round to the nearest dollar.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 14 images

Knowledge Booster

Similar questions

- need comprehensive and correct answers.This question is about optimization.arrow_forwardSuppose you are the marketing manager of a firm, and you plan to introduce a new product to the market. You have to estimate the first year net profit, which depends on several variables • Sales volume (in units) • Price per unit • Unit cost . Fixed costs Your net profit is net profit = sales volume x (price per unit-unit cost) - fixed cost The fixed cost is $120, 000, but other factors have some uncertainty. Based on your market research, there are equal chance that the market will be slow, ok, or hot. • Slow market the sales volume follows Poisson distribution with mean 50,000 units product, and the average price per unit is $11.00 ● Ok market the sales volume follows Poisson distribution with mean 75,000 units product, the average price per unit is $10.00 Hot market: the sales volume follows Poisson distribution with mean 100,000 units product, but the competition is severe so you expect the average price per unit is just $8.00 No matter what the market type is, your average unit…arrow_forwardPLEASE ANSWER EVERYTHING. I WILL UPVOTE ALL I PROMISE. DO NOT DO THIS IF YOU ALREADY DID THIS.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman