Terry Inc. manufactures machine parts for aircraft engines. CEO Bucky Walters is considering an offer from a subcontractor to provide 2,000 units of product OP89 for $120,000. If Terry does not purchase these parts from the subcontractor, it must continue to produce them in-house with these costs: Cost per unit ($) Direct Materials 28 Direct Labor 18 Variable Overhead 16 Allocated Fixed Overhead 4 Required 1. What is the relevant cost to make the product internally? 2. What is the estimated increase or decrease in short-term operating profit of producing the product internally versus purchasing the product from a supplier? 3. Which alternative is more attractive to Terry Inc, make or buy the machine parts?

Terry Inc. manufactures machine parts for aircraft engines. CEO Bucky Walters is considering an offer from a subcontractor to provide 2,000 units of product OP89 for $120,000. If Terry does not purchase these parts from the subcontractor, it must continue to produce them in-house with these costs: Cost per unit ($) Direct Materials 28 Direct Labor 18 Variable Overhead 16 Allocated Fixed Overhead 4 Required 1. What is the relevant cost to make the product internally? 2. What is the estimated increase or decrease in short-term operating profit of producing the product internally versus purchasing the product from a supplier? 3. Which alternative is more attractive to Terry Inc, make or buy the machine parts?

Chapter10: Short-term Decision Making

Section: Chapter Questions

Problem 7EB: Oat Treats manufactures various types of cereal bars featuring oats. Simmons Cereal Company has...

Related questions

Question

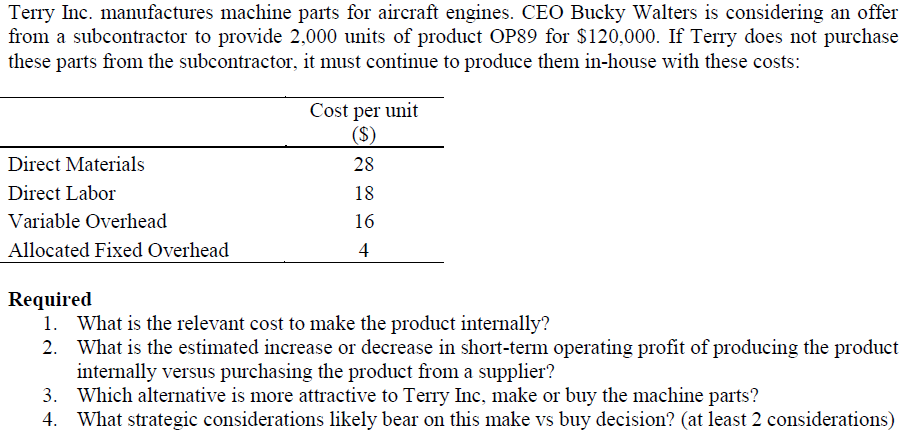

Transcribed Image Text:Terry Inc. manufactures machine parts for aircraft engines. CEO Bucky Walters is considering an offer

from a subcontractor to provide 2,000 units of product OP89 for $120,000. If Terry does not purchase

these parts from the subcontractor, it must continue to produce them in-house with these costs:

Cost per unit

($)

Direct Materials

28

Direct Labor

18

Variable Overhead

16

Allocated Fixed Overhead

4

Required

1. What is the relevant cost to make the product internally?

What is the estimated increase or decrease in short-term operating profit of producing the product

internally versus purchasing the product from a supplier?

3. Which alternative is more attractive to Terry Inc, make or buy the machine parts?

4. What strategic considerations likely bear on this make vs buy decision? (at least 2 considerations)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning